Click here for full report and disclosures

Click here to request a call about this note.

â Historic shock meets historic policy response: The Bank of Englandâs (BoE) exceptionally loose monetary and financial policies during 2020 and early 2021 were a necessary and proportionate response to the historic COVID-19 pandemic and economic downturn. But now that a robust recovery is underway, policies need to adjust. In this note, we assess the economic and BoE policy outlook and make the following conclusions.

1) Normal economic times require normal policies: During the post-Lehman era, the normalisation of BoE monetary policy had been hamstrung by the need to strengthen the financial system, repair private-sector balance sheets and by political uncertainty. This time is different. The BoEâs ultra-loose policies are underpinning a strong cyclical recovery from the pandemic. As part and parcel of the rebound, inflationary pressures are building, inflation expectations are rising and credit demand and availability are strong.

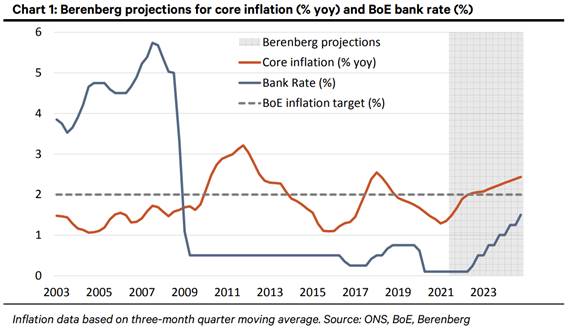

2) Policy rate hikes may occur earlier than expected: Relative to the outlook for robust growth and sustained inflation at rates above the BoEâs 2% target, monetary policy is becoming too easy. Real rates continue to fall as inflation expectations rise and as the BoE holds benchmark rates artificially low via asset purchases. We expect the BoE to begin a gradual normalisation of its policies in 2022 after completing asset purchases by end-2021 – Chart 1. We expect the first rate hike in August 2022 (15bp) followed by a further 25bp hike in November 2022 – to take the bank rate to 0.5% by end-2022. We bring our first hike call forward from early 2023 previously.

3) A policy normalisation is not a tightening: Financial policy will not constrain economic activity, unlike in past cycles. Banks entered the COVID-19 pandemic with adequate capital and liquidity. While regulators ensured that additional capital buffers could be used by banks, these were not necessary. Partly as a result, the normalisation of regulations will not affect credit conditions meaningfully. Similarly, further substantial rises in bond yields – 10-year to 2.3% by end-2023 – reflect a strong upswing and should not be a significant impediment to growth.

â Conference call: We would like to invite investors to a call on 27 May to discuss these issues alongside our broader UK strategy and views on UK banks. To register, please contact Berenbergâs salesteam or Eleni Papoula, our financials specialist salesperson (eleni.papoula@berenberg.com).

Kallum Pickering

Senior Economist

+44 20 3465 2672

kallum.pickering@berenberg.com

Analyst

+44 20 3465 2681

peter.richardson@berenberg.com

![]()

Disclosures

This material is intended as commentary on political, economic or market conditions for institutional investors or market professionals only and does not constitute a financial analysis or a research report as defined by applicable regulation. See the "Disclaimers" section of this report.

The commentary included herein was produced by Joh. Berenberg, Gossler & Co. KG (Berenberg). For sales inquiries, please contact:

Phone: +44 (0)20 3207 7800

Email: berenberg.economics@berenberg.com

BERENBERG

Joh. Berenberg, Gossler & Co. KG

Neuer Jungfernstieg 20

20354 Hamburg

Germany

Registered Office: Hamburg, Germany

Local Court Hamburg HRA 42659

Joh. Berenberg, Gossler & Co. KG is a Kommanditgesellschaft (a German form of limited partnership) established under the laws of the Federal Republic of Germany registered with the Commercial Register at the Local Court of the City of Hamburg under registration number HRA 42659 with its registered office at Neuer Jungfernstieg 20, 20354 Hamburg, Germany. A list of partners is available for inspection at our London Branch at 60 Threadneedle Street, London, EC2R 8HP, United Kingdom.

Joh. Berenberg, Gossler & Co. KG is authorised by the German Federal Financial Supervisory Authority (BaFin) and deemed authorised and regulated by the Financial Conduct Authority. The nature and extent of consumer protections may differ from those for firms based in the UK. Details of the Temporary Permissions Regime, which allows EEA-based firms to operate in the UK for a limited period while seeking full authorisation, are available on the Financial Conduct Authorityâs website. For further information as well as specific information on Joh. Berenberg, Gossler & Co. KG, its head office and its foreign branches in the European Union please refer to http://www.berenberg.de/en/corporate-disclosures.html.