CPI Inflation in August simmers down at a high level

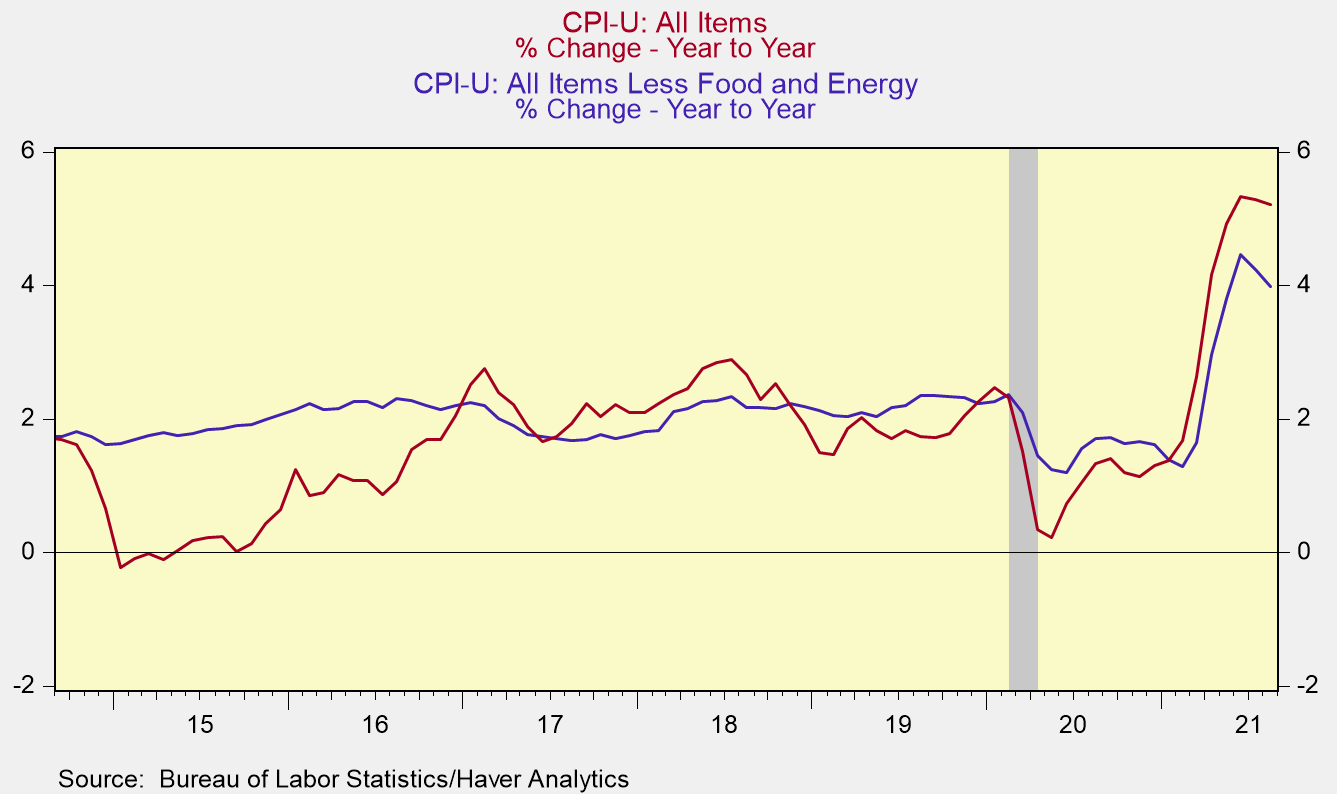

*CPI inflation increased 0.3% mo/mo in August, lowering its yr/yr rise to 5.2%, down from July’s increase of 5.3%, while the core CPI, excluding food and energy, increased 0.1%, lowering its yr/yr rise to 4.0% from July’s increase of 4.2% (Chart 1). The August data suggests a temporary flattening of inflation at a high level. In the coming months, we expect inflation to remain elevated as the earlier sharp increases in prices of some goods ease (automobiles) while other prices (shelter) accelerate, while businesses continue to raise product prices to offset sharp increases in production costs.

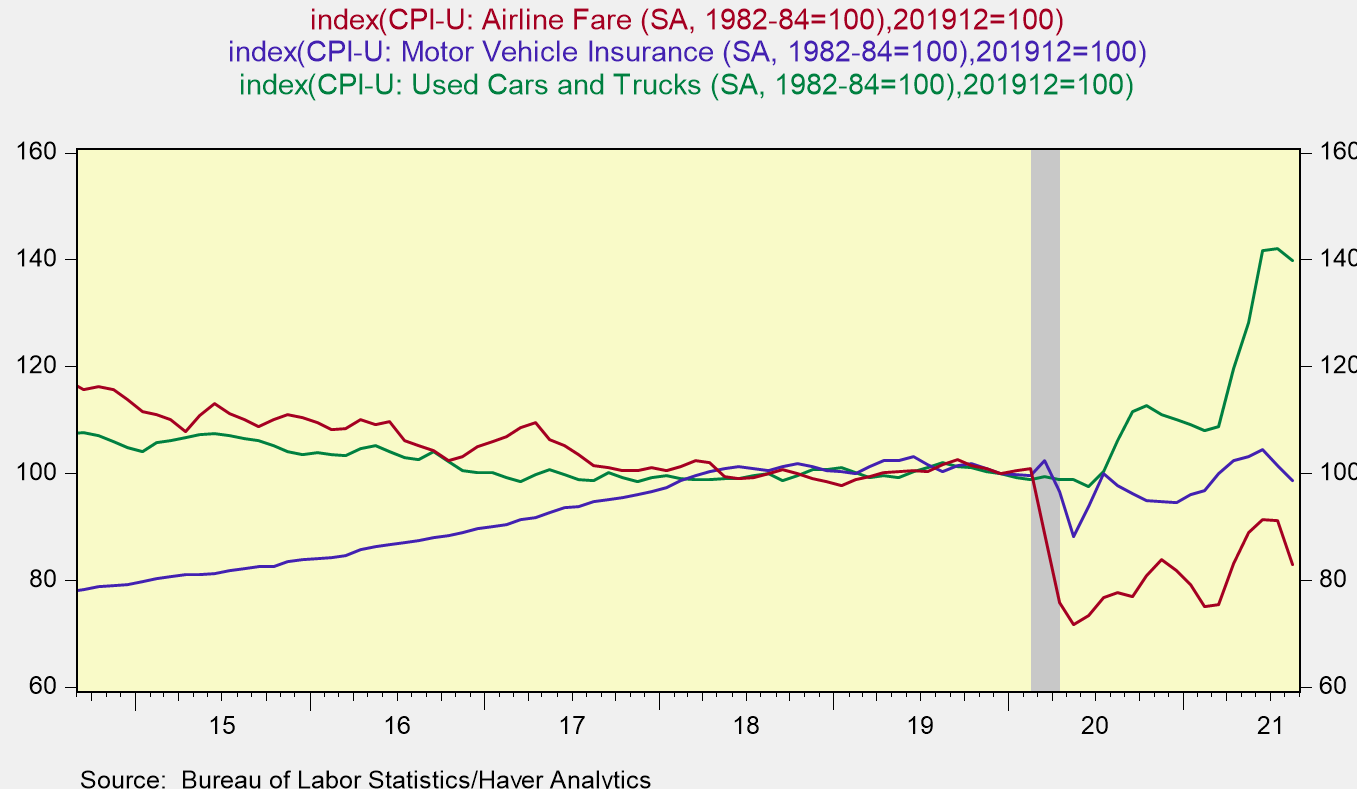

*The components of the CPI that contributed to the easing of the monthly inflation rate include: used cars and trucks (-1.5%) motor vehicles, transportation services (-2.3%), including large monthly declines in motor vehicle insurance (-2.8%) and airline fares (-9.1%). All of these components had experienced large double-digit yr/yr increases through June. We note that the CPI index for used cars and trucks is 40% above its pre-pandemic level, the index for motor vehicle insurance is about the same while airline fares are 17% lower (Chart 2).

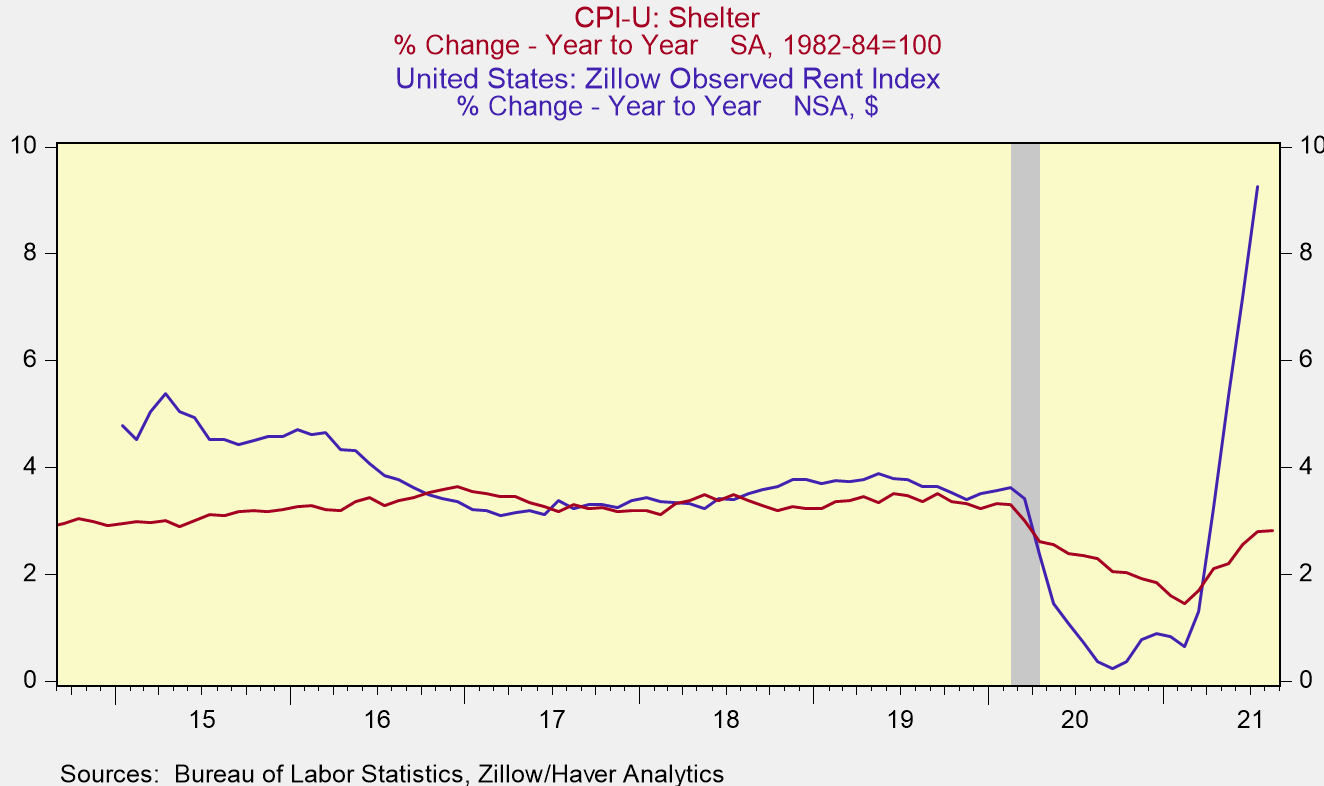

*Shelter, the largest component in the CPI, increased a scant 0.2% in August, while its subcomponent owners’ equivalent rent of residencies (OER) increased 0.25%, barely lifting its yr/yr increases to 2.8% and 2.5%, respectively. These increases represent small fractions of the yr/yr increases in home prices (+18.6% according to S&P CoreLogic Case-Shiller) or rental costs (+9.25% according to Zillow Observed Rental Index, Chart 3). While the shelter component of the CPI traditionally lags home prices, this current shortfall from surveys of rental costs is striking. In the coming months, measured increases in the shelter component are expected to rise.

*Inflation is already far above the Fed’s earlier forecasts of inflation and its longer-run 2% target. As inflation has surprised the Fed on the upside, the Fed has altered its definition of “temporary” versus more persistent inflation. The Fed acknowledges that the above-2% inflation in the last year has met its required make-up strategy. Today’s inflation report for August provides some relief to the Fed. But, it is only one piece of monthly data and the inflation story is not over. The future trajectory of inflation depends on the pace of aggregate demand in the economy, how long supply constraints persist, and how higher inflationary expectations influence price and wage setting behavior. We anticipate inflation will remain elevated.

Chart 1

Chart 2.

Mickey Levy, mickey.levy@berenberg-us.com