Click here for full report and disclosures

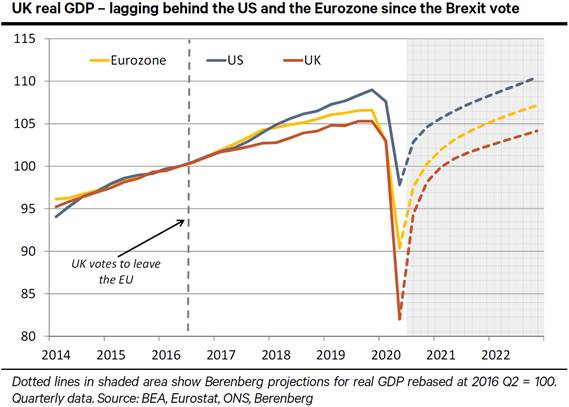

â Bad decisions damage economies: Brexit is not going well for the UK so far. Our chart tells a clear story. Shortly after the UK voted in June 2016 to leave the EU, the UK economy started to underperform its major trading partners. Bad policy choices linked to Brexit and the response to the COVID-19 pandemic have taken a heavy toll on the UK economy.

â The Brexit gap: UK GDP grew at a respectable 2.4% yoy in the three years up to the June 2016 referendum – only slightly below the US (2.5%) but well above the Eurozone (1.5%). From Q3 2016 until Q4 2019, UK GDP growth decelerated to an annual average of 1.6% as business investment stagnated and private consumption growth slowed to 1.9% yoy (versus 2.8% pre-referendum). Brexit uncertainty and messy domestic politics, including two snap elections, weighed on confidence and risk appetites in the private sector. Over the same period US growth –supported by a big fiscal stimulus – remained solid at 2.5% yoy while growth in the Eurozone – helped by aggressive ECB easing – accelerated to 2.0% yoy.

â Fumbled pandemic response: The UK government has added to the economyâs problems since the COVID-19 pandemic struck in early 2020. Because the UK imposed a national lockdown to contain the pandemic roughly a week later than other major European nations, the harsh restrictions had to remain in place for longer than elsewhere in order to bring the virus under control. This lengthened and deepened the UK downturn: GDP contracted by 22.1% from Q4 2019 to Q2 2020. This compares with a still-horrific but less dismal 15.2% in the Eurozone. GDP shrank by 10.2% in the US. However, unlike in Europe, major US states eased lockdowns before the virus was fully brought under control.

â Tough policy choices ahead: The UK government has two crucial policy choices to make before 2020 is over: 1) whether to make the necessary compromises in the ongoing UK-EU trade talks to secure a deal with its biggest trading partner in time for 1 January 2021 when it leaves the EU single market; and 2) whether to raise taxes or continue to provide generous fiscal support to the recovery in the Autumn Budget, due probably in November. Fortunately, we do not expect a serious fiscal tightening anytime soon. But on the downside, we doubt that the UK will make the necessary concessions to strike a deal with the EU. In case of a no-deal outcome, UK potential growth may fall to no more than 1.5%, versus 2.1% when the UK was a member of the EU. Unless Johnson softens his position fast to clear the way for an ambitious trade deal with the EU, the UK growth gap versus the US and Eurozone will likely persist for foreseeable future.

â A solid but poorly managed economy: UK economic fundamentals remain strong. A light-touch approach to regulation, rock-solid institutions like HM Treasury and the Bank of England, a pre-eminent financial sector, a legal system trusted around the world and world-class universities put the UK among the top countries in the advanced world for its supply potential. All of these factors predate the Brexit and Johnson era. Unfortunately, UK leaders currently seem to be doing more to undermine than to enhance these good fundamentals. An ideological approach to Brexit by many Conservatives and a questionable grasp of detail at the top are leading to policy choices with suboptimal results.

Chief Economist

+44 20 3207 7889

holger.schmieding@berenberg.com

Senior Economist

+44 20 3465 2672

kallum.pickering@berenberg.com

European Economist

+4420 3207 7859

![]()

Disclosures

This material is intended as commentary on political, economic or market conditions for institutional investors or market professionals only and does not constitute a financial analysis or a research report as defined by applicable regulation. See the "Disclaimers" section of this report.

The commentary included herein was produced by Joh. Berenberg, Gossler & Co. KG (Berenberg). For sales inquiries, please contact:

Phone: +44 (0)20 3207 7800

Email: berenberg.economics@berenberg.com

BERENBERG

Joh. Berenberg, Gossler & Co. KG

Neuer Jungfernstieg 20

20354 Hamburg

Germany

Registered Office: Hamburg, Germany

Local Court Hamburg HRA 42659

Any e-mail message (including any attachment) sent by Berenberg, any of its subsidiaries or any of their employees is strictly confidential and may contain information that is privileged or exempt from disclosure under applicable law. If you have received such message(s) by mistake please notify the sender by return e-mail. We ask you to delete that message (including any attachments) thereafter from your system. Any unauthorised use or dissemination of that message in whole or in part (including any attachment) is strictly prohibited. Please also note that any legally binding representation needs to be signed by two authorised signatories. Therefore we do not send legally binding representations via e-mail. Furthermore we do not accept any legally binding representation and/or instruction(s) via e-mail.

In the event of any technical difficulty with any e-mails received from us, please contact the sender or info@berenberg.com.

Click here to unsubscribe from these emails.