Click here for full report and disclosures

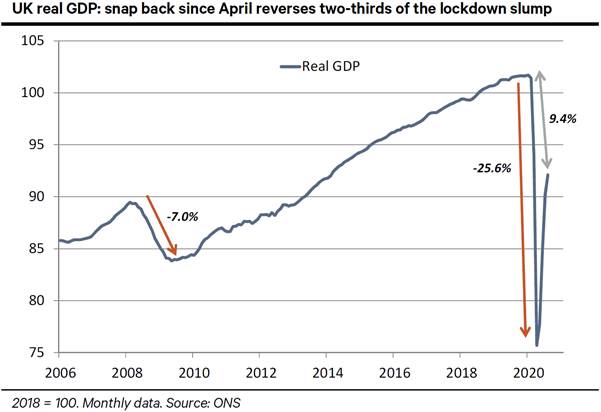

â Fading gains: The summer rebound from the massive slump in GDP during the UKâs spring lockdown lost more momentum than expected in August. Real GDP rose by 2.1% mom after a 6.4% gain in July, according to the ONS. In line with the solid survey data through August, including PMIs at multi-year high, we had projected a 3.0% mom gain. Despite the August disappointment, however, the data still show a strong snap back in economic activity from May onwards. In the four months to August, the UK economy recovered almost two-thirds of the record 25.6% decline in GDP between January and April – see chart.

â Uneven gains in August: Domestic-oriented services expanded by 2.4% mom in August after a 5.9% gain in July. While key sub-sectors such as retail have recouped all of their losses, others remain weak, though. For instance, education

(-16.0%) and human health (-24.1%) remained well below their January levels. However, estimates for these sectors may be artificially low due to statistical factors. A reversal of such factors could lead to a sudden jump in real output. Despite strong gains in global trade during the summer, export-oriented industrial production edged up by just 0.3% mom (+5.2% in July). Construction gains slowed to 3.0% mom from 17.2% in July with output still 12.0% below its January peak.

â Robust Q3 gives way to serious virus risks: Survey data on production and consumer sectors as well as the housing market point to sustained gains in economic momentum through September. However, following the disappointment in the August monthly GDP estimate, we downgrade our Q3 growth estimate to a still strong 15.8% from 16.2% previously.

â Big slowdown in Q4. Reacting to the sharp increase in the number of SARS-COV 2 infections, national and local governments across the UK are once again tightening restrictions on daily life. The rules range from limiting the number of people in a group and a 10pm curfew for pubs and restaurants across England, to the temporary closure of such places across the central belt of Scotland. Further restrictions in parts of northern England look likely in the days to come. Amid mounting restrictions, and in line with our latest revisions to the Eurozone outlook, we downgrade our Q4 call to 2.0% qoq from 2.5% previously. Due to the statistical overhang from the big rise during Q3, quarterly Q4 growth would be 1.7% qoq even if economic momentum stalled between September and December. The changes to our H2 calls lower our 2020 annual projection from -9.9% to -10.1%.

â No major Brexit disruptions (probably): As long as the UK avoids a disorderly hard exit (80% probability) from the EU single market on 31 December, downside risks from the virus restrictions in Q4 would be partly offset by upside risks thereafter once such restrictions are eased. Reflecting a likely catch-up from a weaker Q4, we raise our qoq calls for Q1 and Q2 2021 to 1.9% and 1.5% from 1.5% and 1.0%, respectively. This lifts our annual 2021 call to 6.6% from 6.4%. The news that UK and EU negotiators are making some progress helps to limit the risk of new shock in Q1 while raising the hope of a deal (30%) rather than stopgap measures to manage a no-deal exit (50%). When EU leaders assess the progress of UK-EU talks at the 15-16 October EU summit, we may get a better sense of year-end prospects for the UK.

Chief Economist

+44 20 3207 7889

holger.schmieding@berenberg.com

Senior Economist

+44 20 3465 2672

kallum.pickering@berenberg.com

European Economist

+4420 3207 7859

![]()

Disclosures

This material is intended as commentary on political, economic or market conditions for institutional investors or market professionals only and does not constitute a financial analysis or a research report as defined by applicable regulation. See the "Disclaimers" section of this report.

The commentary included herein was produced by Joh. Berenberg, Gossler & Co. KG (Berenberg). For sales inquiries, please contact:

Phone: +44 (0)20 3207 7800

Email: berenberg.economics@berenberg.com

BERENBERG

Joh. Berenberg, Gossler & Co. KG

Neuer Jungfernstieg 20

20354 Hamburg

Germany

Registered Office: Hamburg, Germany

Local Court Hamburg HRA 42659