| -- | November 21, 2017 Two Bad Choices in Tax Debate By Patrick Watson Remember when everyone wanted to cut the federal deficit? Fiscal policy was much simpler back then: balanced budget good, deficits bad.  Times change. Now the House and Senate are considering tax legislation that, according to their own numbers, will add $1.5 trillion to annual deficits over the next 10 years. This is okay, we’re told, because the tax cuts will stoke economic growth, thereby delivering added tax revenue that offsets the rate reductions. Note the bigger point here. Republicans still say they don’t like deficits—but apparently, this particular plan lets them cut taxes without adding more debt. It’s a miracle. Is their claim really true? Will the GOP tax plans boost economic growth? That’s the 1.5-trillion-dollar question.

Photo: Getty Images Theory vs. Reality Last week in “The Tax Trade Is Getting Crowded,” we considered the strange ways in which the current proposals “simplify” individual income taxes. Today, we’ll look at the corporate side. The Republican plan’s centerpiece is a reduction in corporate tax rates from a 35% top bracket to only 20%. That would put the US more in line with other countries. What you seldom hear is that most other developed countries also have value-added tax (VAT), a kind of consumption tax. The US doesn’t. Our tax system will remain different, and not necessarily better, under the new proposal. Anyway, the theory is that lower tax rates will entice businesses to bring back operations they currently conduct overseas. They will build new factories and hire more US workers. Those workers will spend their higher incomes on consumer goods, and we’ll all be better off. Unfortunately, that thinking has several flaws. For one, as we saw in the NFIB Small Business Economic Trends report that John Mauldin shared last week, business owners say that finding qualified workers is their top challenge right now. Reducing corporate tax rates won’t make new workers magically appear, nor will it improve the skills of those already here. What increasing labor demand might do is spark that inflation the Federal Reserve has wanted for years. There’s also a good chance it could spiral out of control, forcing the Fed to hike interest rates even faster than planned—which could offset any benefit from the tax cuts. Fortunately, such added labor demand will appear only if businesses respond to the lower tax rates by expanding US production capacity. Will they? Let’s ask.

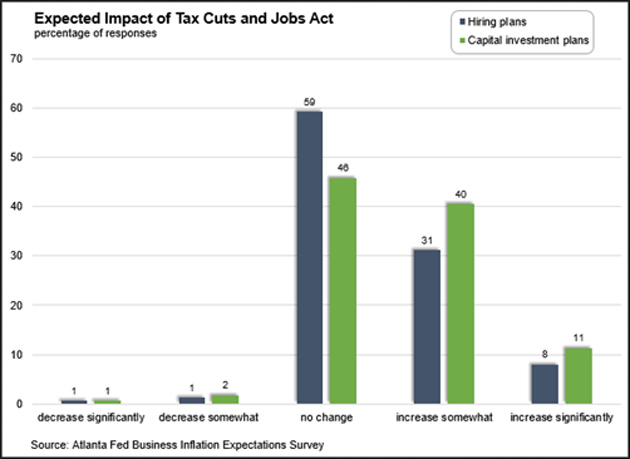

Photo: Getty Images “Why Aren’t the Other Hands Up?” This month, in one of its regular business surveys, the Atlanta Federal Reserve Bank asked executives, “If passed in its current form, what would be the likely impact of the Tax Cuts and Jobs Act on your capital investment and hiring plans?” Here are the results.

Image: Federal Reserve Bank of Atlanta Only 8% of the executives surveyed said the bill would make them increase hiring plans “significantly.” Only 11% said they would significantly increase their capital investment plans. A solid majority answered either “no change” or “increase somewhat.” Other surveys reached similar conclusions. White House Economic Advisor Gary Cohn had an awkward moment last Tuesday at a Wall Street Journal CEO Council meeting. Sitting on stage to promote the tax cuts, Cohn watched as the moderator asked the roomful of executives whether their companies would expand more if the tax bill passed. When only a few hands rose, Cohn looked surprised and said, “Why aren’t the other hands up?” So maybe they were distracted or needed a minute to think. Fair enough. A few hours later, White House Economist Kevin Hassett appeared at the same event and asked the same audience the same question. He got the same result: only a few raised hands.

Photo: Getty Images Pocketing Profits None of this should surprise us. Tax rates are only one factor businesses consider when deciding to expand. The far more important question is whether consumers will buy whatever the new capacity produces. Think about it this way: if you’re a CEO and you have difficulty selling your products profitably now, why would lower taxes make you produce more? Even a 0% tax rate is no help if you lack customers. Former Brightcove CEO David Mendels explained how big companies view this in a November 10 LinkedIn post. A tax cut for corporations will increase their profitability. Why we should believe that this increase in profitability will lead to wage increases when we have already seen that increases in profitability over the last 10 years did not, but rather went to stock buybacks and dividend increases that benefitted the investors? As a CEO and member of the Board of Directors at a public company, I can tell you that if we had an increase in profitability, we would have been delighted, but it would not lead in and of itself to more hiring or an increase in wages. Again, we would hire more people if we saw growing demand for our products and services. We would raise salaries if that is what it took to hire and retain great people. But if we had a tax cut that led to higher profits absent those factors, we would ‘pocket it’ for our investors.” By “pocket it,” Mendels means executive bonuses, share buybacks, or higher dividends. That’s what 10 years of Federal Reserve stimulus produced. A corporate tax cut would likely have a similar effect.

Photo: Getty Images Choose Wisely As I’ve said for months, I don’t think the House and Senate can agree on any significant tax changes. The two chambers have different political incentives they probably can’t reconcile. So I think we’ll be stuck with the current tax system. The economy will limp along like it has been and eventually go into recession. The hope-driven asset bubble will pop, hurting many investors. If I’m wrong and the GOP plan passes in anything like the current form, we will get higher deficits but little additional growth. The tax cuts will flow to asset owners and shareholders, probably blowing the market bubble even bigger. That will make the inevitable breakdown even more painful. Clearly, we need a better tax system. Other reform ideas exist. I think John Mauldin’s plan to sharply reduce or even eliminate the income tax, replacing it with a VAT-like consumption tax, would solve many problems. Trump advisors Stephen Moore and Larry Kudlow had another good idea last year: keep all the current deductions and credits but cap them at $150,000 per taxpayer. It would raise revenue and end many unproductive tax-avoidance schemes. Those ideas apparently aren’t attractive to Congress, though. So we’re stuck with either the current broken system or a modified one that will… - put the government even deeper in debt

- blow the market bubble bigger

- all without helping the economy grow.

Neither scenario is attractive, I know. But those are our choices. You can only pick one. Or rather, Congress will pick one for you. Let’s hope they choose wisely. See you at the top,  Patrick Watson P.S. If you’re reading this because someone shared it with you, click here to get your own free Connecting the Dots subscription. You can also follow me on Twitter: @PatrickW.  | Subscribe to Connecting the Dots—and Get a Glimpse of the Future

We live in an era of rapid change… and only those who see and understand the shifting market, economic, and political trends can make wise investment decisions. Macroeconomic forecaster Patrick Watson spots the trends and spells what they mean every week in the free e-letter, Connecting the Dots. Subscribe now for his seasoned insight into the surprising forces driving global markets. |

Senior Economic Analyst Patrick Watson is a master in connecting the dots and finding out where budding trends are leading. Patrick is the editor of Mauldin Economics’ high-yield income letter, Yield Shark, and co-editor of the premium alert service, Macro Growth & Income Alert. You can also follow him on Twitter (@PatrickW) to see his commentary on current events. Senior Economic Analyst Patrick Watson is a master in connecting the dots and finding out where budding trends are leading. Patrick is the editor of Mauldin Economics’ high-yield income letter, Yield Shark, and co-editor of the premium alert service, Macro Growth & Income Alert. You can also follow him on Twitter (@PatrickW) to see his commentary on current events.

Share Your Thoughts on This Article

Use of this content, the Mauldin Economics website, and related sites and applications is provided under the Mauldin Economics Terms & Conditions of Use. Unauthorized Disclosure Prohibited The information provided in this publication is private, privileged, and confidential information, licensed for your sole individual use as a subscriber. Mauldin Economics reserves all rights to the content of this publication and related materials. Forwarding, copying, disseminating, or distributing this report in whole or in part, including substantial quotation of any portion the publication or any release of specific investment recommendations, is strictly prohibited.

Participation in such activity is grounds for immediate termination of all subscriptions of registered subscribers deemed to be involved at Mauldin Economics’ sole discretion, may violate the copyright laws of the United States, and may subject the violator to legal prosecution. Mauldin Economics reserves the right to monitor the use of this publication without disclosure by any electronic means it deems necessary and may change those means without notice at any time. If you have received this publication and are not the intended subscriber, please contact service@mauldineconomics.com. Disclaimers The Mauldin Economics website, Yield Shark, Thoughts from the Frontline, Patrick Cox’s Tech Digest, Outside the Box, Over My Shoulder, World Money Analyst, Street Freak, Just One Trade, Transformational Technology Alert, Rational Bear, The 10th Man, Connecting the Dots, This Week in Geopolitics, Stray Reflections, and Conversations are published by Mauldin Economics, LLC. Information contained in such publications is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The information contained in such publications is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. The information in such publications may become outdated and there is no obligation to update any such information. You are advised to discuss with your financial advisers your investment options and whether any investment is suitable for your specific needs prior to making any investments.

John Mauldin, Mauldin Economics, LLC and other entities in which he has an interest, employees, officers, family, and associates may from time to time have positions in the securities or commodities covered in these publications or web site. Corporate policies are in effect that attempt to avoid potential conflicts of interest and resolve conflicts of interest that do arise in a timely fashion.

Mauldin Economics, LLC reserves the right to cancel any subscription at any time, and if it does so it will promptly refund to the subscriber the amount of the subscription payment previously received relating to the remaining subscription period. Cancellation of a subscription may result from any unauthorized use or reproduction or rebroadcast of any Mauldin Economics publication or website, any infringement or misappropriation of Mauldin Economics, LLC’s proprietary rights, or any other reason determined in the sole discretion of Mauldin Economics, LLC. Affiliate Notice Mauldin Economics has affiliate agreements in place that may include fee sharing. If you have a website or newsletter and would like to be considered for inclusion in the Mauldin Economics affiliate program, please go to http://affiliates.ggcpublishing.com/. Likewise, from time to time Mauldin Economics may engage in affiliate programs offered by other companies, though corporate policy firmly dictates that such agreements will have no influence on any product or service recommendations, nor alter the pricing that would otherwise be available in absence of such an agreement. As always, it is important that you do your own due diligence before transacting any business with any firm, for any product or service. © Copyright 2017 Mauldin Economics | -- |