Labor markets tighten further, according to December JOLTS report

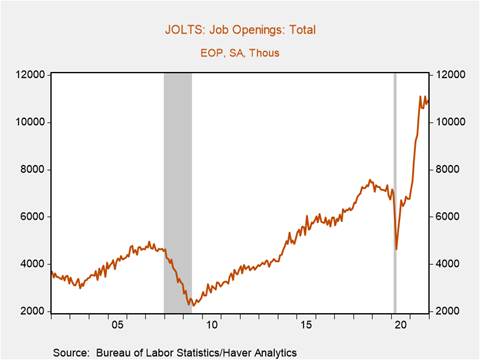

*Job openings ticked up to 10.9 million in December from an upwardly revised 10.8 million in November, 200k below their record high 11.1 million in July (Chart 1). The job opening rate was flat at 6.8%, with December’s increase in job openings led by accommodation and food services (+133k) and education and health services (+61k). The increase in job openings in the leisure and hospitality industry is notable given the emergence of the omicron variant and subsequent rise in daily COVID-19 cases, which by mid-December had reached levels comparable with the late summer delta-driven surge.

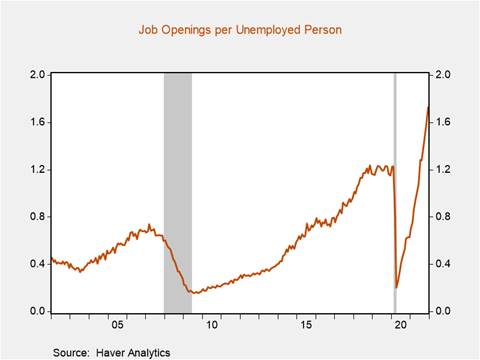

*The rise in job openings and the 500k decline in unemployment in December led to a 0.15pp rise in the number of job openings per unemployed person to a new all-time high of 1.73 (Chart 2). The increase in this measure of labor market tightness reflects the extent to which labor demand exceeds available labor supply and has contributed to the marked acceleration in employment costs, which rose 5% annualized in Q4 for service providing industries. Labor markets may have tightened further due to the rise in COVID-19 cases, which has tended to dampen the willingness of workers to take on positions in high contact, in-person industries.

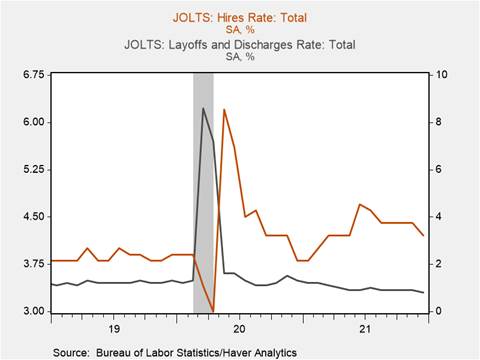

*Total hires edged down to 6.2 million (-330k), while the hiring rate fell 0.2pp to 4.2%, its lowest level since May (Chart 3). Illness, quarantines, and the deteriorating public health situation likely impaired hiring efforts in December, with notable hiring declines in professional & business services (-160k) and construction (-46k). Declining hiring in construction may reflect ongoing material constraints and adverse weather that has stalled construction and housing completions. Hiring difficulties and labor shortages prompted businesses to further reduce layoffs in an effort to hoard labor and minimize employee churn, with the layoffs and discharges rate falling to a new record low of 0.8%.

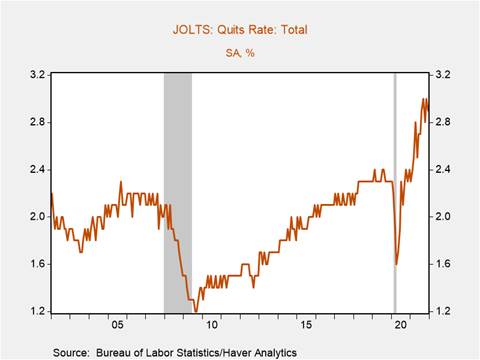

*The quits rate ticked down 0.2pp to 3.2% but remains elevated relative to its H1 2021 average of 2.8%, and suggests workers remain confident in their ability to secure new employment, albeit perhaps less so than in November (Chart 4). Notably, the quits rate declined dramatically in leisure and hospitality, falling 0.4pp to 5.8%, likely reflecting increased uncertainty among those currently employed over the impact of the omicron variant.

*The December JOLTS report indicates labor markets tightened further but does not fully reflect the impact of the omicron variant, as the seven-day moving average of daily COVID-19 case counts peaked in mid-January. Nevertheless, preliminary signs from December’s JOLTS data suggest labor shortages likely intensified in January.

Chart 1.

Chart 2.

Chart 3.

Chart 4.

Mickey Levy, mickey.levy@berenberg-us.com

Mahmoud Abu Ghzalah, mahmoud.abughzalah@berenberg-us.com

© 2022 Berenberg Capital Markets, LLC, Member FINRA and SPIC

Remarks regarding foreign investors. The preparation of this document is subject to regulation by US law. The distribution of this document in other jurisdictions may be restricted by law, and persons, into whose possession this document comes, should inform themselves about, and observe, any such restrictions. United Kingdom This document is meant exclusively for institutional investors and market professionals, but not for private customers. It is not for distribution to or the use of private investors or private customers. Copyright BCM is a wholly owned subsidiary of Joh. Berenberg, Gossler & Co. KG (“Berenberg Bank”). BCM reserves all the rights in this document. No part of the document or its content may be rewritten, copied, photocopied or duplicated in any form by any means or redistributed without the BCM’s prior written consent. Berenberg Bank may distribute this commentary on a third party basis to its customers.