| -- | September 19, 2017 How to Beat Banks at Their Own Game By Patrick Watson When it comes to public sentiment, banks and Congress have a lot in common. People tell pollsters they dislike Congress in general, but they keep re-electing their own representative and senators. Similarly, people tend to like their own bank and disapprove of others, according to the latest American Banker/Reputation Institute survey. One glaring exception: Wells Fargo (WFC). Pretty much no one likes Wells Fargo since last year’s revelation that the bank’s staff had opened millions of false accounts to meet ambitious sales targets. I said at the time there’s never just one cockroach. Turn on the lights, and you’ll see more scurrying away. That proved true for Wells Fargo. It’s now embroiled in several other scandals, like forcing customers to buy car insurance they didn’t need. Other banks may have similar issues. The banking giants get away with these things because people feel powerless against them, but now there’s a new way to beat the banks at their own game—and keep some of those handsome profits for yourself.

Photo: AP Shedding Layers Economists love to use fancy words for simple concepts, like disintermediation. It simply means “removing intermediaries” or what we used to call “middlemen.” In the 1970s, if you needed a new refrigerator, you would buy one at your local appliance store. The store bought it from a wholesale distributor, which got it from a manufacturer’s rep, who took it on consignment from the manufacturer. Every one of those intermediaries had to make money. Today, if you want a refrigerator, you go to a big-box store like Sears (SHLD), Best Buy (BBY), or Home Depot (HD), or even order one from Amazon and save on shipping costs. The store—whether brick and mortar or online—acquired the fridge directly from the manufacturer. Two or three distribution layers are gone now. On balance, that’s a good thing. Extra layers are wonderful with dessert; for the economy, they’re not so sweet.

Photo: Kimberly Vardeman via Flickr Disintermediation allocates labor and capital more efficiently, helping the economy grow. Which brings us to banks. Being a middleman is the main reason banks exist. Their core function is to stand in between two groups: - People with money to lend

- People who need to borrow

Contrary to what many folks think, your savings account or certificate of deposit is not in the bank for safekeeping. It’s in the bank because the bank has borrowed your cash. That’s why deposits go on the liability side of the bank’s balance sheet. So if you have a bank account, you’re automatically a lender. You might also be a borrower if you have a credit card, mortgage, or auto loan. The bank profits by charging the borrower a higher interest rate than it pays the lenders (aka depositors). Say you get 1% on your CD, and the bank lends your cash to someone else for 7%. The difference between the two, the net interest margin, is how the bank makes its money. But what if there were a way for borrowers and lenders to find each other and cut out the middleman?

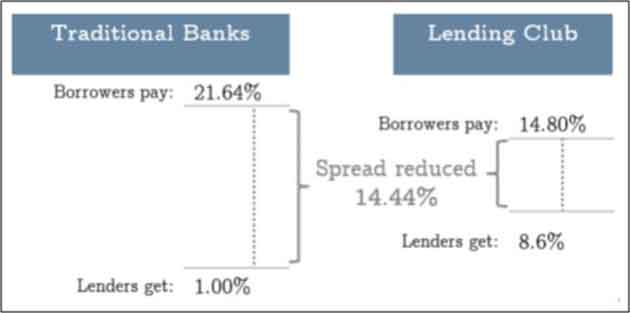

Photo: AP Peer to Peer The new way to be your own bank is as simple as it is ingenious. It’s called peer-to-peer (P2P) lending. Using any of several online platforms, both lenders and borrowers can transact loans directly. If you have money to lend, you can invest in a great variety of loans from prescreened borrowers. You can dial the risk level up or down by allocating to borrowers with higher or lower credit scores. Borrowers win too, by paying lower interest rates. The losers are banks, which don’t get their usual piece of the action. Here’s an illustration of the difference at Lending Club, one of the largest P2P platforms.

Source: HJCO Capital Partners With the bank out of the equation, the borrower’s rate drops and the lender’s return goes up. In this example, the net interest margin drops from 20.64% to only 6.2%. That’s disintermediation at work. The results aren’t always so dramatic, but it can still make a noticeable difference on both sides of a loan. And it can be a great portfolio diversifier if you already have stock or bond investments. Of course, rates go up and down over time, but P2P lending can earn investors a higher yield than most other fixed-income instruments, without higher risks. I know people who make 5–7% annual returns. 7% Yields in a 2% World Does P2P lending have a downside, compared to banks? Yes, and it’s a big one: deposit insurance. The FDIC won’t be there to save you if your loans default. On the other hand, you won’t have bankers taking crazy trading risks with your money, as often happens now. So that partially reduces the need for deposit insurance. Still, you don’t want to do this with money you absolutely can’t lose. If that’s your situation, better stick with insured banks. Liquidity is another issue. You make loans for fixed time periods, anywhere from a year up to five years. Your cash is tied up for the loan term. You might be able to sell your loans to another investor, but don’t count on it. You also depend on your borrowers to pay you back. They can always default, for all kinds of reasons. Maybe they lose their job or get hit by medical bills. Stuff happens. The platforms will help you try to collect, but it’s not guaranteed. And if we get into another recession, default rates will likely go up.  For more on P2P lending, check out my in-depth special report, The New Asset Class That Helps Investors Earn 7% Yields in a 2.5% World. For more on P2P lending, check out my in-depth special report, The New Asset Class That Helps Investors Earn 7% Yields in a 2.5% World. My colleague Stephen McBride and I pulled together all the background information you need to know, including specific tips to get you started. You can get your free copy of the report here. And just so you know: I am not getting paid by the P2P industry, so you won’t find a sales pitch for Lending Club or any of its competitors in the report. Personally, I like P2P lending because it’s a win-win for both lenders and borrowers. Sure, the banks don’t like this idea. But if your bank is like Wells Fargo, you don’t owe it any favors. See you at the top,  Patrick Watson P.S. We’ve also made a short (less than two minutes) YouTube video about P2P lending. You’ll see the highlights and then you can request the report to learn more. Click here to watch.  | Subscribe to Connecting the Dots—and Get a Glimpse of the Future

We live in an era of rapid change… and only those who see and understand the shifting market, economic, and political trends can make wise investment decisions. Macroeconomic forecaster Patrick Watson spots the trends and spells what they mean every week in the free e-letter, Connecting the Dots. Subscribe now for his seasoned insight into the surprising forces driving global markets. |

Senior Economic Analyst Patrick Watson is a master in connecting the dots and finding out where budding trends are leading. Patrick is the editor of Mauldin Economics’ high-yield income letter, Yield Shark, and co-editor of the premium alert service, Macro Growth & Income Alert. You can also follow him on Twitter (@PatrickW) to see his commentary on current events. Senior Economic Analyst Patrick Watson is a master in connecting the dots and finding out where budding trends are leading. Patrick is the editor of Mauldin Economics’ high-yield income letter, Yield Shark, and co-editor of the premium alert service, Macro Growth & Income Alert. You can also follow him on Twitter (@PatrickW) to see his commentary on current events.

Share Your Thoughts on This Article

Use of this content, the Mauldin Economics website, and related sites and applications is provided under the Mauldin Economics Terms & Conditions of Use. Unauthorized Disclosure Prohibited The information provided in this publication is private, privileged, and confidential information, licensed for your sole individual use as a subscriber. Mauldin Economics reserves all rights to the content of this publication and related materials. Forwarding, copying, disseminating, or distributing this report in whole or in part, including substantial quotation of any portion the publication or any release of specific investment recommendations, is strictly prohibited.

Participation in such activity is grounds for immediate termination of all subscriptions of registered subscribers deemed to be involved at Mauldin Economics’ sole discretion, may violate the copyright laws of the United States, and may subject the violator to legal prosecution. Mauldin Economics reserves the right to monitor the use of this publication without disclosure by any electronic means it deems necessary and may change those means without notice at any time. If you have received this publication and are not the intended subscriber, please contact service@mauldineconomics.com. Disclaimers The Mauldin Economics website, Yield Shark, Thoughts from the Frontline, Patrick Cox’s Tech Digest, Outside the Box, Over My Shoulder, World Money Analyst, Street Freak, Just One Trade, Transformational Technology Alert, Rational Bear, The 10th Man, Connecting the Dots, This Week in Geopolitics, Stray Reflections, and Conversations are published by Mauldin Economics, LLC. Information contained in such publications is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The information contained in such publications is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. The information in such publications may become outdated and there is no obligation to update any such information. You are advised to discuss with your financial advisers your investment options and whether any investment is suitable for your specific needs prior to making any investments.

John Mauldin, Mauldin Economics, LLC and other entities in which he has an interest, employees, officers, family, and associates may from time to time have positions in the securities or commodities covered in these publications or web site. Corporate policies are in effect that attempt to avoid potential conflicts of interest and resolve conflicts of interest that do arise in a timely fashion.

Mauldin Economics, LLC reserves the right to cancel any subscription at any time, and if it does so it will promptly refund to the subscriber the amount of the subscription payment previously received relating to the remaining subscription period. Cancellation of a subscription may result from any unauthorized use or reproduction or rebroadcast of any Mauldin Economics publication or website, any infringement or misappropriation of Mauldin Economics, LLC’s proprietary rights, or any other reason determined in the sole discretion of Mauldin Economics, LLC. Affiliate Notice Mauldin Economics has affiliate agreements in place that may include fee sharing. If you have a website or newsletter and would like to be considered for inclusion in the Mauldin Economics affiliate program, please go to http://affiliates.ggcpublishing.com/. Likewise, from time to time Mauldin Economics may engage in affiliate programs offered by other companies, though corporate policy firmly dictates that such agreements will have no influence on any product or service recommendations, nor alter the pricing that would otherwise be available in absence of such an agreement. As always, it is important that you do your own due diligence before transacting any business with any firm, for any product or service. © Copyright 2017 Mauldin Economics | -- |