Click here for full report and disclosures

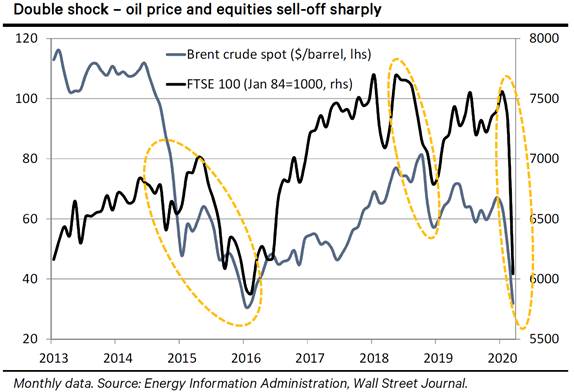

â Oil price war: Saudi Arabiaâs decision to dramatically step up its production of oil and flood the market has triggered the biggest one-day drop in the price of oil since the Gulf War in 1991. Down from $41.3 per barrel of Brent crude oil last Friday, the current price of c$32 per barrel is the lowest since January 2016 – see chart. Against a backdrop of rising global risks linked to COVID-19, a sustained shock to the oil sector can have far-reaching consequences.

â Crude politics: By raising output and offering big price discounts, Saudi Arabia wants to penalise Russia for refusing to cut production in order to stabilise the oil price as COVID-19 disruptions harm global demand. That oil-dependent Russia will strike a deal with the Saudis soon is not a given, though. Russia and other oil producers have lost market share to US shale in recent years. The US is now the top swing producer in global oil markets. Russia may thus choose to tolerate the pain of an unprofitable price for a while in the hope that it can regain some market share.

â Debt vulnerabilities: The immediate concern for markets is that the oil price plunge will squeeze the balance sheets of some heavily indebted US energy companies. Energy companies account for more than 10% of the US high-yield market – so-called junk bonds. The spread on such bonds versus treasuries is currently c10.8ppt – up from c6.4ppt at the start of the year. While that spread is the highest since April 2016, it remains well below the peak of c17.8ppt in February 2016. The sharp sell-off in global equities today reflects the fear of contagion from potential defaults in the US energy sector to other vulnerable pockets of the corporate debt market. As a result, purchases of corporate bonds should be among the instruments central banks ought to consider.

â The lesson of 2015/16: A dramatic decline in oil prices in H2 2015 linked to a Chinese slowdown and rising oil supply from US shale triggered turbulence in financial markets that focused on the concentrated costs to oil producers and some small oil-exporting countries. However, markets rebounded once the widespread benefits to the 75% of the global economy that net imports oil became obvious. A similar logic may eventually apply this time around. However, a sustained period of lower oil prices should be welcomed as the world contends with the global demand- and supply-side shock linked to the spread of COVID-19.

â Economic consequences: A sustained drop in the price of oil by, say, $10 per barrel would reduce headline inflation across Europe by c0.3ppt over the near term. While this would support real income growth, it may not lift spending by much yet. For now, worries about the negative economic consequences of COVID-19 will overwhelm any positives from cheaper oil. Nervous households and firms are more likely to add to precautionary savings than spend the windfall. However, once economies have weathered the worst of the virus-related disruptions and activity normalises, some of the surplus savings will be spent. This should reinforce the eventual recovery – likely in H2 2020.

â Challenges ahead: Before we can seriously consider the shape of any recovery, the global economy must get through the rough patch ahead. The equities bear market and the rush to safe assets like gold and government bonds reflect fears about the outlook. As long as the number of active cases of COVID-19 outside China continues to rise, the risk of more bad news – think Lombardy – in major parts of the world economy looms large.

Senior Economist

+44 20 3465 2672

kallum.pickering@berenberg.com

![]()

Disclosures

This material is intended as commentary on political, economic or market conditions for institutional investors or market professionals only and does not constitute a financial analysis or a research report as defined by applicable regulation. See the "Disclaimers" section of this report.

The commentary included herein was produced by Joh. Berenberg, Gossler & Co. KG (Berenberg). For sales inquiries, please contact:

Phone: +44 (0)20 3207 7800

Email: berenberg.economics@berenberg.com

BERENBERG

Joh. Berenberg, Gossler & Co. KG

Neuer Jungfernstieg 20

20354 Hamburg

Germany

Registered Office: Hamburg, Germany

Local Court Hamburg HRA 42659