To investors,

Below is a guest post from Jan Wüstenfeld analyzing consumer price inflation, monetary inflation, and whether bitcoin is a hedge against one or both. Jan is pursuing a Ph.D. in Economics in Germany and is an on-chain analyst for Quantum Economics. He writes Bitcoin Market Intelligence, a fortnightly newsletter on Bitcoin, markets, on-chain analysis, and macro perspectives. Enjoy!

With inflation sky high and bitcoin price on a downward trend, particularly bitcoin critics have started celebrating another “win” that bitcoin does not appear to hedge against inflation. One of the traits often attributed to bitcoin.

Yes, it may be true that it is not a good hedge against consumer price inflation as measured by the consumer price index (CPI). But is that the right metric to look at? Or should we look at monetary inflation in the Austrian Economics sense and how bitcoin fares against it?

Summary:

No clear relationship between CPI and bitcoin price

bitcoin a hedge against (extreme) monetary inflation

or at least dependent on central bank liquidity

Is bitcoin a hedge against consumer price inflation?

Many have argued that bitcoin is supposed to perform well in times of high consumer price inflation due to its properties (scarcity in particular). But is that really the case?

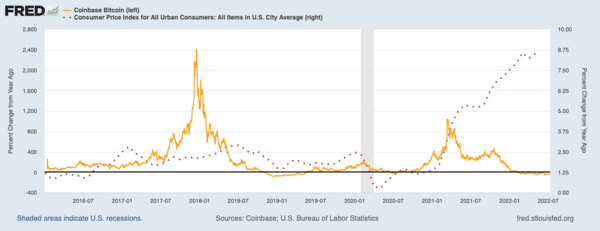

Graph 1 shows the percentage of bitcoin’s price compared to a year ago and that of the Consumer Price Index for All Urban Consumers: All Items in the U.S. City Average since the beginning of 2017.

Just by the looks of it, there does not appear to be a clear correlation between consumer price inflation and bitcoin’s price. Particularly pre-COVID-19, it is hard to see a clear relationship.

|

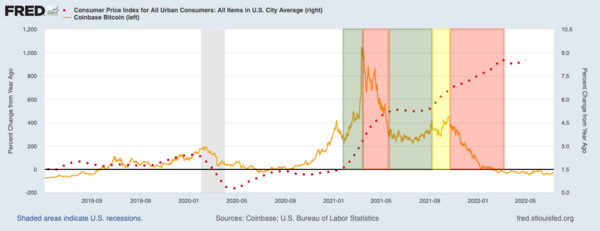

In Graph 2, I zoomed in on this cycle so that the scale is not as distorted by price changes in 2017.

Since 2020 some co-movements between both variables can be observed. While there are co-movements (green areas) or one of the variables at times seems to lead the other, they are also trending in opposing directions for a substantial time of this cycle (red areas).

Bitcoin’s price already started to rise before inflation started to rise.

Some argue that in this case, bitcoin’s price has been front-running high inflation numbers. However, I don’t really buy this argument.

While many bitcoiners may have been predicting high inflation numbers due to increasing monetary intervention (for the right or wrong reasons), I do not think most market participants have bought bitcoin to hedge against upcoming inflation numbers.

I believe that price has been primarily driven by a central bank-induced liquidity rally which better matches the data as I will explain below.

|

Is bitcoin a hedge against monetary inflation?

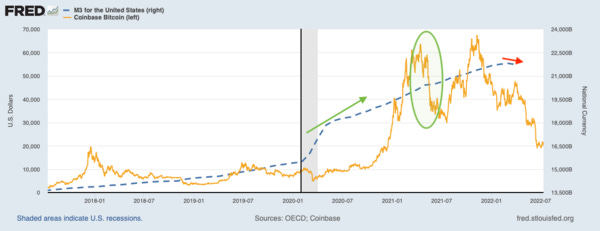

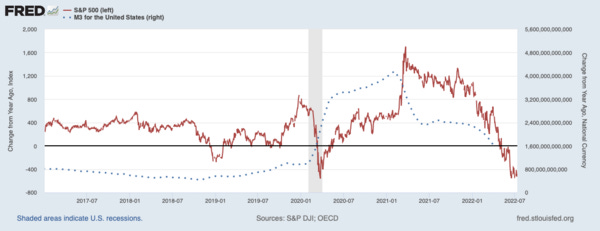

In Graph 3 the bitcoin price in USD and the value of the money supply M3 of the USD are displayed (the picture is very similar if M2 is used, but M3 is broader, so I am going to use M3 here).

Not long after M3 started to explode upwards at the beginning of 2020 bitcoin’s price did also bottom out during the flash crash in March. Around mid-2021 when M3 started to slow bitcoin’s price started to decline as well.

Lately, we have even seen M3 starting to decline as the Fed is taking liquidity out of the system.

|

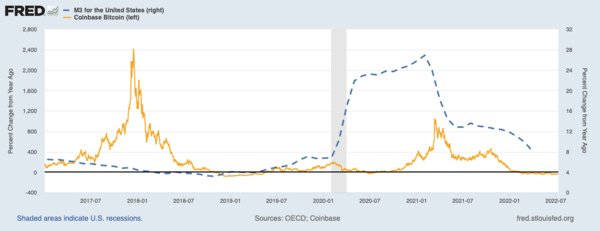

In Graph 3, the slow down in money supply growth and its relation to bitcoins price growth is not as visible. The percentage change from a year ago shows that much more clearly in Graph 4.

In February 2021, the year-over-year money supply growth of M3 started to peak. Shortly after that, bitcoin’s year-over-year price growth peaked in mid-March. The lagging reaction of bitcoin’s price may be as liquidity injections and withdrawals by the Fed potentially take time to materialize in the markets.

Interestingly, when the decline in M3 growth slows, you can see bitcoin’s price growth behave similarly.

M3 and bitcoin’s price movements even match over the last months, whereas the price of bitcoin does not match with CPI developments over the last months.

Following this, the data speaks for bitcoin being a hedge against monetary inflation over it being a hedge against consumer price inflation.

In the previous cycle, we do not see the relationship between bitcoin and M3 as clearly.

On the one hand, this may be since M3 did not increase to such an extreme, and on the other hand, the retail frenzy in 2017 could have been the dominating factor.

So bitcoin may be a hedge against extreme monetary inflation, as we have seen during this cycle, but not necessarily modest monetary inflation.

|

However, it is important to point out that with increasing monetary intervention and liquidity injections, not only bitcoin benefited but also financial assets.

For instance, if you look at the year-over-year change of the S&P 500, the index shows a very similar pattern to that of bitcoin (see: Graph 5). This is not surprising as they have been highly correlated during this cycle.

Due to this, some might argue that bitcoin is not a hedge against monetary inflation but that liquidity is simply lifting all boats.

|

Whether you call bitcoin a hedge against (extreme) monetary inflation or argue that it simply goes up with increasing central bank liquidity as many other assets do is up to you.

Currently, the Fed is hard on the brakes and with that is dampening bitcoin’s price.

But worry not. Three things are certain in life:

Death

Taxes

And ever-increasing monetary intervention by central banks

It is just a matter of time before the interventionist spiral of central banks turns back on. Once the Fed pivots or hints at a pivot it is time for bitcoin to shine again.

This was a guest post from Jan Wüstenfeld, who is pursuing a Ph.D. in Economics in Germany and is an on-chain analyst for Quantum Economics. He writes Bitcoin Market Intelligence, a fortnightly newsletter on Bitcoin, markets, on-chain analysis, and macro perspectives. I hope this was valuable to each of you. Have a great weekend and I’ll talk to everyone on Monday.

-Pomp

SPONSOR:

Valour is the first and only publicly traded company built to give investors direct exposure to the rapidly growing space of decentralized finance (DeFi). The company provides simplified, trusted access to crypto, decentralized finance and Web 3.0 investment opportunities.

Institutions and investors can gain diversified, secure, compliant, and easily tradable access to a diversified set of industry-leading equity products and protocols, through a single stock purchase on a regulated exchange. Currently listed on U.S. (OTC: DEFTF) and Canadian (NEO:DEFI) exchanges. For more information or to subscribe to receive company updates and financial information, visit https://valour.com/

|

Darius Dale is the Founder & CEO of 42 Macro, the leading macro risk manager adviser.

In this conversation, we discuss the macro economy, 9.1% inflation rate in the United States, why Inflation does not appear to be subsiding any time soon, and how can we get out of this current economic crisis.

Listen on iTunes: Click here

Listen on Spotify: Click here

Federal Reserve Thinks The Lightning Network Will Improve Bitcoin

Podcast Sponsors

These companies make the podcast possible, so go check them out and thank them for their support!

BCB Groupis the leading payment services partner for the digital assets industry. BCB Group provides payment services in 30+ currencies, FX, cryptocurrency liquidity, digital asset custody and BLINC–BCB’s free, instant settlements network for the BCB client ecosystem. Find out more by visiting bcbgroup.com/pomp

Coinchange is an automated wealth management platform. Register now at coinchange.io/pomp and get a welcome bonus of 40 USDC when you fund your account.

Copper has been at the forefront of institutional digital asset development since 2018. From award winning custody solutions, to creating the first truly off-exchange settlement function, Copper pioneers technology, products, and services, in lock-step with a rapidly changing world. Learn how Copper helps the world’s largest institutional investors secure their digital assets at copper.co

Eight Sleep is the most advanced solution on the market for thermoregulation by pairing dynamic cooling and heating with biometric tracking. Click here to check out the Pod Pro Cover and save $150 at checkout.

Bullish is a powerful exchange for digital assets that offers deep liquidity, automated market making, and industry-leading security. Click here to learn more.

Valour represents what’s next in the digital economy -- providing simplified, trusted access to crypto, decentralized finance and Web 3.0 investment opportunities. For more information visit valour.com

Unstoppable Domains’ 10 NFT domain endings are now fully integrated with Trust Wallet. Claim your Unstoppable Domainhere today.

FTX US is the safe, regulated way to buy digital assets. Trade crypto with up to 85% lower fees than top competitors by signing up at FTX.US today.

Compass Mining is the world's first online marketplace for bitcoin mining hardware and hosting. Visit compassmining.io to start mining bitcoin today!

LMAX Digitalis the market-leading solution for institutional crypto trading & custodial services. Learn more at LMAXdigital.com/pomp

Exodus is the world’s leading desktop, mobile, and hardware crypto wallets, with over 150 assets. Founded in 2015 to empower people to control their wealth. Visit http://exodus.com/pomp today.

You are receiving The Pomp Letter because you either signed up or you attended one of the events that I spoke at. Feel free to unsubscribe if you aren’t finding this valuable. Nothing in this email is intended to serve as financial advice. Do your own research.

You’re a free subscriber to The Pomp Letter. For the full experience, become a paid subscriber.

© 2022

5 West Hargett St, Suite 1110, Raleigh, NC 27601

Unsubscribe

![]()

![]()