Click here for full report and disclosures

Click here to request a call about this note.

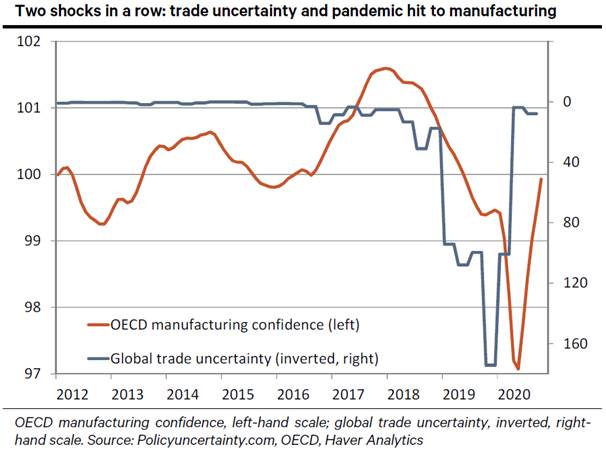

â The case for strong growth in 2021: Over the past two years, the world economy has been battered by two major shocks in rapid succession. In 2019, Donald Trumpâs trade war against China and his threats against the European Union and others caused a dramatic spike in trade policy uncertainty – see chart. Shortly after the uncertainty started to fade in late 2019 due to a âphase oneâ US-China trade deal, the pandemic dealt an unprecedented blow to the world economy. Now, all we need to justify a positive outlook for 2021 is a simple assumption: neither of these two shocks will be repeated next year. Joe Biden will pursue a much calmer and more predictable trade policy. And with the advent of spring in the northern hemisphere and ongoing medical progress, the worst of the COVID-19 pandemic should finally be behind us by April at the latest. Thanks to vaccines, we will hopefully be spared a comparable third wave in autumn 2021.

â Trade war damage: Manufacturing confidence in OECD countries started to weaken in 2018 as China briefly scaled back its domestic economic stimulus. From late 2018 onwards, US-stoked trade tensions then turned into a major drag on the global economy. Largely because of this factor, economic growth in the export-oriented Eurozone slowed from an annualised rate of c2% in late 2018 and early 2019 to below 1% by the end of 2019. On its own, the absence of such tensions could contribute 1ppt to Eurozone growth next year. OECD manufacturing confidence is already above its pre-COVID level.

â The Biden effect: The size of the next US fiscal package and the extent to which Biden can pursue his domestic agenda will partly depend on the run-off elections for two Senate seats in Georgia on 5 January. But for the world economy, his foreign and trade policies will matter more. By picking experienced people for key posts – Antony Blinken as foreign minister, John Kerry for climate change, Janet Yellen for the Treasury – he has sent a strong signal: he will shift from Trumpâs erratic confrontation back to co-operation with Europe and support rules-based global trade.

â Better times for Europe: Trump will leave office on 20 January and COVID-19 should cease to be a major drag by spring 2021 at the latest. In addition, the end of Brexit uncertainty will unlock some investment into the restructuring of pan-European supply chains. Combined with a likely uptick in demand for durable and capital goods in the early phase of a new global business cycle, producers in export-oriented Europe can enjoy outsized gains once the current wave of the pandemic has faded. Europe suffered a deeper recession in 2020 than other major parts of the global economy. Supported also by a record monetary and fiscal stimulus, Europe can enjoy relatively fast catch-up growth in 2021.

â Turning risk on – the dollar story: When the global recovery gains momentum next year and risk appetites recover further, investors will likely redirect some funds out of the safe haven of the US dollar toward opportunities in emerging markets and, to a lesser extent, also in Europe. Versus the euro and pound sterling, we thus expect the dollar to weaken to 1.25 and 1.47, respectively, over the course of 2021.

Holger Schmieding

Chief Economist

+44 20 3207 7889

holger.schmieding@berenberg.com

Kallum Pickering

Senior Economist

+44 20 3465 2672

kallum.pickering@berenberg.com

Florian Hense

European Economist

+4420 3207 7859

florian.hense@berenberg.com

![]()

Disclosures

This material is intended as commentary on political, economic or market conditions for institutional investors or market professionals only and does not constitute a financial analysis or a research report as defined by applicable regulation. See the "Disclaimers" section of this report.

The commentary included herein was produced by Joh. Berenberg, Gossler & Co. KG (Berenberg). For sales inquiries, please contact:

Phone: +44 (0)20 3207 7800

Email: berenberg.economics@berenberg.com

BERENBERG

Joh. Berenberg, Gossler & Co. KG

Neuer Jungfernstieg 20

20354 Hamburg

Germany

Registered Office: Hamburg, Germany

Local Court Hamburg HRA 42659