| -- | August 22, 2017 How American Blood Can Fill the Trade Deficit By Patrick Watson In June, the US ran a $32.6 billion “trade in goods” deficit with China. That’s the difference between our imports from China ($42.3 billion) and our exports to China ($9.7 billion), according to the US Census Bureau. That sounds terrible, but it’s really not if you look at the big picture. Double-entry accounting includes flows of both goods and capital. The current account deficit (another name for the trade deficit) is simply the other side of a capital account surplus. The two always reconcile to zero—hence the name, “balance of payments.” Nonetheless, the Trump administration doesn’t like trade deficits, so they must be reduced or eliminated. To do that, we need Chinese consumers to buy more “Made in the USA” products. Problem is, China has little need for US-manufactured products, beyond the agricultural goods it already buys. They would buy certain things we refuse to sell them, like defense technology. What else can we send? Here’s an idea President Trump should consider.

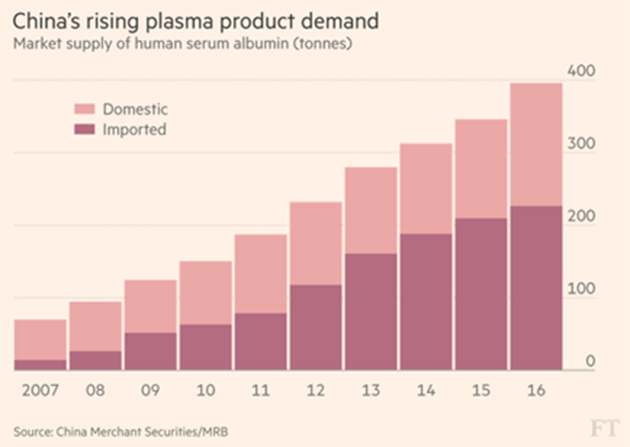

AP photo China-Sized Liver Problems Everything about China is big—including its health problems. According to the World Health Organization, about 100 million Chinese have some form of chronic hepatitis. That’s one in 13 people. Hepatitis can lead to liver cirrhosis and liver cancer, so this is a serious problem. Treating it requires serum albumin, a substance found in human blood plasma. As the Financial Times reported last week, Chinese patients consumed 300 metric tons of serum albumin in 2016, approximately half of the global total. Now, while the necessary supply could be provided by the Chinese population, many of them are afraid to donate blood. The reason is a well-remembered 1990s health scare in which tens of thousands of farmers who had been paid to donate blood acquired HIV from unsanitary needles. The ensuing scandal was covered up by the government. As a result, China has to import about 60% of its serum albumin—and the ever-rising demand has driven up prices. Hepatitis patients are not the only buyers, either. FT reports: Widespread misconceptions about blood injections as an elixir of youth have also boosted Chinese demand. “Some Chinese people have an unscientific idea that human albumin is a nutritious product, and some wealthy or privileged consumers such as retired officials demand it,” said Xu Xianming, an administrator at a Shanghai hospital. This “unscientific idea” may not be unscientific at all, by the way. In recent years, some Western scientists found that injecting older test subjects with a certain protein found in youthful blood can delay and possibly even reverse the effects of aging. Animal studies have already been vastly successful. But I digress. In any case, it’s probably bullish for serum albumin prices if wealthy Chinese want to buy large amounts.  American Edge According to the Financial Times article (FT subscribers can read it here), three foreign companies currently account for 88% of China’s serum albumin imports. They are: - Baxalta, now owned by Shire Pharmaceuticals (SHPG)

(Disclaimer: This is not a stock recommendation. Please do your own research before you buy any of these.) Interestingly, even though CSL is an Australian company and Grifols is from Spain, all three collect most of their plasma in the US. That suggests we have some natural advantage. Total US blood plasma collection was 31,000 metric tons last year, compared to only 7,000 metric tons collected in China—even though China has four times as many people. Clearly, Americans have an edge in this business. We could amplify it by ramping up blood plasma collection to keep pace with rising Chinese demand. This would help reduce the trade deficit and might have other benefits too. To give blood, you must be in generally good health. That may incentivize donors (who are often paid for giving blood) to avoid unhealthy lifestyle choices, which in turn could result in lower healthcare expenditures as a side benefit. Another advantage: blood plasma offers high value for its volume and weight. One refrigerated container might be worth more than an entire shipload of grain, for instance. We’d be able to boost exports with minimal extra carbon emissions. Risk Factors Every business plan has to ask, “What could go wrong?” In this case, one obvious risk is competition. Americans aren’t the only ones with blood to sell, so other countries could underbid the US. In addition, researchers in China and elsewhere are working on artificially produced serum albumin. One Chinese project using rice seeds has proven safe and effective in initial trials. These are indeed risks, but I think they’re minimal for now. The US can maintain its edge as long as we maintain high quality.  President Trump loves to make deals. I think this is a natural one he could negotiate with President Xi. - The Chinese can get all the made-in-America blood plasma they need, saving many lives.

- US healthcare spending will fall.

- The US-China trade deficit will shrink.

See, everybody wins. What’s not to like? Regular readers know I’m very concerned about the Trump administration setting off an economically destructive trade war. I hope it doesn’t happen, but I think investors should prepare for it. International trade doesn’t have to create winners and losers. Voluntary exchange is good for everyone. See you at the top,  Patrick Watson P.S. If you’re reading this because someone shared it with you, click here to get your own free Connecting the Dots subscription. You can also follow me on Twitter: @PatrickW.  | Subscribe to Connecting the Dots—and Get a Glimpse of the Future

We live in an era of rapid change… and only those who see and understand the shifting market, economic, and political trends can make wise investment decisions. Macroeconomic forecaster Patrick Watson spots the trends and spells what they mean every week in the free e-letter, Connecting the Dots. Subscribe now for his seasoned insight into the surprising forces driving global markets. |

Senior Economic Analyst Patrick Watson is a master in connecting the dots and finding out where budding trends are leading. Patrick is the editor of Mauldin Economics’ high-yield income letter, Yield Shark, and co-editor of the premium alert service, Macro Growth & Income Alert. You can also follow him on Twitter (@PatrickW) to see his commentary on current events. Senior Economic Analyst Patrick Watson is a master in connecting the dots and finding out where budding trends are leading. Patrick is the editor of Mauldin Economics’ high-yield income letter, Yield Shark, and co-editor of the premium alert service, Macro Growth & Income Alert. You can also follow him on Twitter (@PatrickW) to see his commentary on current events.

Share Your Thoughts on This Article

Use of this content, the Mauldin Economics website, and related sites and applications is provided under the Mauldin Economics Terms & Conditions of Use. Unauthorized Disclosure Prohibited The information provided in this publication is private, privileged, and confidential information, licensed for your sole individual use as a subscriber. Mauldin Economics reserves all rights to the content of this publication and related materials. Forwarding, copying, disseminating, or distributing this report in whole or in part, including substantial quotation of any portion the publication or any release of specific investment recommendations, is strictly prohibited.

Participation in such activity is grounds for immediate termination of all subscriptions of registered subscribers deemed to be involved at Mauldin Economics’ sole discretion, may violate the copyright laws of the United States, and may subject the violator to legal prosecution. Mauldin Economics reserves the right to monitor the use of this publication without disclosure by any electronic means it deems necessary and may change those means without notice at any time. If you have received this publication and are not the intended subscriber, please contact service@mauldineconomics.com. Disclaimers The Mauldin Economics website, Yield Shark, Thoughts from the Frontline, Patrick Cox’s Tech Digest, Outside the Box, Over My Shoulder, World Money Analyst, Street Freak, Just One Trade, Transformational Technology Alert, Rational Bear, The 10th Man, Connecting the Dots, This Week in Geopolitics, Stray Reflections, and Conversations are published by Mauldin Economics, LLC. Information contained in such publications is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The information contained in such publications is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. The information in such publications may become outdated and there is no obligation to update any such information. You are advised to discuss with your financial advisers your investment options and whether any investment is suitable for your specific needs prior to making any investments.

John Mauldin, Mauldin Economics, LLC and other entities in which he has an interest, employees, officers, family, and associates may from time to time have positions in the securities or commodities covered in these publications or web site. Corporate policies are in effect that attempt to avoid potential conflicts of interest and resolve conflicts of interest that do arise in a timely fashion.

Mauldin Economics, LLC reserves the right to cancel any subscription at any time, and if it does so it will promptly refund to the subscriber the amount of the subscription payment previously received relating to the remaining subscription period. Cancellation of a subscription may result from any unauthorized use or reproduction or rebroadcast of any Mauldin Economics publication or website, any infringement or misappropriation of Mauldin Economics, LLC’s proprietary rights, or any other reason determined in the sole discretion of Mauldin Economics, LLC. Affiliate Notice Mauldin Economics has affiliate agreements in place that may include fee sharing. If you have a website or newsletter and would like to be considered for inclusion in the Mauldin Economics affiliate program, please go to http://affiliates.ggcpublishing.com/. Likewise, from time to time Mauldin Economics may engage in affiliate programs offered by other companies, though corporate policy firmly dictates that such agreements will have no influence on any product or service recommendations, nor alter the pricing that would otherwise be available in absence of such an agreement. As always, it is important that you do your own due diligence before transacting any business with any firm, for any product or service. © Copyright 2017 Mauldin Economics | -- |