| -- | July 26, 2016

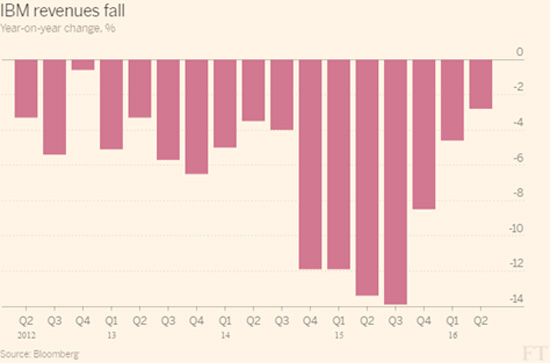

Putting Lipstick on a Pig, IBM Style Judging from the large amount of positive feedback on my June 21, 2016 column, An Anatomy of a Successful Short Sale, many of you find it as useful to spot failing companies as to uncover hidden gems. Instead of looking through the rearview mirror at a stock that has already been beaten down, I want to take a look at a stock that my Rational Bear subscribers are currently shorting, and the reasons why I expect it to fall. That stock is IBM. IBM reported its quarterly results last week, and the see-no-evil analysts on Wall Street jumped for joy at what I think were terrible results. Revenues Magic. What was so terrible? How about this—IBM has reported falling revenues for 17 consecutive quarters.  IBM pulled in sales of $20.2 billion last quarter, but that is 2.7% less than a year ago and 25% lower than in 2011.  The weakness is widespread: - Global Business Services had revenues of $4.3 billion, down 2%.

- Technology Services & Cloud Platforms (includes infrastructure services, technical support services, and integration software) had sales of $8.9 billion, down 0.5%.

- Systems (includes systems hardware and operating systems software) had sales of $2 billion, down 23.2%.

- Global Financing (includes financing and used equipment sales) had sales of $424 million, down 11.3%.

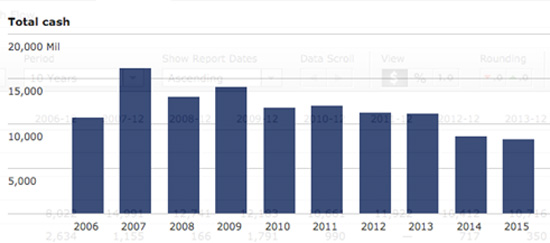

With all that red ink, the only way you can make yourself look good is by buying other companies. IBM has bought 11 companies worth $5 billion so far this year. In fact, it has spent more on acquisitions in the last 12 months than ever before in the history of the company. The $20.2 billion of Q2 revenues was boosted by around $400 million from those acquisitions, so the results would have been even uglier without them. Instead of 2.7%, the decline in revenues would have been a considerable 5%. Profit Magic. First of all, IBM reports its earnings on a pro forma basis instead of a GAAP basis. The main reason: it can use accounting magic to prop up its pro forma profits. On the profit side, IBM reported better-than-expected “pro forma” profits of $2.95, which was above the average forecast of $2.88. On a GAAP basis, those profits shrink to $2.61 a share.  Nonetheless, even using those phony pro forma calculations, the company’s profits are 25% lower than they were a year ago. Cash Magic. IBM is proud to point out that it increased its cash hoard from $7.6 billion in Q2 of 2015 to $10.6 billion today. However, that cash doesn’t come from operating profits but from borrowing money. A year ago, IBM had $33 billion of debt, but took on an additional $11.5 billion and now owes a staggering $44.5 billion.  That $10.6 billion cash isn’t going to last long, because IBM is burning through it. In Q2, the company had $3.4 billion of operating cash flow, but spent $5.9 billion on: - $1.0 billion on capital expenditures

- $2.8 billion on acquisitions

- $1.3 billion on dividends

- $800 million on share repurchases

That’s $2.5 million of negative operating cash flow. It’s only possible because of IBM’s debt binge and a big warning sign of a company in trouble. By the way, competitor Infosys warned that Brexit could hurt its business, but IBM is adopting the see-no-evil defense: “Brexit didn’t help, but from everything we’ve seen we haven’t changed our view,” said CFO Martin Schroeter. My view, on the other hand, is that IBM’s Brexit comeuppance may be near. Remember, at the top of this column, I said that my Rational Bear subscribers are already betting against IBM, so I am certainly guilty of “talking my book.” But no matter how its accountants spin things, IBM is a disaster in the making.

Tony Sagami

30-year market expert Tony Sagami leads the Yield Shark and Rational Bear advisories at Mauldin Economics. To learn more about Yield Shark and how it helps you maximize dividend income, click here. To learn more about Rational Bear and how you can use it to benefit from falling stocks and sectors, click here. Share this newsletter

http://www.mauldineconomics.com/members

Use of this content, the Mauldin Economics website, and related sites and applications is provided under the Mauldin Economics Terms & Conditions of Use. Unauthorized Disclosure Prohibited The information provided in this publication is private, privileged, and confidential information, licensed for your sole individual use as a subscriber. Mauldin Economics reserves all rights to the content of this publication and related materials. Forwarding, copying, disseminating, or distributing this report in whole or in part, including substantial quotation of any portion the publication or any release of specific investment recommendations, is strictly prohibited. Participation in such activity is grounds for immediate termination of all subscriptions of registered subscribers deemed to be involved at Mauldin Economics’ sole discretion, may violate the copyright laws of the United States, and may subject the violator to legal prosecution. Mauldin Economics reserves the right to monitor the use of this publication without disclosure by any electronic means it deems necessary and may change those means without notice at any time. If you have received this publication and are not the intended subscriber, please contact service@mauldineconomics.com. Disclaimers The Mauldin Economics web site, Yield Shark, Thoughts from the Frontline, Tony Sagami's Rational Bear, Stray Reflections, Outside the Box, Over My Shoulder, World Money Analyst, Street Freak, Just One Trade, Macro Growth & Income Alert, Transformational Technology Alert, and Conversations are published by Mauldin Economics, LLC. Information contained in such publications is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The information contained in such publications is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. The information in such publications may become outdated and there is no obligation to update any such information. John Mauldin, Mauldin Economics, LLC and other entities in which he has an interest, employees, officers, family, and associates may from time to time have positions in the securities or commodities covered in these publications or web site. Corporate policies are in effect that attempt to avoid potential conflicts of interest and resolve conflicts of interest that do arise in a timely fashion. Mauldin Economics, LLC reserves the right to cancel any subscription at any time, and if it does so it will promptly refund to the subscriber the amount of the subscription payment previously received relating to the remaining subscription period. Cancellation of a subscription may result from any unauthorized use or reproduction or rebroadcast of any Mauldin Economics publication or website, any infringement or misappropriation of Mauldin Economics, LLC’s proprietary rights, or any other reason determined in the sole discretion of Mauldin Economics, LLC. Affiliate Notice Mauldin Economics has affiliate agreements in place that may include fee sharing. If you have a website or newsletter and would like to be considered for inclusion in the Mauldin Economics affiliate program, please go to http://affiliates.pubrm.net/signup/me. Likewise, from time to time Mauldin Economics may engage in affiliate programs offered by other companies, though corporate policy firmly dictates that such agreements will have no influence on any product or service recommendations, nor alter the pricing that would otherwise be available in absence of such an agreement. As always, it is important that you do your own due diligence before transacting any business with any firm, for any product or service. © Copyright 2016 Mauldin Economics | -- |