Click here for full report and disclosures

Click here to request a call about this note.

â The worst: Harsh lockdowns plunged much of the world into its deepest peacetime recession in early 2020. Even worse, the COVID-19 pandemic continues to take a devastating toll in terms of lost and impaired human lives. The current spread of a new variant of the virus in the UK and beyond illustrates the potential risks that still lie ahead.

â The best: Never before did mankind get its act together so fast in a global emergency, with medical progress spanning many frontiers. Take the example of the first vaccine approved in the advanced world. Developed by a small German biotech company run by two scientists of Turkish migrant stock, a US pharma giant gave it the required scale. Tested partly in Brazil, a Belgian production site shipped it instantly for first use in the UK. More vaccines are being approved or tested. This bolsters the hope that the pandemic can be brought under control in 2021. Helped by warmer weather that slows the spread of the virus, the worst should hopefully be over in the Northern Hemisphere by April.

â Getting it mostly right: Policymakers deserve some praise as well. By and large, central banks, finance ministers and regulators reacted fast and effectively. Despite a plunge in output by up to 30% within two months and a bout of serious financial turmoil in early March, the world did not descend into a genuine financial crisis. Relative to the severity of the shock, the hit to employment remained modest or â in the US â started to reverse fast. Massive fiscal survival support limited the damage to household and corporate balance sheets. By and large, science and reason trumped populism.

â Strong growth from spring onwards: Helped by record policy support, economic activity rebounded astonishingly fast once restrictions were eased from May to October. This bodes well for 2021. Once the current wave of the pandemic has run its course, we expect activity to expand rapidly from Q2 2021 onwards. Our calls for gains in real GDP in 2021 of 5.0% in the US and the Eurozone, 3.4% in Japan and 7.3% in the UK are well above the Bloomberg consensus â see Forecasts.

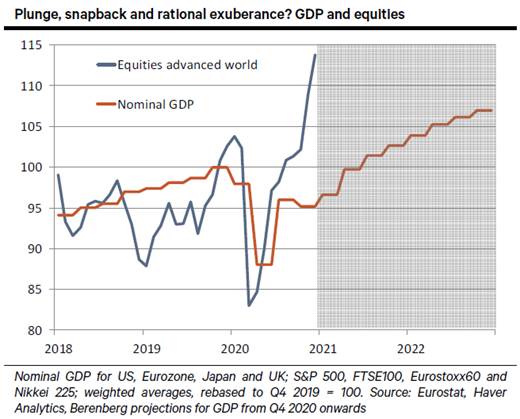

â And the bounciest: After markets collapsed when the pandemic spread to Europe and the US in early March, they began to anticipate the economic rebound to come from late March. While we had labelled the scale of the March plunge in markets an irrational panic, the extent of the subsequent surge surprised even optimists like us. Despite a pre-Christmas correction, markets have moved ahead of our bullish projections for nominal GDP in the advanced world â see chart.

â Positive outlook â with a snag: Two factors underpin the rational exuberance, even if it is now tempered by the latest virus news. First, after the 2020 recession, markets are now in the early phase of a new cycle rather than the late stage of an aging cycle. Investors can look forward to years of solid growth with record monetary and fiscal support. Second, inflation and interest rates look set to remain on a lower trajectory than before for a few years. Our above-consensus calls for economic growth justify some upside for risk assets and a further flow of money out of safe havens such as the US dollar into other currencies in 2021. But the outlook comes with a warning: the sweet spot of the cycle will not last forever. Once inflation returns more than just modestly, as it will eventually, markets will no longer outperform economic activity.

â After an unusually eventful 202o, we wish all our readers some rest and, most importantly, good health for 2021.

Chief Economist

+44 20 3207 7889

holger.schmieding@berenberg.com

Senior Economist

+44 20 3465 2672

kallum.pickering@berenberg.com

Florian Hense

European Economist

+4420 3207 7859

![]()

Disclosures

This material is intended as commentary on political, economic or market conditions for institutional investors or market professionals only and does not constitute a financial analysis or a research report as defined by applicable regulation. See the "Disclaimers" section of this report.

The commentary included herein was produced by Joh. Berenberg, Gossler & Co. KG (Berenberg). For sales inquiries, please contact:

Phone: +44 (0)20 3207 7800

Email: berenberg.economics@berenberg.com

BERENBERG

Joh. Berenberg, Gossler & Co. KG

Neuer Jungfernstieg 20

20354 Hamburg

Germany

Registered Office: Hamburg, Germany

Local Court Hamburg HRA 42659