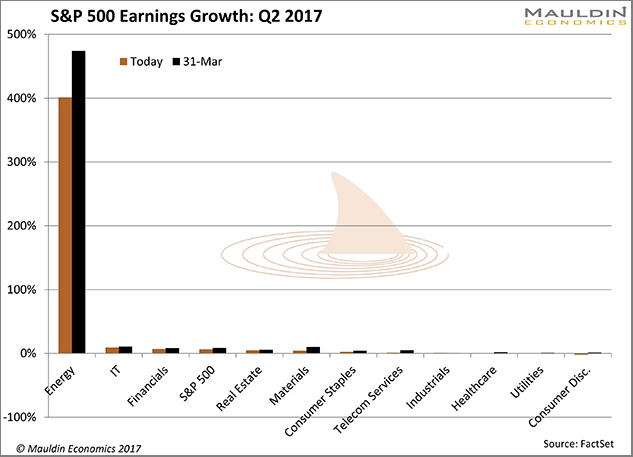

| -- | June 27, 2017 One Sector Is Propping Up the US Stock Market By Patrick Watson US stock benchmarks hit new all-time highs this month, and despite rich valuations, buyers think they’ll go higher still. One reason for this exuberance is the growing dominance of passively indexed ETFs. Rather than go to the trouble of picking individual stocks, people dump their cash into index ETFs. The ETF sponsor then buys every stock in the index—even the ugly ones. Profit growth seems to justify this, even in the broad indexes. In its June 16 bulletin, FactSet Research estimated that combined profits in the S&P 500 companies will rise 6.5% in this year’s second quarter. So, “combined profits” means some companies (and sectors) performed better than average, some worse, right? Actually, no. What we really have is one sector growing profits at a gangbuster rate. The others, not so much. Break down that 6.5% profit growth by sector, and you get this:  Here are the sectors that comprise the S&P 500’s 6.5% earnings growth this quarter, in ascending order. | Sector | 2Q Estimated Earnings Growth | | Consumer Discretionary | -2.0% | | Utilities | -0.5% | | Healthcare | 0.5% | | Industrials | 0.9% | | Telecom Services | 1.3% | | Consumer Staples | 2.5% | | Materials | 4.4% | | Real Estate | 5.1% | | S&P 500 Average | 6.5% | | Financials | 6.9% | | Technology | 9.4% | | Energy | 401.3% |

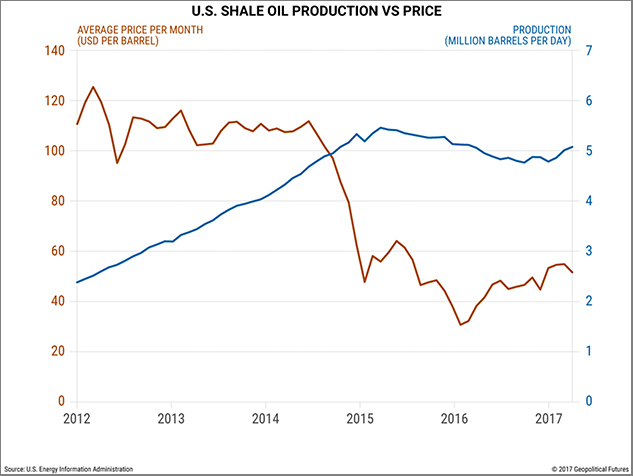

As you can see, the 6.5% average disguises considerable variation. Five of the 11 sectors have 1.3% earnings growth or less. Two are actually declining. Then there’s energy, where earnings growth is not just above above-average but 61 times more than average. Needless to say, earnings growth is way out of balance. The energy sector’s big recovery skews the average—remove it and the average drops from 6.5% to 3.6%, according to FactSet. In other words, almost half of this quarter’s S&P 500 earnings growth originates in a single sector that probably won’t keep growing at its present rate. Yet money still pours into index ETFs. Theory, Meet Reality Keep in mind, these are earnings estimates. We won’t know the real numbers until companies release their quarterly reports, starting next month. But there’s good reason to think they will be lower than many investors expect. The analysts behind these estimates presumed the average Q2 oil price to be $51.96 per barrel—a pretty optimistic estimate, to say the least. Oil traded below $50 the entire month of June and most of May as well. Oil and gas producers don’t always sell at the spot price. Some probably hedged at higher prices. Their industry has bigger problems, though. Economic theory tells us that “the cure” for excessively high or low commodity prices is more of the same. High prices encourage more production until, eventually, excess supply makes the price fall. Low prices cause production cuts that reduce supply and ultimately raise prices. Except that this theory no longer works for the US energy sector, as we see in this chart from Geopolitical Futures:  Oil prices plunged in late 2014, from over $100 to half that level. That should have led to lower production, but it didn’t—hence the present oil glut. Hen Apparently, the rules have changed. Technology is a big factor. New exploration and drilling technologies have made production costs fall sharply in the last three years. Many companies can produce oil and gas profitably even at today’s prices or lower. Some producers are so leveraged, they’ll have to keep pumping even if prices drop further. They need revenue to stay current on their debts. To be sure, any sudden supply disruption could push prices way up. A hurricane damaging Gulf Coast energy facilities or warfare in the Middle East would do it, at least temporarily. But the broader trends don’t look good if you need oil to stay over $50.

Image: GoFish While the S&P 500 earnings outlook looks impressive mainly due to a bounced-back energy sector, two other sectors—technology and financial services—look impressive as well. But they depend on energy too. If oil prices fall enough to hurt the energy sector, some producers will miss loan payments. That would be bad news for the lenders in the financial-services sector. Likewise, energy companies won’t buy as much hardware and software if they have to cut back on drilling activity. Not good for some technology companies. Bottom line: the bull market in US stocks will be on even shakier ground if oil prices dip below $40 again. In any case, earnings growth probably won’t continue at current rates unless oil prices climb higher. Opportunities will still exist—but throwing money into an index ETF isn’t be the way to find them. Millions of investors will learn that lesson the hard way. Don’t be one of them. See you at the top,  Patrick Watson P.S. If you’re reading this because someone shared it with you, click here to get your own free Connecting the Dots subscription. You can also follow me on Twitter: @PatrickW.  | Subscribe to Connecting the Dots—and Get a Glimpse of the Future

We live in an era of rapid change… and only those who see and understand the shifting market, economic, and political trends can make wise investment decisions. Macroeconomic forecaster Patrick Watson spots the trends and spells what they mean every week in the free e-letter, Connecting the Dots. Subscribe now for his seasoned insight into the surprising forces driving global markets. |

Senior Economic Analyst Patrick Watson is a master in connecting the dots and finding out where budding trends are leading. Patrick is the editor of Mauldin Economics’ high-yield income letter, Yield Shark, and co-editor of the premium alert service, Macro Growth & In come Alert. You can also follow him on Twitter (@PatrickW) to see his commentary on current events. Senior Economic Analyst Patrick Watson is a master in connecting the dots and finding out where budding trends are leading. Patrick is the editor of Mauldin Economics’ high-yield income letter, Yield Shark, and co-editor of the premium alert service, Macro Growth & In come Alert. You can also follow him on Twitter (@PatrickW) to see his commentary on current events.

Share Your Thoughts on This Article

Use of this content, the Mauldin Economics website, and related sites and applications is provided under the Mauldin Economics Terms & Conditions of Use. Unauthorized Disclosure Prohibited The information provided in this publication is private, privileged, and confidential information, licensed for your sole individual use as a subscriber. Mauldin Economics reserves all rights to the content of this publication and related materials. Forwarding, copying, disseminating, or distributing this report in whole or in part, including substantial quotation of any portion the publication or any release of specific investment recommendations, is strictly prohibited.

Participation in such activity is grounds for immediate termination of all subscriptions of registered subscribers deemed to be involved at Mauldin Economics’ sole discretion, may violate the copyright laws of the United States, and may subject the violator to legal prosecution. Mauldin Economics reserves the right to monitor the use of this publication without disclosure by any electronic means it deems necessary and may change those means without notice at any time. If you have received this publication and are not the intended subscriber, please contact service@mauldineconomics.com. Disclaimers The Mauldin Economics website, Yield Shark, Thoughts from the Frontline, Patrick Cox’s Tech Digest, Outside the Box, Over My Shoulder, World Money Analyst, Street Freak, Just One Trade, Transformational Technology Alert, Rational Bear, The 10th Man, Connecting the Dots, This Week in Geopolitics, Stray Reflections, and Conversations are published by Mauldin Economics, LLC. Information contained in such publications is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The information contained in such publications is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. The information in such publications may become outdated and there is no obligation to update any such information. You are advised to discuss with your financi al advisers your investment options and whether any investment is suitable for your specific needs prior to making any investments.

John Mauldin, Mauldin Economics, LLC and other entities in which he has an interest, employees, officers, family, and associates may from time to time have positions in the securities or commodities covered in these publications or web site. Corporate policies are in effect that attempt to avoid potential conflicts of interest and resolve conflicts of interest that do arise in a timely fashion.

Mauldin Economics, LLC reserves the right to cancel any subscription at any time, and if it does so it will promptly refund to the subscriber the amount of the subscription payment previously received relating to the remaining subscription period. Cancellation of a subscription may result from any unauthorized use or reproduction or rebroadcast of any Mauldin Economics publication or website, any infringement or misappropriation of Mauldin Economics, LLC’s proprietary rights, or any other reason determined in the sole discretion of Mauldin Economics, LLC. Affiliate Notice Mauldin Economics has affiliate agreements in place that may include fee sharing. If you have a website or newsletter and would like to be considered for inclusion in the Mauldin Economics affiliate program, please go to http://affiliates.ggcpublishing.com/. Likewise, from time to time Mauldin Economics may engage in affiliate programs offered by other companies, though corporate policy firmly dictates that such agreements will have no influence on any product or service recommendations, nor alter the pricing that would otherwise be available in absence of such an agreement. As always, it is important that you do your own due diligence before transacting any business with any firm, for any product or service. © Copyright 2017 Mauldin Economics | -- |