| Four Keys to Sidestepping This Huge Retirement Risk | | By Alexander Green, Chief Investment Strategist, The Oxford Club | | Wednesday, March 30, 2016 |

| Over the last century, the average bear market has lasted almost exactly one year, according to Ned Davis Research. The average recovery to a new all-time high took the market an additional 2.1 years.

So long-term investors who plan to put fresh money to work should not wish for the market to keep going up – because that would only mean investing in equities at ever-higher prices – but rather pray that it starts going down, so that they can invest at lower prices.

Bear markets are an enormous opportunity for the accumulation of retirement assets. (Although far too few folks see it that way.) Yet for another group of investors, they pose a serious risk.

I'm referring to those just entering retirement. They face what is often called sequence-of-returns risk. And it can be a serious challenge.

Here's what I mean...

----------Recommended Links---------

---------------------------------

One of the toughest potential developments for any individual with equities is retiring right into the teeth of a bear market. If you are forced to make withdrawals early in retirement from a portfolio that is rapidly declining in value, there will be fewer shares left to benefit when the market eventually rebounds.

And while an average of 3.1 years (one year of decline followed by 2.1 years of recovery) from one bull market top to the next may not sound that long, history shows it could take years longer.

The bear market that began in 1973, for example, took almost 12 years to reach a new high. So prepare in advance for sequence-of-returns risk with four key steps.

| 1. | As you get ready to retire, put one to three years of income in cash. But don't start spending it immediately. If we're in a bull market, you can cull annual gains to cover your overhead. But when we go into a bear market – as we will eventually – use this cash account for spending needs so you won't have to invade your long-term assets when they are at a low ebb. | | | | | 2. | Of course, with the worst of luck, stocks could start declining as soon as you retire and still be falling or near the bottom three years later. In that case, you would be better off cashing in bonds and other low-risk assets rather than selling your stocks. Again, the reason is obvious. You can't recover from a bear market in equities if you sell your stocks when they are near the bottom. | | | | | 3. | Set up a home-equity line of credit. It may seem foolish to borrow and pay interest to meet your expenses in retirement, but you can always pay off that home-equity loan in the future by cashing in some of your stocks after they've recovered. | | | | | 4. | As a final sequence-of-returns strategy, consider a reverse mortgage. If you own your home and are 62 or older, you can pull equity out of your house and pay the bank nothing until you move, sell, or die. However, reverse mortgages also have drawbacks and can be complicated. So I recommend this only as a last resort. |

There are other non-investment-related moves you can also make to maximize the life of your portfolio in retirement. These include cutting costs, downsizing, or plunking for a low-cost immediate fixed annuity like the kind Vanguard brokers. (This is the only type of annuity worth considering, in my view. The rest benefit the annuity salesman far more than the purchaser.)

In short, your primary investment goal in retirement is to make sure your portfolio doesn't kick the bucket before you do. A bear market that begins right after you leave the workforce can be a substantial challenge. But follow the four steps outlined above, and you can easily sidestep potential sequence-of-returns risk.

Good investing,

Alexander Green

Editor's note: Bear market or not, Congress has just approved a program that will put more than $42 billion back in the pockets of Americans. To learn about this "Consumer Rebate Program" – which will let you collect a cash rebate on nearly every single purchase you made in 2015, even if you don't have receipts – click here. But act quickly... this offer disappears next month. |

Further Reading:

Earlier this year, Alexander explained why you can't act on emotions and expect to prosper in the stock market. "Panicking is for when a toddler in your charge suddenly darts into the street," he says. "It has no place in portfolio management." Learn what he says the key to long-term investment success is right here. Expert wealth-builder Mark Ford believes the conventional dream of retirement is not very satisfying as a reality. That's why he says you should "never retire." Learn more about Mark's strategy in this interview. |

|

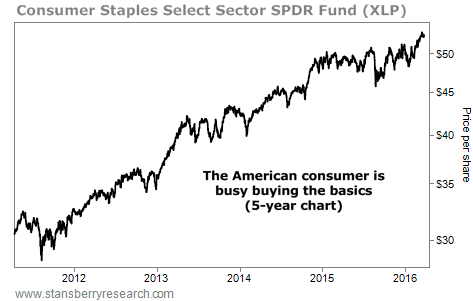

AN UPDATE ON THE AMERICAN CONSUMER

Today's chart tells us that once again, the American consumer is alive and well... and he's out buying the everyday "basics"... With gas prices so low at the pump, Americans have more money in their pockets... and they're loading up on consumer staples. These include things like beer, cigarettes, and soda. We've covered the importance of these types of products many times before. In short, these items are never in danger of going obsolete. We can see this trend by looking at the Consumer Staples Select Sector SPDR Fund (XLP). This fund holds many world-class companies we've featured before, including consumer-goods company Procter & Gamble, soft-drink giant Coca-Cola, retailers Wal-Mart and Costco, cigarette maker Philip Morris, and drugstore CVS Health. The performance of XLP can tell us a lot about the state of the economy... If people are spending money on these types of "boring" goods, things can't be all that bad. As you can see below, XLP is locked into a long-term uptrend. Shares are up nearly 80% over the past five years. And the stock continues to tick higher today... |

|

| Collect a 7.9% income stream, starting now... Most investors nearing retirement dread the thought of a bear market. But your total stock investments should be lower as you approach retirement anyway. |

Are You a

New Subscriber?

If you have recently subscribed to a Stansberry Research publication and are unsure about why you are receiving the DailyWealth (or any of our other free e-letters), click here for a full explanation... |

|

Advertisement

You may need to act by Friday, April 29, to avoid missing out on thousands in extra benefits from Social Security. Luckily, there's an easy solution. Check out the summary of our findings, here. |

| You Haven't Missed the Boom in Florida Real Estate | | By Dr. Steve Sjuggerud | | Tuesday, March 29, 2016 |

| | The prices have gone up, a lot. But you haven't missed the boom yet. The values are still here... |

| | The Three Principles of Consistent Wealth-Building | | By Dr. David Eifrig | | Monday, March 28, 2016 |

| | Building wealth is all about being patient and staying committed. If you want to grow your wealth meaningfully over time, there are three principles you must understand... |

| | Triple-Digit-Upside Potential in a Sector You Haven't Considered... | | By Dr. Steve Sjuggerud | | Thursday, March 24, 2016 |

| | A certain commodity jumped 7% from February 26 to March 4, its largest weekly return since 2011. And based on history, the jump will likely lead to even higher prices... |

| | Grow Your Wealth for Decades Without a Single Losing Year | | By Mark Ford | | Wednesday, March 23, 2016 |

| I have learned several lessons about growing wealth and avoiding the biggest mistakes average investors make... |

| | 53% Upside in Hong Kong Stocks | | By Dr. Steve Sjuggerud | | Tuesday, March 22, 2016 |

| | Hong Kong residential sales just hit a 25-year low... Based on history, gains of 53% in two years are possible, starting now... |

|

|

|

|