GM! Welcome to Milk Road PRO – where your weekly crypto fix is served piping hot, just like DeFi Summer vibes. |

Love $ETH? So do we. |

But what really catches our eye are those hidden gems that quietly outperform $ETH and then skyrocket. 🚀 |

Imagine catching one of these winners early… |

The trick to it is analyzing price charts in $ETH, instead of dollars. When we see an uptrend, it means the token is outpacing $ETH. |

(It’s like a secret weapon for finding potential breakout stars). |

Recently, we stumbled upon an intriguing chart showing $AAVE’s price compared to $ETH. |

|

We tried our best, but we couldn’t ignore it! Something big is brewing… and it seems like the market is yet to catch on. |

This surge isn't the result of a few people buying in here and there – it takes significant buying pressure to outperform $ETH this dramatically. |

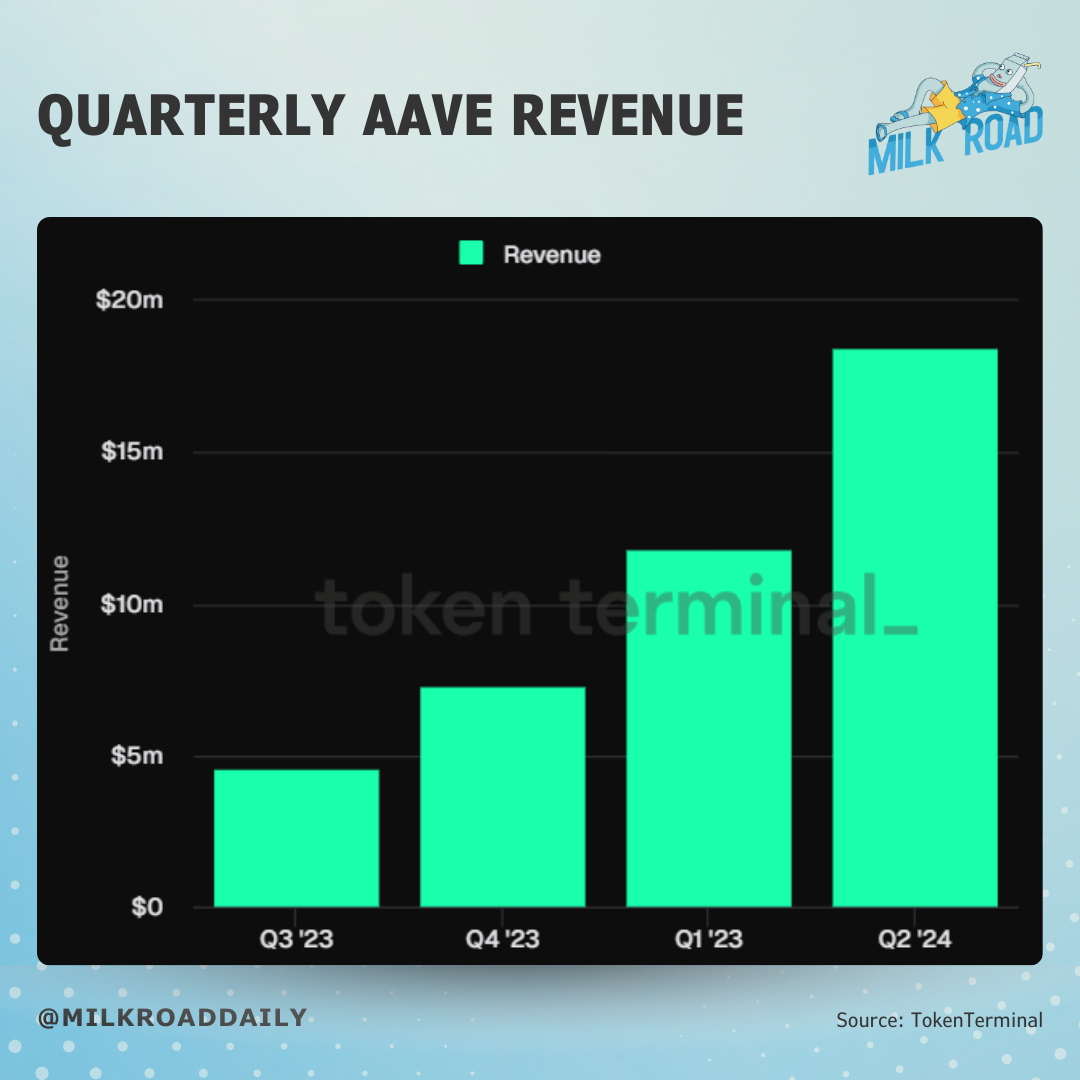

Not only that, but Aave’s revenue is on the rise. 📈 |

|

We're loving this uptrend in quarterly revenue. |

Plus, we've heard about new proposals for updated tokenomics and activating the fee switch—yet another reason this setup is impossible to ignore! |

But hold on—sometimes short-term hype or incentives inflate revenue. Is that the case with Aave, or is it a genuinely solid investment opportunity? 🤔 |

That’s the focus of our report, along with other key questions like: |

Can Aave compete with Goldman Sachs? Where are Aave's 1M users coming from? Is Aave still the market leader in the lending and borrowing sector? Is the revenue growth driven by incentives? What are the key support and resistance levels to watch for?

|

P.S. - We’re hosting a PRO AMA next week — scroll to the bottom for more info. 👀 |

And because we value everyone's time, we’re going to jump right into it. |

WHAT IS AAVE? 🤔 |

Aave, a respected pioneer in DeFi, first launched as ETHLend in 2017. |

In 2020, it rebranded to Aave and has been on quite a journey since (that's what we are exploring today)—a remarkable one at that. 👏 |

Aave is a decentralized lending platform that connects lenders and borrowers, functioning similarly to a bank. |

Users can deposit their money to earn yield, while others can borrow funds. To borrow, users must deposit collateral that exceeds their debt, ensuring repayment. |

Aave keeps the difference between the interest paid by borrowers (higher) and the interest paid to lenders (lower).💰 |

But unlike traditional banks, Aave relies on smart contracts to handle everything—no need for grumpy loan managers asking why 100% of your net worth is in crypto. 🤣 |

People love the permissionless, 24/7 access Aave offers for lending and borrowing. No KYC, no approvals, no waiting. It’s a massive improvement over traditional banking! |

So let's tap into Aave's potential. |

AAVE POTENTIAL 📈 |

Over the years, Aave has attracted substantial liquidity, further cementing its place in the DeFi space. |

Just take a look at the TVL, which shows the amount of money currently deposited in the protocol. |

|

Aave currently holds around $12 billion in Total Value Locked (TVL), which may seem small compared to major U.S. banks like JPMorgan ($2.1 trillion) or Goldman Sachs ($363 billion). |

But this ain’t a bug, it’s a feature! One that highlights the enormous market Aave could tap into. 👀 |

…ok, but how can a crypto protocol look to compete against global financial giants like JP Morgan and Goldman Sachs? |

In a single word: efficiency. |

Aave has 30 times less TVL than Goldman Sachs, but it also has 750 times fewer employees. Just take a look at the number of employees needed per $1 billion in TVL: |

|

See the difference in efficiency? We certainly do, and that's why we believe Aave could eventually disrupt these giants. |

Now, let’s dive into how Aave’s business works. |

AAVE BUSINESS MODEL 🤓 |

Aave's business model is relatively straightforward: They offer yield to lenders, charge borrowers a higher interest rate, and the difference generates the protocol's revenue—essentially the same way banks make money. |

Let’s take a look at the chart below, which shows the interest rates for lenders and borrowers of $USDC. |

|

Notice how the green line (yield for lenders) is always lower than the red line (interest for borrowers). That difference is Aave’s revenue. 🤑 |

For example: Currently, you can lend $USDC on Aave for 5.8% and borrow it for 7.6%. These percentages vary based on usage. |

We don't want to bother you with the specific formula… |

But if a bunch of $USDC is borrowed and there's not much left in reserve, the yield and interest rates will increase to attract new depositors, while discouraging additional borrowing (and vice versa). |

Pretty smart, no? |

PS: We also covered the lending sector in our PRO Report about DeFi. Feel free to read more here. |

Now that we grasp Aave’s massive potential and how it generates revenue, it’s tempting to feel bullish. 🤣 |

But hold on—we still need to dive deeper before drawing any final conclusions. |

WHERE AAVE OPERATES 🔧 |