Consumption and prices up strongly in October

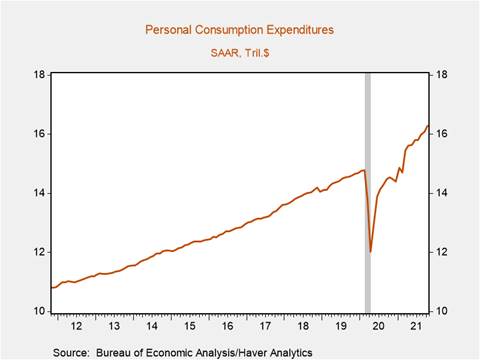

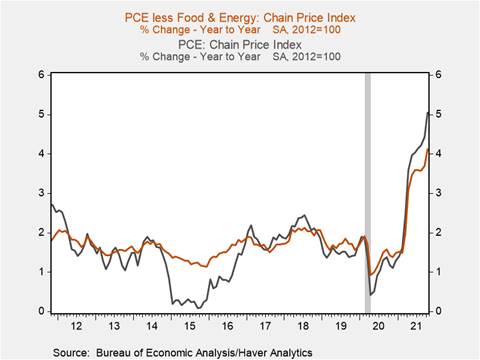

*U.S. consumption increased 1.3% m/m, lifting its yr/yr increase to 12% supported by rising employment, wages, and disposable incomes (Chart 1). Strong demand amid supply bottlenecks and disruptions have led to soaring prices: the headline and core PCE price indexes rose substantially in October, increasing 0.6% and 0.4% m/m, respectively, lifting their yr/yr increase to 5.1% and 4.1% (a thirty-year high) (Chart 2). Continued growth in employment and wages will support consumption heading into what will likely be a strong holiday retail season, contributing to a rebound in GDP growth in Q4.

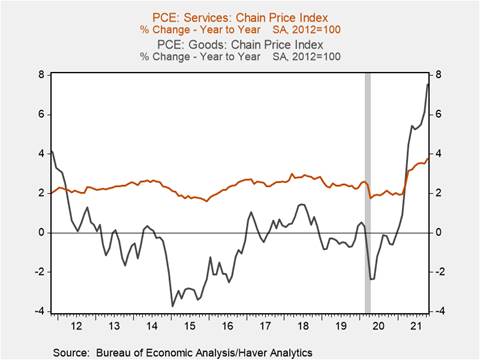

*October’s increase in consumption was underscored by a surge in durable goods consumption, which rose 3.3% m/m reflecting the intra-pandemic tilt of consumption towards goods – in comparison services consumption rose 0.9%, partly reflecting the negative impact of the delta variant on in-person service sector activity (Chart 3). In real terms consumption rose 0.7% m/m, lifting real consumption $570 billion above its pre-pandemic peak on an annualized basis. Consumption of motor vehicles and parts rose 5% m/m, and further increases are likely as auto production expands in response to easing supply disruptions.

*Zooming headline PCE inflation has been driven by marked increases in goods prices, particularly among durable goods, reflecting supply-demand imbalances that are unlikely to be resolved until well into 2022. Goods prices rose 1.2% m/m, with both durable and nondurable goods prices rising 1.2% m/m, lifting their yr/yr increases to 8.8% and 6.8%, respectively. In contrast, services prices rose 0.3% m/m and 3.7% yr/yr (Chart 3). Of note, imputed rent of owner-occupied housing and rental prices have begun to accelerate with both rising 0.4% m/m. Zooming home prices over the course of the pandemic are beginning to feed in to measures of shelter costs in the PCE, and will likely contribute substantially to headline and core PCE inflation through 2022.

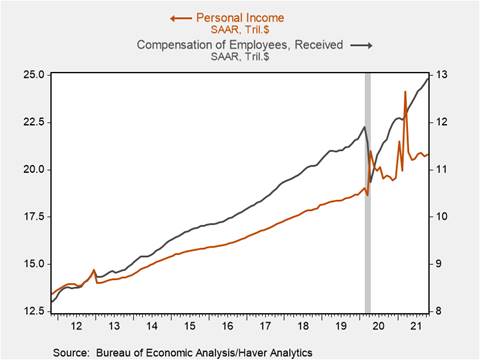

*Personal income rose 0.4% in October reflecting employment gains and rising nominal wages. Private sector wages and salaries rose 1% m/m, highlighting a mix of employment growth and rising average hourly earnings due to high labor demand (Chart 4). Increased employee compensation was not enough to fully offset September’s $250+ billion annualized decline in government transfer receipts following the expiration of pandemic unemployment insurance, consequently personal income remains $110 billion annualized below its level two months ago. Despite the temporary blip, personal income growth should continue as the labor market recovers and employee compensation rises to ‘catch up’ to inflation. The personal saving rate fell to 7.3%, its lowest level since 2019, as surging consumption has outpaced the more moderate gains in disposable income. Going forward, households may begin to draw more aggressively on excess savings accumulated during the pandemic and credit to support spending.

*Rising disposable income and employment will contribute to strong consumption growth in Q4, and as the Fed notes, prices will likely continue to accelerate through H1 2022. November’s CPI print may prompt the Fed to announce an acceleration of the pace of asset purchases at its December or January meeting.

Chart 1: Personal Consumption Expenditures

Chart 2: PCE Price Index vs. Core PCE Price Index (yr/yr, %)

Chart 3: PCE Price Index – Goods vs. Services (yr/yr, %)

Chart 4: Personal Income vs. Compensation of Employees (SAAR, $ trillions)

Mickey Levy, mickey.levy@berenberg-us.com

Mahmoud Abu Ghzalah, mahmoud.abughzalah@berenberg-us.com

© 2021 Berenberg Capital Markets, LLC, Member FINRA and SPIC

Remarks regarding foreign investors. The preparation of this document is subject to regulation by US law. The distribution of this document in other jurisdictions may be restricted by law, and persons, into whose possession this document comes, should inform themselves about, and observe, any such restrictions. United Kingdom This document is meant exclusively for institutional investors and market professionals, but not for private customers. It is not for distribution to or the use of private investors or private customers. Copyright BCM is a wholly owned subsidiary of Joh. Berenberg, Gossler & Co. KG (“Berenberg Bank”). BCM reserves all the rights in this document. No part of the document or its content may be rewritten, copied, photocopied or duplicated in any form by any means or redistributed without the BCM’s prior written consent. Berenberg Bank may distribute this commentary on a third party basis to its customers.