| -- | John Mauldin | Apr 21, 2017 Taxes Are Worse Than You Thought “It is a paradoxical truth that tax rates are too high today and tax revenues are too low, and the soundest way to raise the revenues in the long run is to cut the tax rates.” – John F. Kennedy (Yes, a Democratic president back in the Camelot days of the early ’60s wanted to slash taxes.) This week’s Outside the Box will make half of my readers indignant and the other half feel righteously vindicated in their thinking. I have no idea which half you are in. What is so controversial? Who pays taxes and why they should. Today’s letter was sent to me by reader Tom Bentley. It bears the in-your-face title “Taxes Are Worse Than You Thought.” It’s by Mark J. Perry, whose bio tells us that he’s a scholar at the American Enterprise Institute and a professor of economics and finance at the University of Michigan. So yes, he is a conservative. The point Mark is trying to make is that the top 1%/5%/10% are already paying the bulk of the income tax. From his viewpoint that is fair, or even more than fair. Although I will point out that he does include a chart which shows that the progressivity of tax rates, which climb relentlessly upward with income, surprisingly fails at incomes of over $10 million. I assume that is because at that point capital gains tax and other tax-incentivized income comes into play that is typically not available to those of us with merely mortal incomes. These statistics come from government data. I’ve seen the same type of data demonstrated before in other venues, so there is not much disputing Perry’s facts. I doubt this piece will make those who feel that “the rich” should pay more change their minds. What I would point out, in the vein of the philosophy that my dad regularly quoted to me, is that you can’t squeeze blood from a turnip. There is only so much more income tax that we can extract from the top income tier of the country without doing serious damage to the economy. As Tom said in his note to me accompanying the link, Politicians of all stripes seem to constantly champion middle-class tax cuts, yet it’s the highly progressive nature of our tax code that’s at the root of secular stagnation and social division. If we look at net taxes (after netting out the money we get back in entitlements), 60% of Americana pay zero, 30% pay their proportional (by headcount) share, and the top 10% pay for themselves and for the bottom 60%. No other advanced country has anywhere near that much progressivity, because most all other countries have a VAT that spreads taxes more evenly. Democrats oppose a VAT for that very reason, while Republicans oppose it based on slippery-slope reasoning (they think a VAT makes it too easy to raise taxes further, though that makes little sense – why would it be easier to raise a tax that hits most everyone, rather than just impose higher taxes on the top 5%?). Yes, Europea ns have a VAT and have very high taxes, but poll after poll shows that Europeans have a far more sympathetic view toward taxation than Americans do (no surprise there, we were founded based on our opposition to taxes). We should not be confusing correlation with causation; it leads to sloppy thinking and terrible policies each and every time. Mark provides us with some excellent data to look at our tax code for the FUBAR system it really is, including the damage done by its complexity. In a better world, only the top 10% would pay an income tax, and they would file it on a single sheet of paper – add up all income from all sources, no deductions, multiply by the percentage, and write the check. All other federal taxes (except tariffs and excise taxes), including corporate and payroll taxes, would be eliminated, and replaced by a VAT. The EITC would be invigorated so that those at the lowest income levels got their VAT rebated, to assuage those who get their knickers in a twist about the regressivity of VAT and excise taxes. Prices would go up to reflect the VAT, but capacity to pay would go up also as payroll taxes are eliminated. A system like this is the economic “ideal”; the boom it would creat e would be huge and lasting – and it has no chance of happening. Tom is basically echoing a theme that I’ve been developing for months (which is maybe why I like it): If we really want to reform the tax system, we’re going to have to develop a consumption-based tax, either some form of a VAT or even a carbon-based tax, which is just another consumption tax. The Fair Tax advocates will philosophically agree, although they prefer a direct sales tax, which I think has implementation issues. And as Tom says and I have noted, you could greatly reduce income taxes and get rid of the Social Security tax altogether if you introduced a VAT. Let me be clear: The next time we have a crisis and Democrats are in control of the White House and Congress (and after almost 50 years of observing political to-ing and fro-ing, I consider that a near certainty), the only alternative will be for the Democrats to introduce and pass some form of a value-added tax, which will not be accompanied by income tax cuts. Income tax cuts for the upper end of the income spectrum is just not on their agenda. They don’t understand the philosophical or economic reasons why that is something that should be done. I’m not asking them to here – that’s a debate for another day. I’m just saying that if Republicans don’t wake up and introduce a VAT in a manner that they can live with, they’re going to have it shoved down their throats in a far more devastating and complicated manner. And that’s a fact, Jack. If you want real change, dude, you have to make real change. Accept no substitutes. Seriously, the Washington Post tells me the White House is now considering a VAT or carbon tax – interestingly, a few weeks after I wrote my five-part series suggesting the same thing and trashing the border adjustment tax as a guaranteed trigger of a global recession/depression. I find it encouraging that Peter Navarro, Trump’s Director of Trade and Industrial Policy, is apparently being relegated to the sidelines, at least philosophically (which is all I care about – I’m sure he’s is a nice guy, and I wish him all the best personally). I will certainly be glad to sit down and talk with anyone about the logistics and implementation issues around creating a consumption tax that actually, seriously cuts corporate and income taxes, making this country competitive again. If you want to even have a ghost of a chance of avoiding a recession within the next four years, you’re going to have to have real change. Tinkering with a few points here and there with regard to income tax levels is just not going to cut it. It’s all about incentives. And there are ways to create incentive structures that you can bring Democrats on board with, so it can be a bipartisan initiative. It turned out to be a bad thing that the Democrats shoved healthcare reform down the Republicans’ throats without one Republican vote, and it would be just as bad if Republicans were to shove tax reform down Democrats’ throats without one Democratic vote. We’re all in this together, believe it or not, and we need to figure out a solution that works. And you had better forget about partisan purity if you really want the economy to thrive again. Yes, I’m a dreamer. Sigh. But if we don’t achieve something like the dream I’ve outlined, then you’d better hunker down for more slow recovery, followed closely by the Mother of All Recessions. I’m quite serious about that and will be writing about it over the next few weeks. Meaningless “tax reform,” which only messes around at the edges, will not keep us out of the next recession, which will likely be triggered from Europe. Now, on to better and brighter things. Texas is experiencing one of the finest springs I can remember. We’ve been dining out at night, spending time with friends, and just simply enjoying the atmosphere, which has been awesome. I hope that wherever you are – and with my readership, that means pretty much all over the world –you get to experience a prolonged period of meteorological bliss like the one we have enjoyed the last few weeks and months. On a personal note, I think I’ve recently held more meetings and especially telephone conference calls, reviewed more agreements, and tried to do more research and writing than at any one time in my life. It is exhausting, but at the same time I don’t want to change anything; I just want to get to some finish lines. I swear – and this time I really mean it – that when I finally finish with all these deadlines I have in front of me, I will not commit to anything other than researching and writing this letter and taking care of a few obvious business maintenance matters for at least six months to a year. And Shane is pointing out to me that at some point in time we actually do need to go away to get married and have a honeymoon. Yes, that is kind of a backdoor announcement… and her deadline is becoming something of a critical path. As in, I really do have to meet it. I can’t postpone it like I have been with some of my other deadlines. And then there is the 2017 edition of our SIC conference, which is going to kick off in about one month and is going to be the most awesome thing in the world that I have ever done. You really do want to be there. They tell me we are down to about 35–40 spots left, so stop procrastinating and figure out how to get to Orlando May 22-25. And with that I must hit the send button. You have a great week, and now let’s let Mark talk to us about the distribution of income and taxes. Your “Oh deadline, where is thy sting?” analyst,

John Mauldin, Editor

Outside the Box

JohnMauldin@2000wave.com

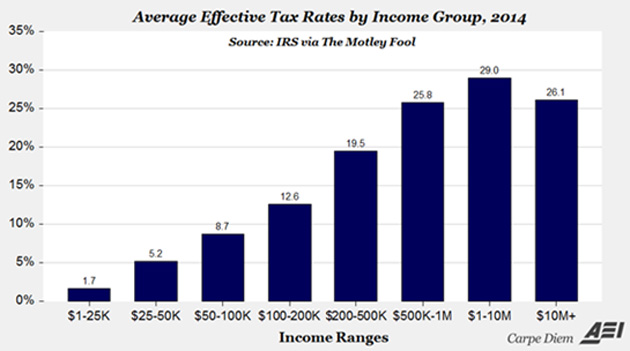

Taxes Are Worse Than You Thought By Mark J. Perry

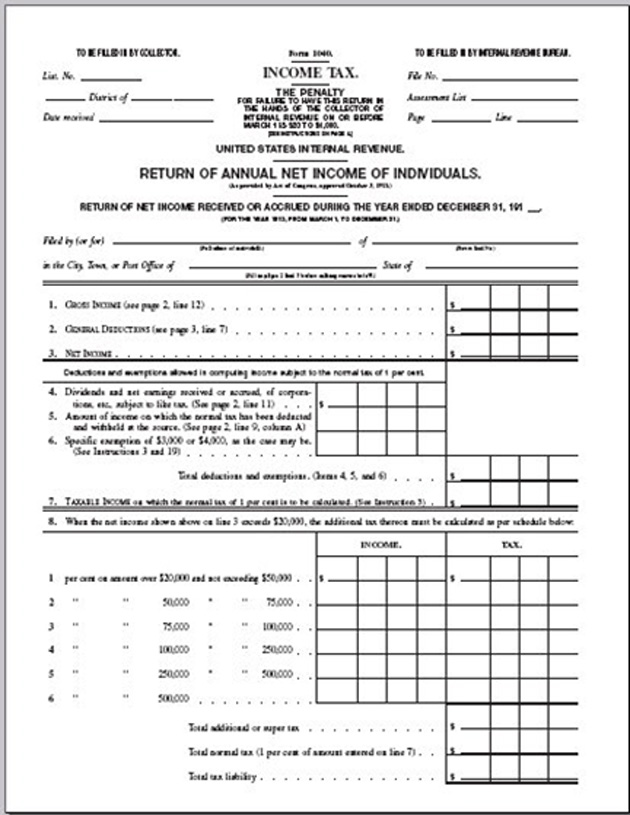

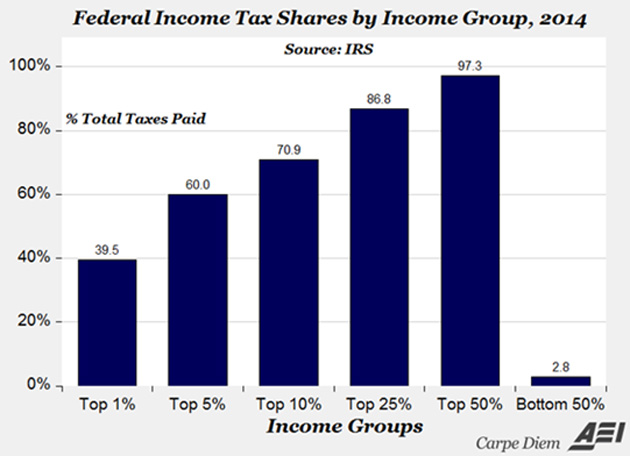

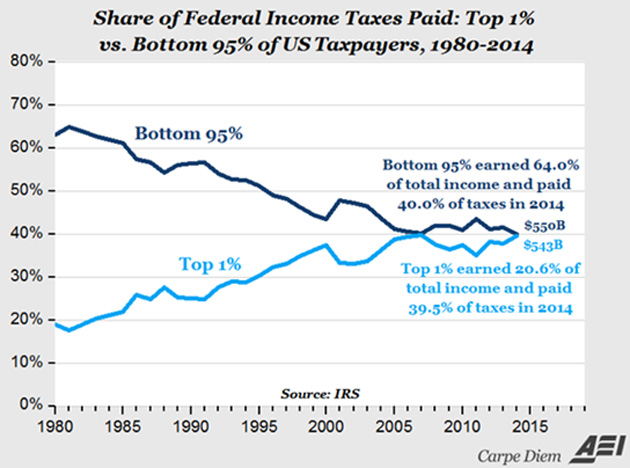

Originally published by the American Enterprise Institute, April 16, 2017 We are quickly approaching the deadline for filing (and paying) our federal and state income taxes (extended to April 18 this year because of Emancipation Day), and that means it’s time for my annual post at tax time to help put things in perspective. 1. Some Historical Perspective. “In the beginning” when the US federal income tax was first introduced in 1913, it used to be a lot, lot simpler and a lot easier to file taxes; so easy in fact that it was basically like filling out your federal tax return on a postcard.  For example, page 1 of the original IRS 1040 income tax form from 1913 appears above. There were only four pages in the original 1040 form, including two pages of worksheets, the actual one-page 1040 form above, and only one page of instructions (view all four pages here). In contrast, just the current 1040 instructions for 2016, without any forms, runs 106 pages. Individual federal income tax rates started at 1% in 1913, and the maximum marginal income tax rate was only 7% on incomes above $500,000 (more than $12 million in today’s dollars). The personal exemption in 1913 was $3,000 for individuals ($72,850 in today’s dollars) and $4,000 for married couples ($97,000 in today’s dollars), meaning that very few Americans had to pay federal income tax since the average income in 1913 was only about $750. The Tax Foundation has historical federal income tax rates for every year between 1913 and 2013 here for tax brackets expressed in both nominal dollars and inflation-adjusted dollars.  2. Tax Graphic of the Day (above). Some more historical perspective… 3. Opportunity Cost. In a 2012 report to Congress (most recent data available), the National Taxpayer Advocate estimated that American taxpayers and businesses spend 6.1 billion hours every year complying with the income tax code, based on IRS estimates of how much time taxpayers (both individual and businesses) spend collecting data for, and filling out their tax forms. In addition, Americans will spend an estimated $10 billion for the services of tax preparation firms and $2 billion on tax-preparation software programs like TurboTax that still require many hours of time. The amount of time spent on income tax compliance – 6.1 billion hours – would be the equivalent of more than 3 million Americans working full-time, year-round (or 2.1% of total US payrolls of 145.9 million). By way of comparison, the federal government currently employs 2.8 million full-time workers, and Wal-Mart, the world’s largest private employer, currently employs 2.2 million workers worldwide and 1.3 million workers in the US (both full-time and part-time). At the current average hourly wage of $21.90 an hour, the dollar value of the opportunity cost associated with tax filing would be more than $131 billion, slightly more than the 2016 GDP of Washington, D.C. ($127 billion). As T.R. Reid pointed out recently in a New York Times op-ed, it really doesn’t have to be that way. For example: In Japan, you get a postcard in early spring from Kokuzeicho (Japan’s IRS) that says how much you earned last year, how much tax you owed, and how much was withheld. If you disagree, you go into the tax office to work it out. For nearly everybody, though, the numbers are correct, so you never have to file a return.  4. Tax Progressivity. And just how progressive is the US federal income tax system? Very, very progressive, see the chart above showing average effective tax rates by various income groups in 2014 (most recent year available). That pattern of income tax progressivity explains why almost all federal income taxes are paid by the top income groups (see next few items).  5. Tax Progressivity and Tax Burden. According to the most recent IRS data, the federal income tax shares by six different income groups are displayed in the chart above. Almost all federal income taxes (97.3%) are paid by the top 50%, more than 2/3 of income taxes are paid for by the top 10% and nearly 40% of taxes are paid by the top 1% of taxpayers. For all of the criticism and negative publicity the “Top 1%” get, I’d like to personally thank that group this year at tax time for shouldering such a disproportionate share of our collective tax burden. It’s a form of “disparate impact” on the 1% that we all benefit from! So, I say “Thank You Top 1%” from all of us in the bottom 99% for your valuable and significant contribution to our nation’s tax burden.  6. Tax Burden of the Top 1% vs. the Bottom 95%. The chart above gives us another perspective on the tax burden of the top 1% over time, and compares the tax share of that group to the tax burden of the bottom 95% in every year between 1980 and 2014 (most recent year available). In 2014, the top 1% earned 20.6% of the total income reported to the IRS and paid 39.4% of all federal income taxes collected ($543 billion). The bottom 95% of US taxpayers earned 64% of total income (almost three times as much as the top 1%) and paid only 40.5% of the total income taxes collected ($550 billion). So once again, to the 1.395 million taxpayers in the top 1%, I say “Thank You” for paying almost as much in federal income taxes in 2013 as the 132.6 million taxpayers in the bottom 95% by income. 7. Bowling vs. Taxes. Speaking of the progressivity of income taxes, here’s a thought about the way we tax income vs. the way we score bowling. Under the scoring rules of bowling, you get rewarded, not penalized, for being successful. If you get a spare, the scoring system rewards you by adding the pins from the next ball into the current frame, and if you get a strike you get rewarded by adding your next 2 balls into the current frame. Under our progressive income tax system with seven tax rates in 2015 increasing from 10% to 39.6%, you get penalized, not rewarded, for being successful, productive and entrepreneurial, because the more you earn, the higher the tax rate you pay. The top marginal income tax rate has been as high as 91% in the 1950s and 1960s, and 70% in the 1970s. If we scored bowling the way we tax income, we would subtract, not add pins for a spare or strike, i.e., penalize successful bowling. If we taxed income the way we score bowling, we would have lower, not higher, tax rates on our most successful income-earners. 8. Coincidence? Why are Tax Day (April 15) and Voting Day (first Tuesday in November) so far apart? Couldn’t we move Tax Day to the first Monday in November, or Voting Day to the first Tuesday following April 15? 9. What’s in a Name? Why do we call the IRS a “service?” Couldn’t it have been named a department like Labor, a bureau like the BLS or the FBI, a commission like the FTC, an administration like FDA, an agency like EPA, etc.? 10. 20 Inspirational Quotes about Taxes from Forbes, here are a few good ones: “The taxpayer: that’s someone who works for the federal government, but doesn’t have to take a civil service examination.” – Ronald Reagan “We have what it takes to take what you have.” – Suggested IRS Motto “It is a paradoxical truth that tax rates are too high today and tax revenues are too low, and the soundest way to raise the revenues in the long run is to cut the tax rates.” – John F. Kennedy I am proud to be paying taxes in the United States. The only thing is I could be just as proud for half of the money.” – Arthur Godfrey “A liberal is someone who feels a great debt to his fellow man, which debt he proposes to pay off with your money.” – G. Gordon Liddy Happy Tax Day!

| Get Varying Expert Opinions in One Publication with John Mauldin’s Outside the Box

Every week, celebrated economic commentator John Mauldin highlights a well-researched, controversial essay from a fellow economic expert. Whether you find them inspiring, upsetting, or outrageous... they’ll all make you think Outside the Box. Get the newsletter free in your inbox every Wednesday. |

Share Your Thoughts on This Article

http://www.mauldineconomics.com/members Outside the Box is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting http://www.mauldineconomics.com. To subscribe to John Mauldin's e-letter, please click here:

http://www.mauldineconomics.com/subscribe Outside the Box and MauldinEconomics.com is not an offering for any investment. It represents only the opinions of John Mauldin and those that he interviews. Any views expressed are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest and is not in any way a testimony of, or associated with, Mauldin's other firms. John Mauldin is the Chairman of Mauldin Economics, LLC. He also is the President of Millennium Wave Advisors, LLC (MWA) which is an investment advisory firm registered with multiple states, President and registered representative of Millennium Wave Securities, LLC, (MWS) member FINRA and SIPC, through which securities may be offered. MWS is also a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB) and NFA Member. Mill ennium Wave Investments is a dba of MWA LLC and MWS LLC. This message may contain information that is confidential or privileged and is intended only for the individual or entity named above and does not constitute an offer for or advice about any alternative investment product. Such advice can only be made when accompanied by a prospectus or similar offering document. Past performance is not indicative of future performance. Please make sure to review important disclosures at the end of each article. Mauldin companies may have a marketing relationship with products and services mentioned in this letter for a fee. Note: Joining the Mauldin Circle is not an offering for any investment. It represents only the opinions of John Mauldin and Millennium Wave Investments. It is intended solely for investors who have registered with Millennium Wave Investments and its partners at www.MauldinCircle.com or directly related websites. The Mauldin Circle may send out material that is provided on a confidential basis, and subscribers to the Mauldin Circle are not to send this letter to anyone other than their professional investment counselors. Investors should discuss any investment with their personal investment counsel. John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker ( IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private and non-private investment offerings with other independent firms such as Altegris Investments; Capital Management Group; Absolute Return Partners, LLP; Fynn Capital; Nicola Wealth Management; and Plexus Asset Management. Investment offerings recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements. PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER. Alternative investment performance can be volatile. An investor could lose all or a substantial amount of his or her investment. Often, alternative investment fund and account manager s have total trading authority over their funds or accounts; the use of a single advisor applying generally similar trading programs could mean lack of diversification and, consequently, higher risk. There is often no secondary market for an investor's interest in alternative investments, and none is expected to develop. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs may or may not have investments in any funds cited above as well as economic interest. John Mauldin can be reached at 800-829-7273. | -- |