| Week ending July 14, 2017 |

| Oil and metals continue to drive index higher, although the majority of the subindexes were positive |

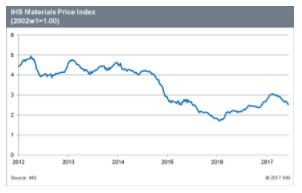

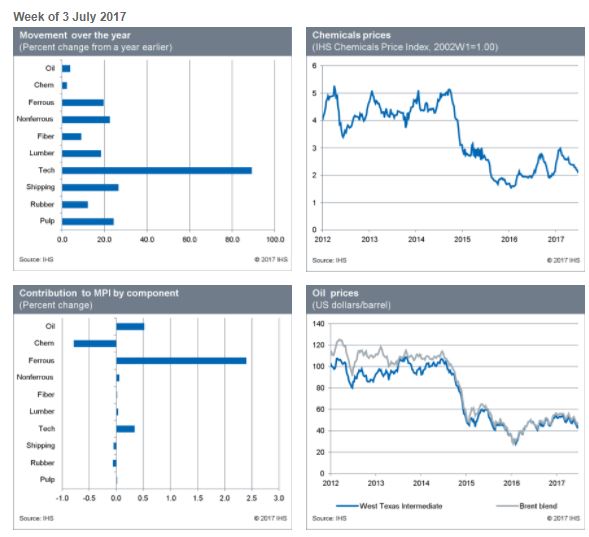

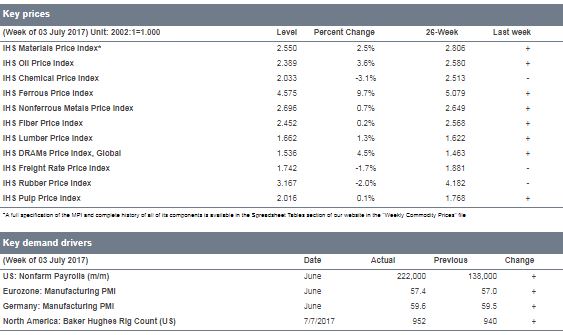

The IHS Materials Price Index (MPI) rose again last week, moving up 2.5%. Once more it was oil and metals that drove the overall index higher. Gains were not confined to these two subcategories, however. As has been the case since mid-June, gains were posted across a majority of the MPI's subcomponents.

Oil price increases early last week were not completely erased by a slump on Friday after data showed US production and rig counts rose and OPEC exports hit a 2017 high. Although the mood clearly soured Friday, with prices falling nearly 3%, gains from Monday through Thursday had ensured the oil subindex still rose 3.6% for the week. The ferrous subindex jumped 9.7% last week. Steel markets have seen a strong turnaround in sentiment over the last few weeks, with iron ore and scrap prices rebounding from May and June levels that now look too weak.

Last week positive macroeconomic announcements continued to flow in, helping improve market sentiment considerably. In Germany, the Markit Manufacturing PMI hit a fresh 74-month high, at 59.6, while the Eurozone manufacturing PMI hit 57.4—the second-quarter showing was its best reading since early 2011. In the United States, nonfarm payroll employment added 222,000 jobs in June, with revisions to prior months adding another 47,000 jobs. Tighter conditions in financial markets will act as a headwind for commodities, to be balanced against what continues to be a steady expansion in manufacturing activity. For commodities, this dynamic suggests support rather than pressure on prices.

|

|

|

| | IHS Materials Price Index |  |

|

| |

| Market Insight

For an overview of the IHS Materials Price Index, view this video.

Get the Materials Price Index delivered to your in-box weekly.

Subscribe here.

|

|  |

| | |

|

| Industrial Materials: Prices |  |

| Key Prices & Demand Drivers |  |

Construction Materials and Equipment Cost Escalation Hit Lowest Level This Year

|

Construction costs rose again in June, according to IHS Markit and the Procurement Executives Group (PEG). |

The headline IHS Markit PEG Engineering and Construction Cost Index registered 51.5, down from 54.0 in May, indicating less broad price increases across the industry. Both the material/equipment and labor categories continue to record higher prices. The materials/equipment price index came in at 51.3 in June, its lowest level in seven months. Price increases were uneven with only six of the 12 categories tracked in the materials sub-index showing higher prices, three categories registered flat pricing, and three had falling prices. Although structural steel and steel pipe prices have backed off from this spring’s peaks, anxiety about the pending Section 232 trade case decision continues. “Steel pipe prices have peaked for the time being and prices for certain products have started to fall,” said Amanda Eglinton, senior economist at IHS Markit. “However, there is still tightness in products such as oil country tubular goods (OCTG) and line pipe, where demand remains elevated. There is high potential for further tightening pending the outcome of the Section 232 trade case. If pipe is included in the scope of this case and imports are restricted, prices will spike again and supply will be very tight. If pipe is not included, steel pipe prices will continue to soften with lower steel input costs.”

| | Learn More |

|

| About IHS Pricing & Purchasing | | The IHS Pricing & Purchasing Service | The IHS Pricing & Purchasing Service enables supply chain cost savings by providing timely, accurate price forecasts and cost analysis. Armed with a better understanding of suppliers' cost structures and market dynamics, organizations can effectively negotiate prices, strategically time buys, and boost the bottom line.

With a database of more than 80,000 historic prices and thousands of price, wage and input cost forecasts, IHS offers more coverage than any other provider in the market. IHS has been providing forecasts of key commodity, labor, and input costs since 1970 -- helping define the purchasing advice industry. | | Learn More |

|

| Commodity Price Forecasts & Supply Chain Cost Benchmarking. Learn More | | |

|

|

|