| Week ending August 25, 2017 |

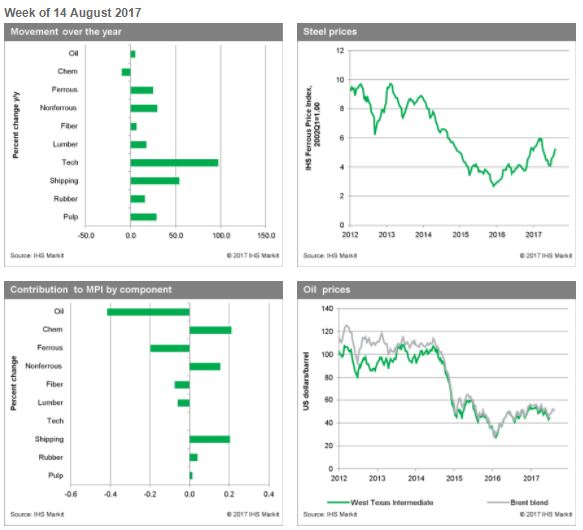

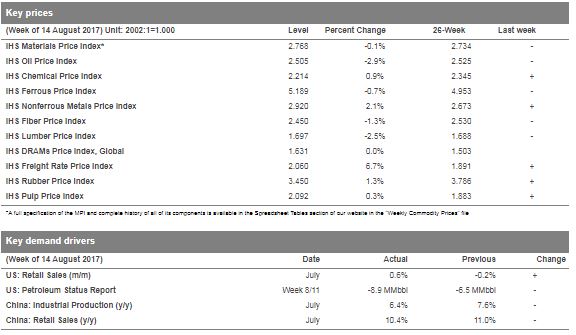

The IHS Materials Price Index fell 0.1% last week, marking a pause in the rally that started in late June. Four of the ten sub-indexes declined, led by lumber and oil, which dropped by 2.9% and 2.5%, respectively. Shipping rates increased a strong 6.7%, while nonferrous metals moved up another 2.1%.

Despite a drop of 6.5 million barrels in crude inventories last week and a decline in the Baker Hughes rig count, oil prices fell. While demand growth looks healthy over the near term, increases in production look to keep the market well supplied, with prices expected to fall in early 2018. Lumber prices have appeared to advance in front of fundamentals recently and, hence, some give back in prices was not unexpected. Prices could retreat further before the final decision on countervailing and antidumping duties on Canadian imports is rendered in Washington.

Economic reports last week in the United States were largely positive, but reports coming from China disappointed. US retail sales grew by 0.6% month on month (m/m), beating expectations. The University of Michigan consumer sentiment survey shot higher to 97.6, also stronger than expected. Meanwhile, fresh Chinese data showed signs of slowing GDP growth, a potential headwind for commodity prices in the fourth quarter. Industrial production grew at 6.4% year on year (y/y) in July, lower than market expectations, while retail sales also slowed.

Markets seemed to lose some momentum last week. Volatility has increased recently, perhaps a sign that the optimism that has carried the market in the third quarter is beginning to dissipate. Our view remains that the strong rebound in prices over the past seven to eight weeks cannot continue given our fundamental picture of the near term.

|

|

|

| | IHS Materials Price Index |  |

|

| |

| Market Insight

For an overview of the IHS Materials Price Index, view this video.

Get the Materials Price Index delivered to your in-box weekly.

Subscribe here.

|

|  |

| | |

|

| Industrial Materials: Prices |  |

| Key Prices & Demand Drivers |  |

Construction Materials and Equipment Cost Escalation Hit Lowest Level This Year

|

Construction costs rose again in June, according to IHS Markit and the Procurement Executives Group (PEG). |

The headline IHS Markit PEG Engineering and Construction Cost Index registered 51.5, down from 54.0 in May, indicating less broad price increases across the industry. Both the material/equipment and labor categories continue to record higher prices. The materials/equipment price index came in at 51.3 in June, its lowest level in seven months. Price increases were uneven with only six of the 12 categories tracked in the materials sub-index showing higher prices, three categories registered flat pricing, and three had falling prices. Although structural steel and steel pipe prices have backed off from this spring’s peaks, anxiety about the pending Section 232 trade case decision continues. “Steel pipe prices have peaked for the time being and prices for certain products have started to fall,” said Amanda Eglinton, senior economist at IHS Markit. “However, there is still tightness in products such as oil country tubular goods (OCTG) and line pipe, where demand remains elevated. There is high potential for further tightening pending the outcome of the Section 232 trade case. If pipe is included in the scope of this case and imports are restricted, prices will spike again and supply will be very tight. If pipe is not included, steel pipe prices will continue to soften with lower steel input costs.”

| | Learn More |

|

| About IHS Pricing & Purchasing | | The IHS Pricing & Purchasing Service | The IHS Pricing & Purchasing Service enables supply chain cost savings by providing timely, accurate price forecasts and cost analysis. Armed with a better understanding of suppliers' cost structures and market dynamics, organizations can effectively negotiate prices, strategically time buys, and boost the bottom line.

With a database of more than 80,000 historic prices and thousands of price, wage and input cost forecasts, IHS offers more coverage than any other provider in the market. IHS has been providing forecasts of key commodity, labor, and input costs since 1970 -- helping define the purchasing advice industry. | | Learn More |

|

| Commodity Price Forecasts & Supply Chain Cost Benchmarking. Learn More | | |

|

|

|