Click here for full report and disclosures

Click here to request a call about this note.

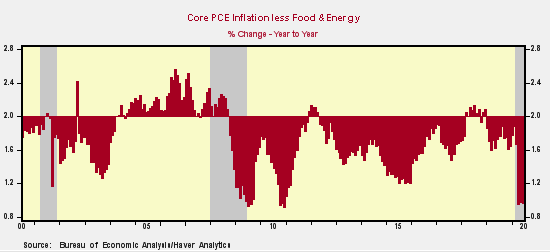

â Chair Powellâs announced new strategic framework for the Fed introduces significant changes in the conduct of monetary policy that reinforce sustained ease. In an explicit effort to provide support for strong labor markets for âall American citizens,â the Fed will now flexibly target a 2% average inflation and, importantly, it will no longer tighten policy pre-emptively in anticipation of rising inflation. Since the Fed established 2% as its inflation target in January 2012, inflation has been nearly persistently sub-2%, so the FedÂfs new Âgmake-up strategyÂh suggests that it favors inflation above 2% for years to come. The FedÂfs not-so-subtle changes are both a reflection of its recent behavior and represent a significant shift in official strategy.

â No discussion of the Fedâs monetary policy tools. Powell did not discuss what tools the Fed would use to achieve its new strategy. He mentioned the importance of communications, but did not provide any detail.

â The Fedâs focus will be providing support to strong labor markets subject to a flexible inflation constraint. Powell makes it clear the Fedâs aim is to conduct monetary policy that supports maximum and inclusive employment, and that it will aggressively pursue this goal until – and after – inflation and inflationary expectations rise above 2% – that is, until they become a problem.

â Underlying rationale: the Fed now perceives the Phillips Curve is FLAT until proven otherwise. In recent years, the Fed has said the trade-off between the unemployment rate and inflation has become flatter. The FedÂfs belief now is that strong employment can be consistent with stable inflation. Accordingly, maximum employment becomes the dominant mandate for monetary policy as the Fed hopes inflation rises above 2% and makes up for its recent shortfalls.

â The critical issue the Fed has not answered is: why has the FedÂfs monetary ease since the financial crisis failed to stimulate economic activity sufficiently to lift inflation to 2%? Over the years, the Fedâs arguments that the Phillips Curve has become flatter has been an ex post rationale for the persistence of low inflation consistent with low unemployment. But it reflects the FedÂfs lack of understanding of the actual inflation process. In reality, inflation has remained sub-2% because the FedÂfs policies have failed to stimulate a persistent increase in nominal GDP above productive capacity, so that, with little excess demand, there is only modest inflation. So the issue remains: will the FedÂfs ultra-easy policies actually stimulate accelerating economic activity, or just pump up asset prices and make the stock market happy?

â The FedÂfs new strategic framework supports higher stocks and a weaker U.S. dollar.

Chief Economist US, Americas and Asia

+1 646 445 4842

Economist

+1 646 949 9098

Disclosures

The research report included herein was prepared by Berenberg Capital Markets LLC (BCM) for institutional investors only and is distributed by Joh. Berenberg, Gossler & Co. KG (Berenberg) on a third-party basis in certain non-US & Canadian jurisdictions. For sales and trading inquiries, please contact:

BERENBERG

Joh. Berenberg, Gossler & Co. KG

Neuer Jungfernstieg 20

20354 Hamburg

Germany

Registered Office: Hamburg, Germany

Local Court Hamburg HRA 42659

Any e-mail message (including any attachment) sent by Berenberg, any of its subsidiaries or any of their employees is strictly confidential and may contain information that is privileged or exempt from disclosure under applicable law. If you have received such message(s) by mistake please notify the sender by return e-mail. We ask you to delete that message (including any attachments) thereafter from your system. Any unauthorised use or dissemination of that message in whole or in part (including any attachment) is strictly prohibited. Please also note that any legally binding representation needs to be signed by two authorised signatories. Therefore we do not send legally binding representations via e-mail. Furthermore we do not accept any legally binding representation and/or instruction(s) via e-mail.

In the event of any technical difficulty with any e-mails received from us, please contact the sender or info@berenberg.com.

Click here to unsubscribe from these emails.