| Week ending December 15, 2017 |

Commodity prices advance strongly, driven by rubber and steel

|

The gains last week were driven by a small subset of commodities, with the broader market posting a sequence of small declines.

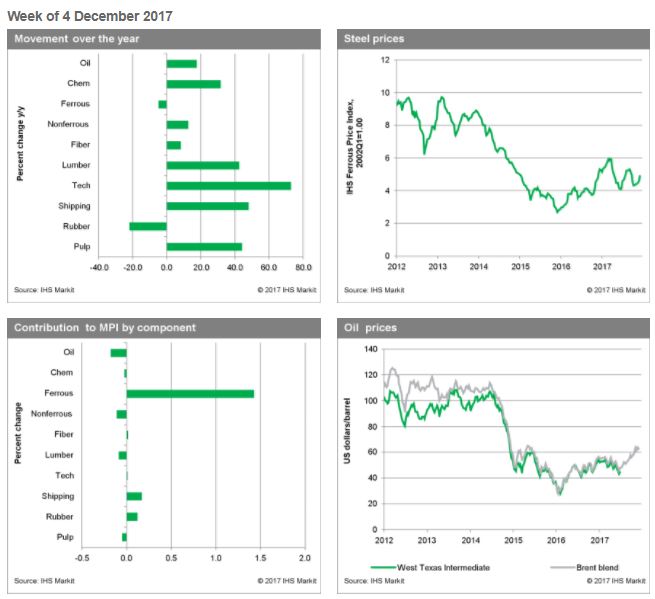

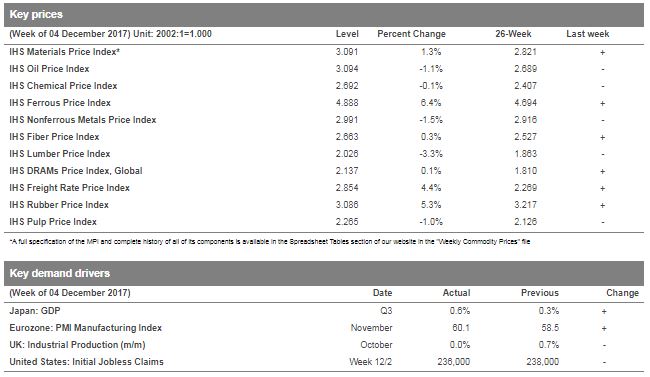

The IHS Materials Price Index (MPI) rose 1.3% last week, hitting its highest level since late 2014. Gains were concentrated in three areas: ferrous metals, rubber, and freight, all of which posted large jumps.

Steel markets have been in a strong uptrend over the last two weeks, with unseasonably warm weather in China helping to prolong the building season. Steady demand has pressured already-tight markets caused by government-mandated cuts in production to meet pollution targets. Rubber prices have also been moving higher recently in reaction to a set of factors—a pledge by rubber producers to cut exports, a warehouse fire in Shanghai that damaged a significant block of inventory, and the Thai government’s plan to increase buffer stock purchases in 2018.

Recent macroeconomic data has added to the buoyant mood in commodity markets. US employment growth for November came in above expectations, highlighting yet again solid labor market conditions leading into 2018. In the Eurozone, November’s manufacturing PMI reading moved up 1.5 points, to 60.0, with Germany hitting 62.5, the highest level since 2011. In Japan, the second reading third-quarter GDP showed 0.6% growth, a doubling from the prior period, driven by stronger private nonresidential investment. Despite these positive demand-side drivers, we expect the New Year to bring slower growth in China, a tightening in financial markets, and slightly lower oil prices, a combination that will cap commodity prices and stem the buildup of pressure in supply chains.

|

|

|

| | IHS Materials Price Index |  |

|

| |

| Market Insight

For an overview of the IHS Materials Price Index, view this video.

Get the Materials Price Index delivered to your in-box weekly.

Subscribe here.

|

|  |

| | |

|

| Industrial Materials: Prices |  |

| Key Prices & Demand Drivers |  |

Construction Labor Costs Reach Highest Level in Almost Three Years, IHS Markit Says

|

Construction costs rose again in November, according to IHS Markit and the Procurement Executives Group (PEG). |

The current headline IHS Markit PEG Engineering and Construction Cost Index registered 60.2, supported by strong figures in both the materials/equipment and labor sub-indexes. The materials/equipment price index was 60.9 in November, moving up from the October figure of 58.9. Price increases were widespread. Current subcontractor labor prices rose at a fast pace in November: the index figure came in at 58.5, the highest reading since December 2014. “Subcontractor rates continued to accelerate over November and expectations for future increases reached a five-year high,” said Emily Crowley, principal economist - pricing and purchasing, IHS Markit. “Tightening labor market conditions combined with an uptick in activity are driving expectations of future rate increases. Currently the U.S. South and West are having the most trouble finding workers leading to stronger wage escalation, whereas the end of major projects in Eastern Canada are keeping pressure off of wages in that region.”

| | Learn More |

|

| About IHS Pricing & Purchasing | | The IHS Pricing & Purchasing Service | The IHS Pricing & Purchasing Service enables supply chain cost savings by providing timely, accurate price forecasts and cost analysis. Armed with a better understanding of suppliers' cost structures and market dynamics, organizations can effectively negotiate prices, strategically time buys, and boost the bottom line.

With a database of more than 80,000 historic prices and thousands of price, wage and input cost forecasts, IHS offers more coverage than any other provider in the market. IHS has been providing forecasts of key commodity, labor, and input costs since 1970 -- helping define the purchasing advice industry. | | Learn More |

|

| Commodity Price Forecasts & Supply Chain Cost Benchmarking. Learn More | | |

|

|

|