| -- | December 5, 2017 How Tax Cuts Will Trigger Recession By Patrick Watson According to the more cynical pundits, government programs usually achieve the opposite of their intended goal. And sometimes they do. For example, Richard Nixon’s “War on Drugs” is still in progress, but the drugs are definitely winning. Some government programs, however, are more effective. Firefighters are doing a pretty good job extinguishing fires. The US Coast Guard saves lives every day. Public school teachers educate students who would rather be elsewhere. And then there’s our increasingly dysfunctional Congress. Where to begin? I’ve written recently how Congress’s new tax plan misses a chance to boost economic growth. Now I think it may be even worse. Instead of merely failing to stimulate growth, the tax changes could actually launch a recession. I’ll tell you why in a moment. But first, a quick reminder: our Mauldin Economics VIP program is open to new members until December 13. VIP members get all our premium investment services, including my own Yield Shark and Macro Growth & Income Alert, for one low price. I suspect they’ll be even more useful if we go into recession, so click here to learn more.

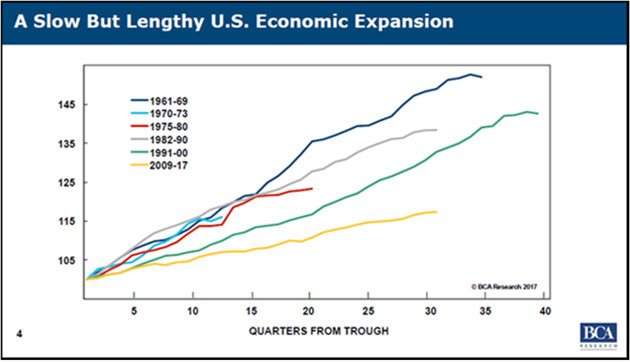

Image: Renegade98 via Flickr Long and Weak Expansion I explained two weeks ago why tax cuts won’t stimulate the economy as much as Republican lawmakers think. Most CEOs say they will use any tax savings for stock buybacks or dividends, not new hiring or expansion. Since then, the Joint Committee on Taxation, Congress’s nonpartisan scorekeeper, found the Senate tax bill would spur only 0.8% of economic growth, split over 10 years, and add a net $1 trillion to the national debt. But let’s set aside debt for now. What if, instead of little or no growth, this tax bill sets off an outright contraction? The current economic expansion is now the third-longest since World War II. It’s also the weakest. Here’s a chart I showed last summer.

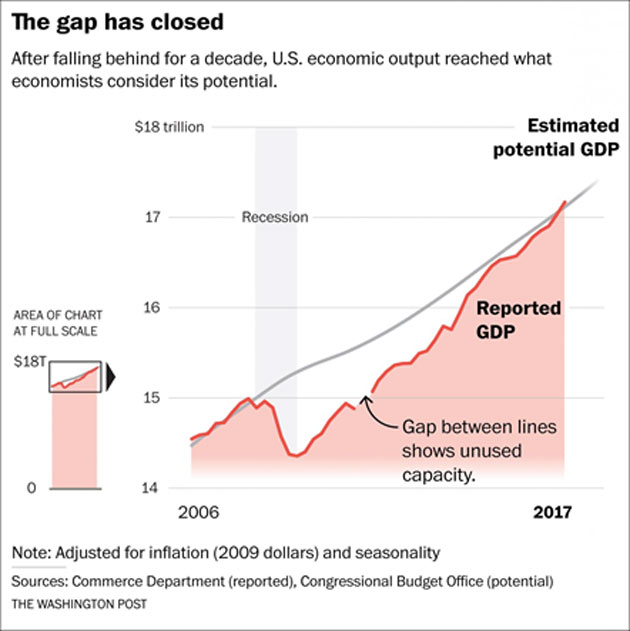

Source: BCA Research The yellow line is the current recovery that began in 2009. Only the 1960s and 1990s growth periods went on longer—and both had much higher growth. So, just by length of time, we’re already due or overdue for recession. Yes, the economy could improve further from here… but probably not for long. Potential Achieved Last week, the Commerce Department revised its third-quarter inflation-adjusted GDP estimate to a 3.3% annualized pace. While that was good news, it also marked something ominous. In addition to actual gross domestic product, economists track “Potential GDP.” That’s how fast the economy is capable of growing, considering the number of available workers, productivity, and other factors. If subsequent data confirms last quarter’s 3.3% growth, it will mark the first time since 2007 the US economy achieved “maximum sustainable output.”

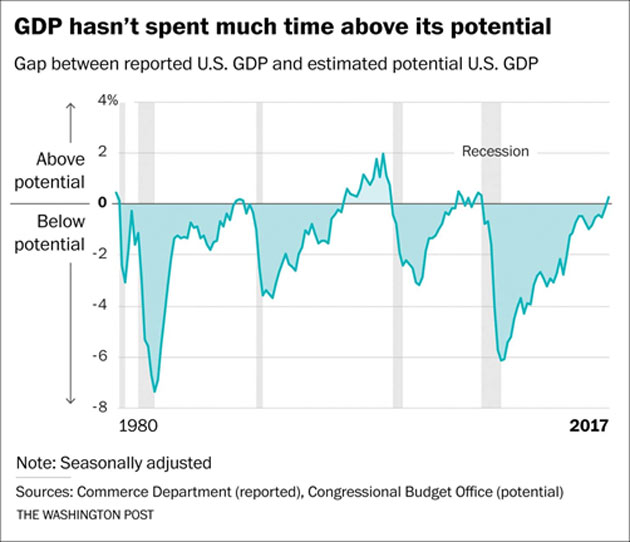

Image: Washington Post The gap between the gray line (potential GDP) and the red line (actual GDP) represents unused capacity. You can see we had a lot of it at the recession’s 2009 depth. The gap slowly shrank since then. Now it’s closed. Great news, right? Yes, it is—but don’t celebrate just yet. The End Is Near Actual GDP can’t stay above potential GDP for long before bad things start happening. This chart proves it:

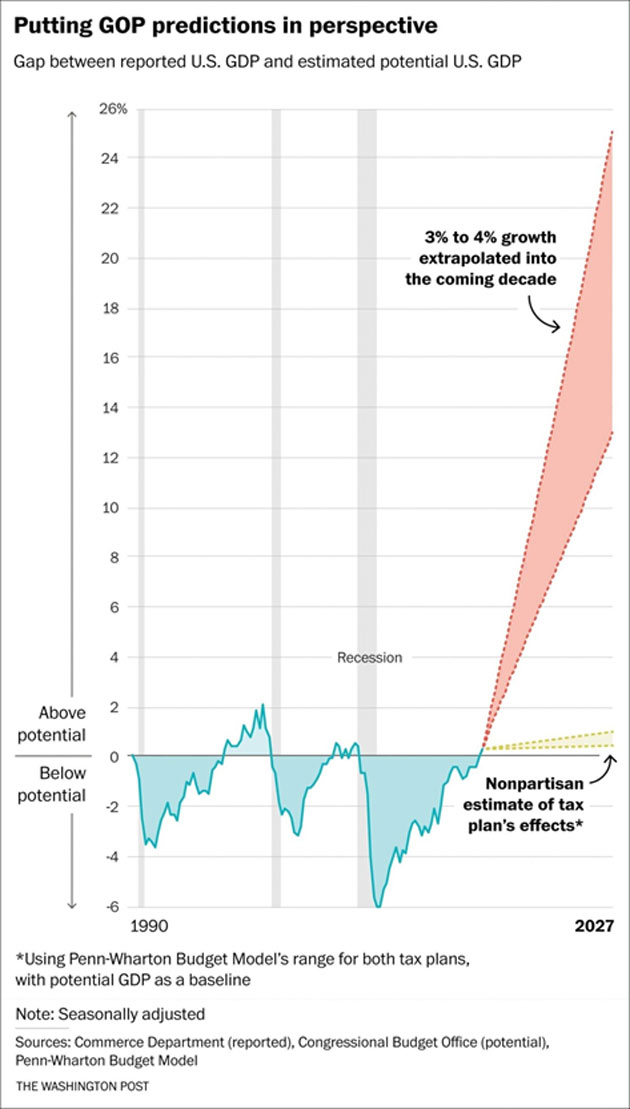

Image: Washington Post We see here how GDP moved above and below its potential since the 1970s. Notice that each time the green line went above zero, a recession (the gray bars) began soon after. “Soon” can vary, of course. GDP ran above potential for extended periods in the late 1990s and 2006–2007, but in both cases, intense downturns followed. Plus, the Fed wasn’t tightening as it is now—which suggests the current expansion is at least approaching its endpoint. The Trump administration and congressional Republicans disagree, saying their tax changes will stimulate years of economic growth and more than pay for themselves. President Trump himself said last month he thought growth could reach 4% and even “quite a bit higher.” I agree we may get a quarter or two of 4% real annualized growth. But will it continue for years? Probably not, unless potential GDP takes a big leap. Here is the potential GDP chart above, extrapolating the future as it would look with 3–4% growth over the next decade.

Image: Washington Post I’m sorry this chart is so tall, but that red triangle is necessary to project as much growth as the president anticipates and that Congress says will pay for the tax cuts. The smaller yellow fan below it is the less thrilling estimate of nonpartisan economists. In either case, to do what the Republicans predict, GDP must grow above potential for years, unless potential GDP rises in a similarly spectacular fashion. That’s not impossible: a major technology breakthrough might do it, say, a cure for cancer that frees up more workers, or wearable supercomputers to make workers more productive. But just as likely, a recession, natural disaster, war, or other shock could sharply reduce GDP. The projections above don’t account for that possibility. Booms Going “Boom” Actual GDP can outpace potential GDP at the end of a cycle, but by definition, such growth is unsustainable. The inputs to higher production—available workers, productivity—can’t grow fast enough, so those booms end up going “boom.” Now consider what else is happening. The Federal Reserve is in tightening mode, both raising short-term interest rates and reducing its massive balance sheet assets. Fed officials think the economy is close to full employment, and they want to control inflation pressure before it gets out of hand. If this tax cut finally passes—and I’m still dubious that it will—I don’t think it will create anything like 3–4% GDP growth. I think it will do the opposite, as the US Treasury borrows hundreds of billions more dollars to cover deficit spending. That will drive rates higher; not good for real estate or consumer spending. Much like the War on Drugs gave us more drugs, the “War on Slow Growth” might give us even slower growth.

Image: Danlele Pesaresi via Flickr Recession Triggers Here’s where we are: - The current expansion is long in the tooth, suggesting a recession could start anytime

- GDP growth is running above potential, which also points to recession in the near future

- The Fed is tightening, soon to be joined by other central banks

- Treasury borrowing will likely increase in the next few years as deficits rise

- Bitcoin and other cryptocurrencies look increasingly bubble-like

All that is happening even if we get no surprises. War with North Korea, a NAFTA breakup, Chinese banking crisis, a hard Brexit—any of those could extinguish global growth. My main fear as we entered 2017 was that the Fed would tighten too much and too fast, pushing the economy into a deflationary recession. I still think that’s the most likely scenario. If this tax bill passes in its current form, the recession may happen sooner and go deeper. The combined fiscal and monetary tightening could be the triggers. However, first we might get a sugar-high inflationary rally, which could last a while. GDP ran above potential for four years in the late 1990s, and for over a year in the housing craze. Those were fun times while they lasted. Then the fun stopped. One thing I’m positive won’t happen is another 10 years of uninterrupted 3% or 4% real GDP growth, as politicians so glibly promise. That’s pure fantasy. Gravity still applies, no matter how many people wish it didn’t. We may get a demonstration soon. See you at the top,  Patrick Watson P.S. If you’re reading this because someone shared it with you, click here to get your own free Connecting the Dots subscription. You can also follow me on Twitter: @PatrickW.  | Subscribe to Connecting the Dots—and Get a Glimpse of the Future

We live in an era of rapid change… and only those who see and understand the shifting market, economic, and political trends can make wise investment decisions. Macroeconomic forecaster Patrick Watson spots the trends and spells what they mean every week in the free e-letter, Connecting the Dots. Subscribe now for his seasoned insight into the surprising forces driving global markets. |

Senior Economic Analyst Patrick Watson is a master in connecting the dots and finding out where budding trends are leading. Patrick is the editor of Mauldin Economics’ high-yield income letter, Yield Shark, and co-editor of the premium alert service, Macro Growth & Income Alert. You can also follow him on Twitter (@PatrickW) to see his commentary on current events. Senior Economic Analyst Patrick Watson is a master in connecting the dots and finding out where budding trends are leading. Patrick is the editor of Mauldin Economics’ high-yield income letter, Yield Shark, and co-editor of the premium alert service, Macro Growth & Income Alert. You can also follow him on Twitter (@PatrickW) to see his commentary on current events.

Share Your Thoughts on This Article

Use of this content, the Mauldin Economics website, and related sites and applications is provided under the Mauldin Economics Terms & Conditions of Use. Unauthorized Disclosure Prohibited The information provided in this publication is private, privileged, and confidential information, licensed for your sole individual use as a subscriber. Mauldin Economics reserves all rights to the content of this publication and related materials. Forwarding, copying, disseminating, or distributing this report in whole or in part, including substantial quotation of any portion the publication or any release of specific investment recommendations, is strictly prohibited.

Participation in such activity is grounds for immediate termination of all subscriptions of registered subscribers deemed to be involved at Mauldin Economics’ sole discretion, may violate the copyright laws of the United States, and may subject the violator to legal prosecution. Mauldin Economics reserves the right to monitor the use of this publication without disclosure by any electronic means it deems necessary and may change those means without notice at any time. If you have received this publication and are not the intended subscriber, please contact service@mauldineconomics.com. Disclaimers The Mauldin Economics website, Yield Shark, Thoughts from the Frontline, Patrick Cox’s Tech Digest, Outside the Box, Over My Shoulder, World Money Analyst, Street Freak, Just One Trade, Transformational Technology Alert, Rational Bear, The 10th Man, Connecting the Dots, This Week in Geopolitics, Stray Reflections, and Conversations are published by Mauldin Economics, LLC. Information contained in such publications is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The information contained in such publications is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. The information in such publications may become outdated and there is no obligation to update any such information. You are advised to discuss with your financial advisers your investment options and whether any investment is suitable for your specific needs prior to making any investments.

John Mauldin, Mauldin Economics, LLC and other entities in which he has an interest, employees, officers, family, and associates may from time to time have positions in the securities or commodities covered in these publications or web site. Corporate policies are in effect that attempt to avoid potential conflicts of interest and resolve conflicts of interest that do arise in a timely fashion.

Mauldin Economics, LLC reserves the right to cancel any subscription at any time, and if it does so it will promptly refund to the subscriber the amount of the subscription payment previously received relating to the remaining subscription period. Cancellation of a subscription may result from any unauthorized use or reproduction or rebroadcast of any Mauldin Economics publication or website, any infringement or misappropriation of Mauldin Economics, LLC’s proprietary rights, or any other reason determined in the sole discretion of Mauldin Economics, LLC. Affiliate Notice Mauldin Economics has affiliate agreements in place that may include fee sharing. If you have a website or newsletter and would like to be considered for inclusion in the Mauldin Economics affiliate program, please go to http://affiliates.ggcpublishing.com/. Likewise, from time to time Mauldin Economics may engage in affiliate programs offered by other companies, though corporate policy firmly dictates that such agreements will have no influence on any product or service recommendations, nor alter the pricing that would otherwise be available in absence of such an agreement. As always, it is important that you do your own due diligence before transacting any business with any firm, for any product or service. © Copyright 2017 Mauldin Economics | -- |