| -- | January 9, 2018 Wages Are the Key to 2018 By Patrick Watson Nine days into 2018, I’ve read 793 economic and market forecasts. Okay, that’s an exaggeration… but it certainly feels like it. In any case, I’ve read enough to know opinions are all over the place. Whatever your desired scenario, some expert says it’s a sure thing. | A Society Quite Unlike Any Other Join the Alpha Society and enjoy an unprecedented level of access to John Mauldin and the Mauldin editors. Find out more |

| | - |

A forecaster’s greatest challenge is separating what you want to happen from what you think will happen. There’s nothing wrong with wishing events will turn out favorably. But that desire shouldn’t keep you from accepting the facts and their likely consequences. I think John Mauldin got the right balance in his 2018 forecast, Economy on a Roll. After helping John with research for that letter, I mostly agree with his conclusions. I say “mostly” because I am not quite as optimistic for 2018. John and I both think this year’s top risk is a miscalculation by the Federal Reserve—specifically, that it will tighten monetary policy too much. As I’ve thought about it and read other forecasts, I have a slightly different view. Here’s the key question: if the average worker’s paycheck grows, is it good or bad for the economy? The answer is less clear than you might think.

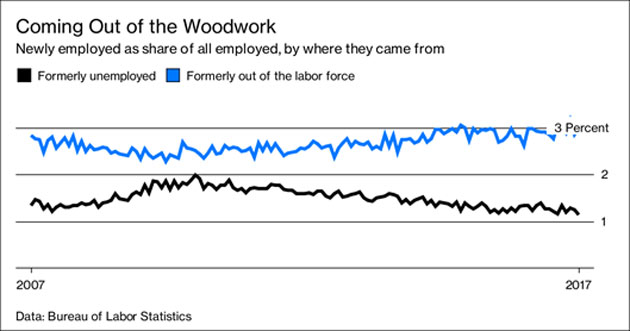

Photo: Getty Images Full Employment? Before we go on, a small mea culpa. I didn’t think the Republicans would manage to pass a tax cut in 2017. They did, albeit after taking almost the whole year. The bill they passed also has more short-term stimulus than I thought possible. Several provisions give businesses an incentive to expand capacity. It’s not much and won’t begin to cover the added debt the tax cuts produce, but it will help. However, the more salient issues are jobs and wages. The Fed is hiking interest rates because its experts believe the economy is close to “full employment,” and the Phillips Curve says wages should start rising any minute now. Economists have been scratching their heads trying to understand why wages aren’t already shooting higher. If qualified workers are so hard to find, why don’t employers offer higher pay to attract more? One possibility: the untapped labor supply is more than the 4.1% jobless rate suggests. Here’s an interesting stat you may not have seen. Most newly employed people weren’t on the books as “unemployed” right before starting their jobs. They went straight from “out of the labor force” to “employed,” because they were in school or military service, or otherwise neither employed nor seeking a job.

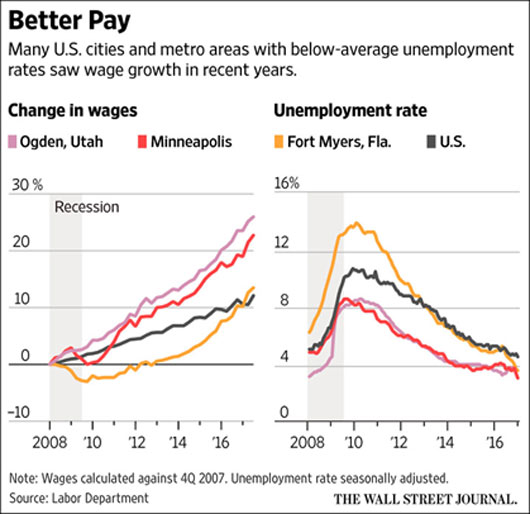

Chart: Bloomberg That means if you’re an employer, the available-worker pool from which you can draw is much bigger than the 4.1% of the labor force that is nominally “unemployed.” This suggests wage pressure might be farther off than we think. Another measuring challenge is that we look at average hourly earnings. Total pay can go up even when hourly wages don’t, if workers get more on-the-clock hours… which they have, slightly. Average weekly earnings rose 2.8% in 2017 while average hourly earnings rose only 2.5%. Even a 2.8% wage gain wasn’t much, though, once you subtract last year’s 2.2% Consumer Price Index (CPI) inflation. Not to mention that it’s hardly an economic boom when the only way to noticeably increase your income is to work more hours. Regional Wage Differences Just as in the employment rate, wages have a lot of regional variation. They’re rising faster in cities that have below-average unemployment. You can see it in this chart, which shows that since 2008, wages rose much more in the Minneapolis and Ogden, Utah metro areas.

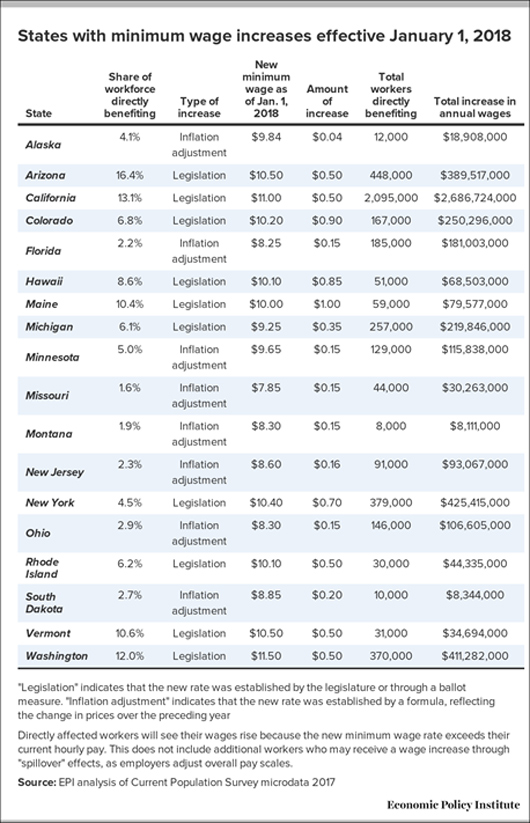

Chart: Wall Street Journal Better yet, wages are catching up in Fort Myers, Florida, where they had lagged badly for years. We need the trends to spread elsewhere, but these are encouraging signs. Another small but positive sign was the move by some large corporations to give employee bonuses after President Trump signed the tax cuts. Was it partly a publicity stunt? Yes, but the money was real. Now we need to see those same companies and others raise regular wages and increase their headcount. Minimum Wage Rising A third change is that 18 states raised their minimum wages as of this month. The Economic Policy Institute estimates the increases will mean $5 billion in additional wages to about 4.5 million workers. Here’s their full list.

Source: Economic Policy Institute Is that enough to affect the national inflation rates the Fed is watching? Maybe not. Further, paying those higher wages may force employers to cut other expenses, leaving the overall inflation rate unaffected. However, there may also be a spillover effect. Higher entry-level wages can force employers to raise pay further up the ladder too, in order to keep “relative” earnings the same. The numbers above don’t include this. Watch Wages Through the Fed’s Eyes For forecasting purposes, whatever you or I think about the wage situation is less important than what Federal Reserve officials think. The December FOMC minutes are our most recent look inside their heads. A few participants judged that the tightness in labor markets was likely to translate into an acceleration in wages; however, another observed that the absence of broad-based upward wage pressures suggested that there might be scope for further improvement in labor market conditions. Reading the tea leaves here, “a few” who thought wages will rise should outweigh the “another” who saw an absence of wage pressures. But is that a majority? We don’t know. Plus, the Fed will be getting new faces this year with possibly different ideas. As of last month, the dot plots showed three rate hikes coming this year. Futures markets imply it will be less than that, maybe only two. If that’s the plan when wage growth is at best uncertain, then it won’t take much for the Fed to hike rates higher and faster than currently expected. That, in turn, could quickly change the Goldilocks scenarios that project everything will go just right this year, letting stock prices move up steadily.

Photo: Getty Images On the other hand, higher wages will put more money in workers’ pockets and give them more spending power. That will be good for the economy, even if it’s negative for stocks. Pay Attention All this suggests paying attention to wage data will be important this year. It’s really the key to everything. - Stronger-than-expected wage growth will make the Fed see inflation, tighten policy more than presently expected, and probably send stock prices lower.

- Conversely, continued flat wages will let the Fed stay on its present slow-hiking course. That would be bullish for stocks.

I’d like to see the first scenario, because I think it will be the best long-term outcome for everyone. However, I think the second scenario is closer to what we’ll get. Other factors are also in the mix. Energy prices have spiked, for instance. That could boost inflation prospects if it persists. Like the Fed, I’m data-dependent. I’ve told my Yield Shark readers I’ll watch the numbers and adjust accordingly. You should do the same. See you at the top,  Patrick Watson P.S. If you’re reading this because someone shared it with you, click here to get your own free Connecting the Dots subscription. You can also follow me on Twitter: @PatrickW.  | Subscribe to Connecting the Dots—and Get a Glimpse of the Future

We live in an era of rapid change… and only those who see and understand the shifting market, economic, and political trends can make wise investment decisions. Macroeconomic forecaster Patrick Watson spots the trends and spells what they mean every week in the free e-letter, Connecting the Dots. Subscribe now for his seasoned insight into the surprising forces driving global markets. |

Senior Economic Analyst Patrick Watson is a master in connecting the dots and finding out where budding trends are leading. Patrick is the editor of Mauldin Economics’ high-yield income letter, Yield Shark, and co-editor of the premium alert service, Macro Growth & Income Alert. You can also follow him on Twitter (@PatrickW) to see his commentary on current events. Senior Economic Analyst Patrick Watson is a master in connecting the dots and finding out where budding trends are leading. Patrick is the editor of Mauldin Economics’ high-yield income letter, Yield Shark, and co-editor of the premium alert service, Macro Growth & Income Alert. You can also follow him on Twitter (@PatrickW) to see his commentary on current events.

Share Your Thoughts on This Article

Use of this content, the Mauldin Economics website, and related sites and applications is provided under the Mauldin Economics Terms & Conditions of Use. Unauthorized Disclosure Prohibited The information provided in this publication is private, privileged, and confidential information, licensed for your sole individual use as a subscriber. Mauldin Economics reserves all rights to the content of this publication and related materials. Forwarding, copying, disseminating, or distributing this report in whole or in part, including substantial quotation of any portion the publication or any release of specific investment recommendations, is strictly prohibited.

Participation in such activity is grounds for immediate termination of all subscriptions of registered subscribers deemed to be involved at Mauldin Economics’ sole discretion, may violate the copyright laws of the United States, and may subject the violator to legal prosecution. Mauldin Economics reserves the right to monitor the use of this publication without disclosure by any electronic means it deems necessary and may change those means without notice at any time. If you have received this publication and are not the intended subscriber, please contact service@mauldineconomics.com. Disclaimers The Mauldin Economics website, Yield Shark, Thoughts from the Frontline, Patrick Cox’s Tech Digest, Outside the Box, Over My Shoulder, World Money Analyst, Street Freak, Just One Trade, Transformational Technology Alert, Rational Bear, The 10th Man, Connecting the Dots, This Week in Geopolitics, Stray Reflections, and Conversations are published by Mauldin Economics, LLC. Information contained in such publications is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The information contained in such publications is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. The information in such publications may become outdated and there is no obligation to update any such information. You are advised to discuss with your financial advisers your investment options and whether any investment is suitable for your specific needs prior to making any investments.

John Mauldin, Mauldin Economics, LLC and other entities in which he has an interest, employees, officers, family, and associates may from time to time have positions in the securities or commodities covered in these publications or web site. Corporate policies are in effect that attempt to avoid potential conflicts of interest and resolve conflicts of interest that do arise in a timely fashion.

Mauldin Economics, LLC reserves the right to cancel any subscription at any time, and if it does so it will promptly refund to the subscriber the amount of the subscription payment previously received relating to the remaining subscription period. Cancellation of a subscription may result from any unauthorized use or reproduction or rebroadcast of any Mauldin Economics publication or website, any infringement or misappropriation of Mauldin Economics, LLC’s proprietary rights, or any other reason determined in the sole discretion of Mauldin Economics, LLC. Affiliate Notice Mauldin Economics has affiliate agreements in place that may include fee sharing. If you have a website or newsletter and would like to be considered for inclusion in the Mauldin Economics affiliate program, please go to http://affiliates.ggcpublishing.com/. Likewise, from time to time Mauldin Economics may engage in affiliate programs offered by other companies, though corporate policy firmly dictates that such agreements will have no influence on any product or service recommendations, nor alter the pricing that would otherwise be available in absence of such an agreement. As always, it is important that you do your own due diligence before transacting any business with any firm, for any product or service. © Copyright 2018 Mauldin Economics | -- |