|

| | | | Today, we’ve got a special Deep Dive to share with you. | Deep Dives are teardowns of interesting companies. They’re designed to illuminate the pros & cons and help you with your investment research. | Today’s issue is on Destiny. The world’s first ETF for shares of pre-IPO startups. This is a very big deal! | As always, we think you’ll find it informative and fair. Read the full issue here. |

| |

| | |

|

It’s no secret that private startups have a potential for wealth generation that public companies simply can’t match: |

Historically, investors who participated in a venture round of an company that IPO'd have received avg annualized returns from 50-100%. But for investors who purchased shares on the first public trading day, the average return shrinks to almost nothing (and often goes negative)

|

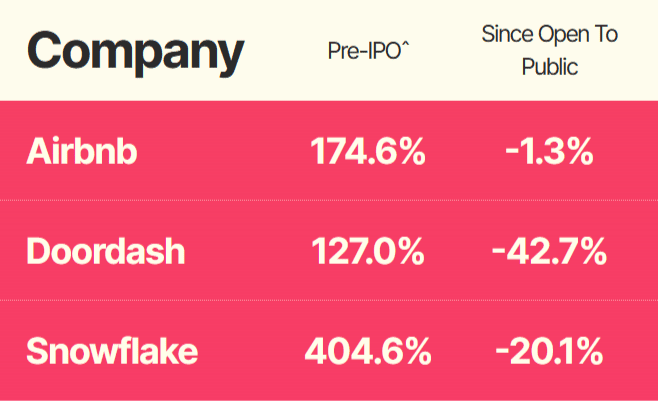

| Some of the most iconic IPOs of the past few years were insanely lucrative for early investors, but not so much for everyone else. |

|

In years gone by, world-changing companies like SpaceX, Stripe, and OpenAI would already be public by now. |

(Remember, Google's massive IPO took place just six years after its founding, younger than all three companies listed.) |

But with companies staying private for longer, everyday investors have basically lost access to venture-backed startups. Only wealthy, well-connected individuals and platforms can get access. |

You could argue the best solution here its to create a publicly-traded fund for pre-IPO shares. Shares that you can buy through your brokerage account. Shares that anyone can invest in... |

And there's only one company doing this: They're called Destiny, and they're the subject of today's issue. |

Let’s go 👇 |

Why private stock markets don't cut it |

Traditionally, investing in secondaries through private stock markets has been one way to bridge this gap. But there are a few reasons to think this isn’t really the best solution for investing in private companies. |

On the surface, building a "stock market for secondaries" seems like an excellent way to let investors access late-stage, venture-backed companies. |

But this approach doesn’t solve some of the fundamental problems with investing in private companies. |

Accreditation restrictions are a huge issue |

A private stock market might make it easier to trade secondaries, but these platforms can only be used by accredited investors (typically those with an income of $200k+ or net worth of $1m+) |

Since qualification as an accredited investor is the fundamental legal restriction barring most people from purchasing private investments, secondaries markets can never be a universal solution. |

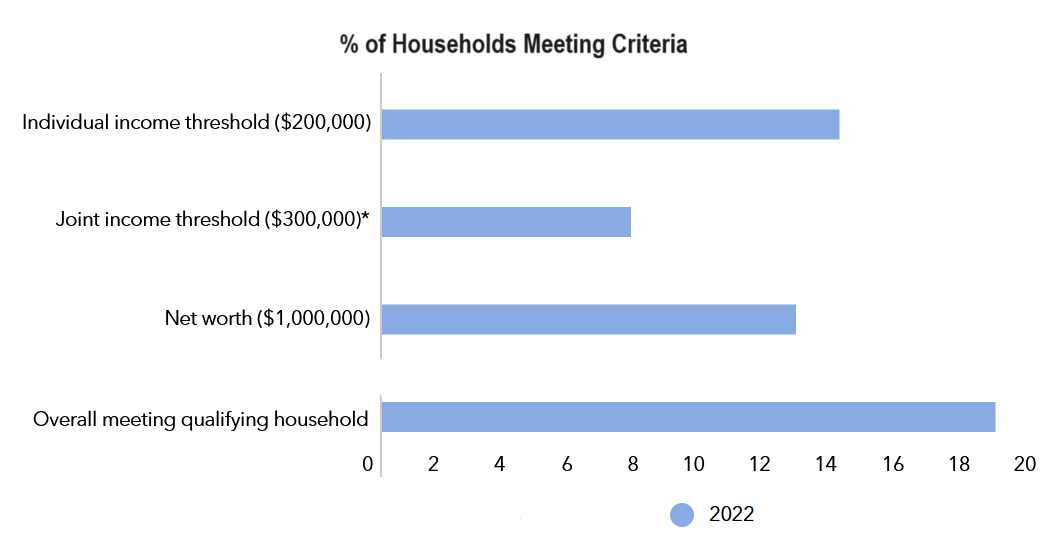

| As of 2022, only about 19% of households in the US actually met accreditation criteria – meaning private stock markets can only be used by about a fifth of the country. Image: Private Funds CFO |

|

Private companies aren’t easy to vet |

Vetting promising startups and deciding which ones to invest in is literally a full-time job. |

Despite this, everyday investors are pretty much expected to fend for themselves in private markets — and often with almost no financial statements or company material to actually analyze. (After all, private companies don’t have the same disclosure and reporting requirements as public ones) |

Diversification is very challenging |

In private markets, you usually need to invest $10,000 or more. |

Some platforms focusing exclusively on transactions in the range of $50,000 - $100,000+. |

What’s more, some high-demand investments (like say, SpaceX) can be assigned custom minimums, often reaching up to $1 million. And brokerage commissions to close these deals can be 5% or more. |

That makes assembling a suitably diverse portfolio of secondaries an expensive task. Most investors don't do this, and end up over-concentrated in just a few companies. |

Liquidity is still pretty rough |

Finally, even though private markets improve liquidity for startup shares, secondary shares still don’t trade very often. This means it's hard to track their current value, let alone cash out. |

Clearly, private secondaries markets are far from perfect. Using them only makes sense for a specific kind of investor: one who is: active, rich, and ultra-hands-on. |

Thankfully, in a few short months, investors are getting access to a better option — DXYZ. |

D/XYZ (Destiny): A breakthrough company |

DXYZ will be the first public, exchange-listed portfolio of hand-picked venture-backed private technology companies (!) |

For the first time, investors can get access to the late-stage startups like SpaceX, Stripe, and OpenAI on the public markets. |

| For the first time, investors will be able to purchase shares of pre-IPO startups through their brokerage account, just like any other public stock or fund. This is a very big deal. |

|

D/XYZ (pronounced Destiny, the actual team behind this) is planning to list this offering on the New York Stock Exchange in March 2024 under the ticker DXYZ. |

And considering that founder Sohail Prasad literally founded and led a private secondaries market (Forge), DXYZ is clearly informed by the shortcomings of that model. |

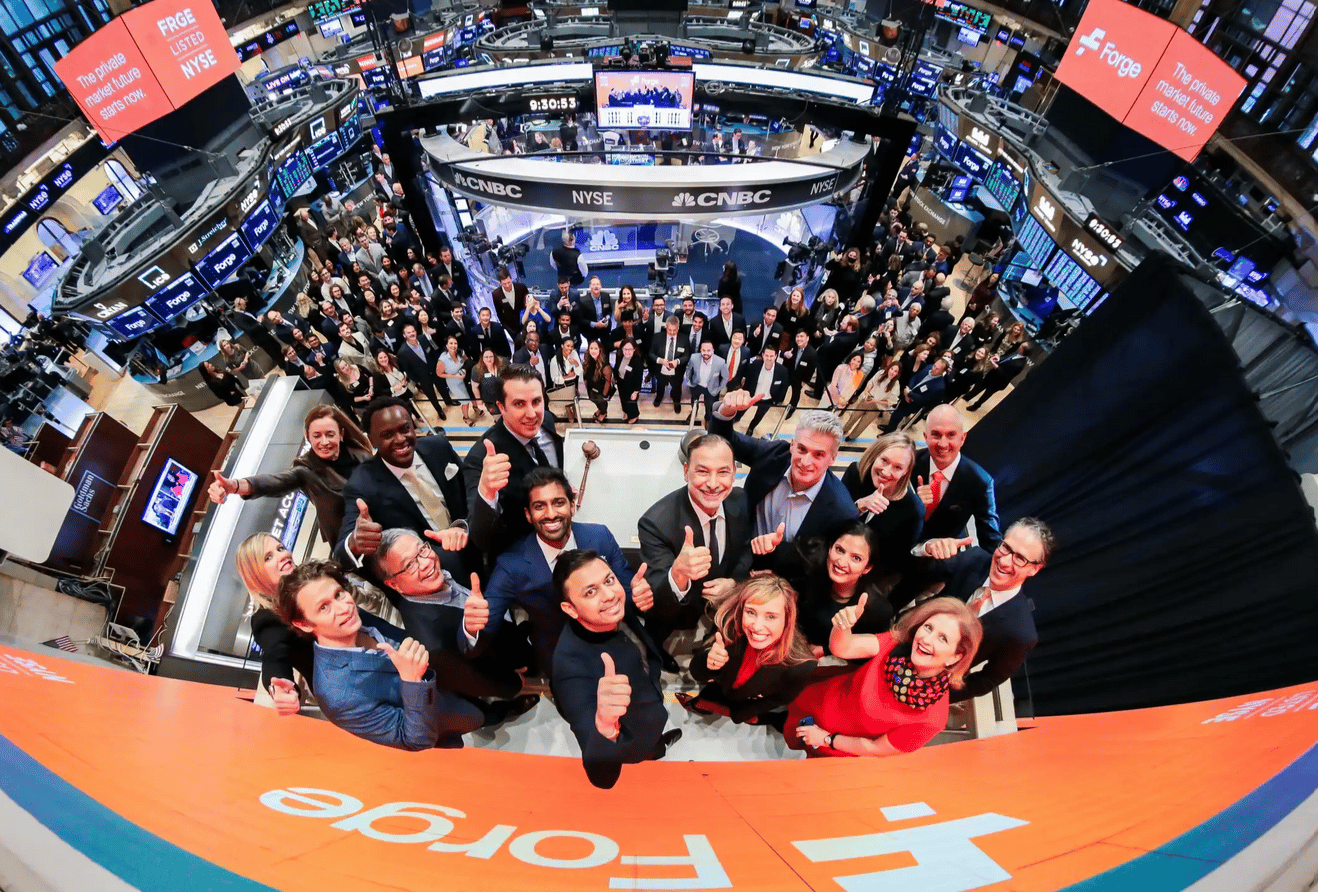

| D/XYZ Founder & CEO Sohail Prasad (bottom center) previously founded and led Forge, seen here at their 2022 IPO. |

|

Destiny's approach |

No accreditation restrictions |

It’s a public product, after all. |

Everyone can participate — no wealth barriers. (Huge!) |

No minimums |

Unlike the restrictive minimums of private secondaries markets, you can invest pretty much whatever you want in DXYZ |

This is basically the only way to invest in SpaceX with your spare cash. |

Plus, making automated investments through a brokerage account is way easier than through a secondaries market, allowing you to make private investing a recurring part of your strategy. |

Strictly vetted companies |

DXYZ has some specific eligibility criteria for companies to be included in the portfolio, including: |

Venture-backed At least $50 million in investment by reputable US institutions. Sound financial structure, including healthy liquidity and no burdensome debt. No unusually high executive turnover or other cultural red flags. And no risky foreign legal structures. (Looking at you, Chinese VIEs...)

|

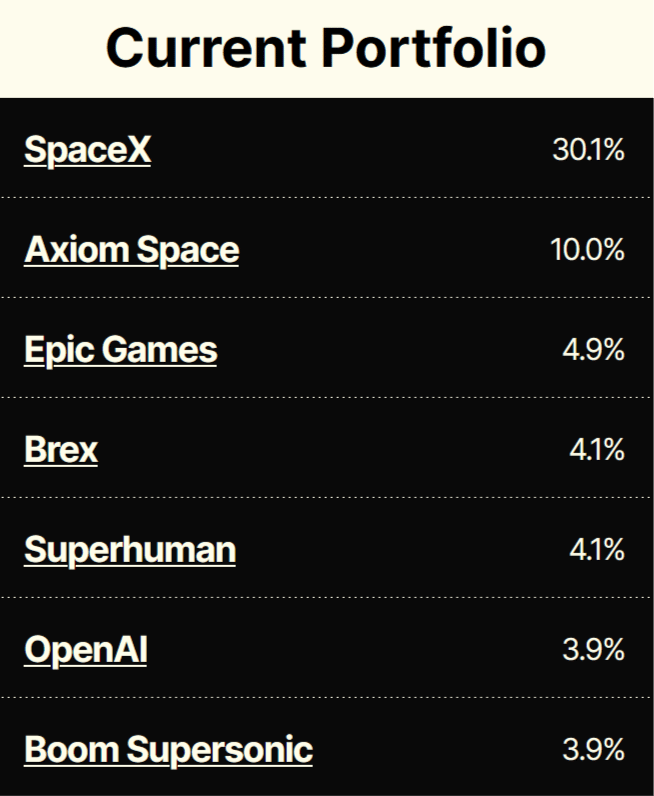

| The top holdings (by weighting) in the current DXYZ portfolio – these aren’t just random unvetted startups, but some of the most well-known private firms in the world. See full portfolio |

|

Broad portfolio construction |

Instead of needing to assemble a broad portfolio piece-by-piece, DXYZ investors can get access to a mix of venture-backed startups with just one purchase. |

The current portfolio includes 23 late-stage companies from a range of industries (although the team eventually hopes to build that up to 100) |

This approach is closer to the passive, index-oriented style of investing that many investors prefer, especially as active stock picking has fallen out of favor (although DXYZ isn’t actually designed to follow an underlying index). |

Strong liquidity (finally!) |

By virtue of listing on a centralized public market like the NYSE, DXYZ will have vastly increased liquidity when compared to the underlying companies. |

Not only does this make it relatively easier to liquidate your position than in private markets, but it allows you to better track the market value of your shares over time — meaning you actually know how much your investment is worth. |

Does DXYZ have competition? |

Here’s the thing: the whole fund-based approach has actually been tried before, with a number of investment funds promising access to a portfolio of private companies or startups in some form. |

These include The Private Shares Fund, the Fundrise Innovation Fund, and the ARK Venture Fund). |

How does DXYZ stack up to these direct competitors? |

DXYZ is truly public |

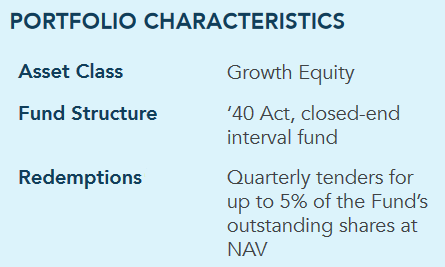

DXYZ is the first of these fund offerings to actually be a publicly listed fund — as opposed to industry-standard interval funds, which have investment minimums and only allow quarterly, partial cash-outs (usually only 5% of your shares can be redeemed per quarter.) |

The Private Shares Fund, for instance, has a $2,500 minimum investment and only offers liquidity on a quarterly basis. |

| The Private Shares Fund, a well-known peer to DXYZ, is an interval fund that relies on periodic “redemptions” to provide liquidity opportunities to its shareholders. This is in stark contrast to publicly-listed funds like DXYZ where investors can sell into the market. |

|

In contrast, the minimum investment in DXYZ is just the cost of a single share (launching at a nominal price of $8, not including any brokerage fees) and you can sell shares daily on the exchange (assuming, of course, that there’s sufficient demand). |

Having the choice to liquidate by selling shares isn’t just good for investment optionality, but also for peace of mind. |

Only private & proven companies are included |

Pretty much all of DXYZ’s competitors hold "private" shares in their funds. But there’s no consistency regarding what that means, nor what portion of the fund is actually private. |

DXYZ is clear that their fund is only interested in the "top 100 venture-backed private technology companies" on the market. |

Other funds vary, with portfolios including everything from public to private companies and early-stage to late-stage startups. |

| The ARK Ventures fund portfolio is wide-ranging, to say the least, with public companies (like Tesla) alongside both early-stage startups (like Pave Financial) and late-stage ones (like Discord). In contrast, DXYZ holds just Discord and Axiom Space out of the above ARK sample. |

|

If you’re interested in either ultra-early-stage or public companies, DXYZ probably isn’t for you. |

But just understand that by focusing on a curated subset of private companies, the DXYZ portfolio is far more tailored than other approaches. |

|

We’re out of space! Read the rest of this issue on the web. |

Disclosures |

This issue was sponsored by Destiny The ALTS 1 Fund holds no interest in any companies mentioned in this issue. This issue contains no affiliate links

|

This issue is a sponsored deep dive, meaning Alts has been paid to write an independent analysis of Destiny and their associated markets. Destiny has agreed to offer an unconstrained look at its business, offerings, and operations. Destiny is also a sponsor of Alts, but our research is neutral and unbiased. This should not be considered financial, legal, tax, or investment advice, but rather an independent analysis to help readers make their own investment decisions. All opinions expressed here are ours, and ours alone. We hope you find it informative and fair. |

|

|