| Week ending September 29, 2017 |

The MPI returns to growth after falling last week

|

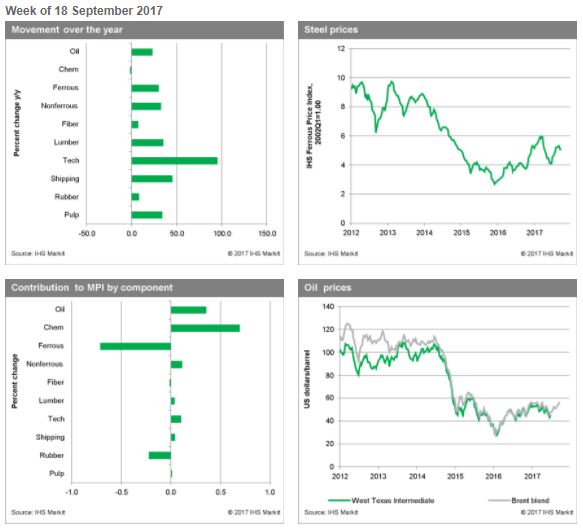

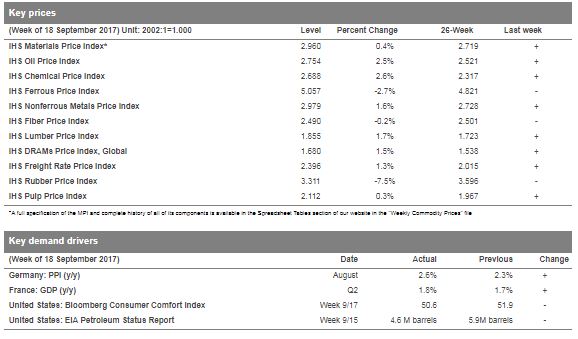

The IHS Markit Materials Price Index (MPI) increased a small 0.4% last week, a slight gain after slipping the week before. Though modest, the increase was broadly based, with eight of ten sub-indexes rising. Oil prices and chemicals led the rebound, gaining by 2.5% and 2.6%, respectively. Rubber was a source of weakness last week with prices dropping 7.5%. Prices are down more than 10% in the past two weeks as inventory has been rising steadily all year and finally seems to be weighing on prices.

Oil prices rallied last week as refinery capacity on the Gulf Coast continued to come back online. Global demand remains strong; when coupled with logistics problems related to Hurricane Harvey, it helped to push prices higher. In the near term, upside price risk for crude markets is limited, however; we expect a global surplus to reemerge before the end of 2017.

The economic calendar was dominated last week by the US Federal Reserve's September meeting. As expected, the Fed outlined its plans to shrink its balance sheet, which will begin in October. The two-day meeting also gave a clear indication that a December rate hike is very much in play, something markets had been discounting just a few weeks ago. These moves highlight the normalization of financial markets now taking place. The process began over a year ago and will continue over the near term with a slow tightening taking place not just in the United States, but also in the United Kingdom, the Eurozone, and China. This change in financial markets is one of three factors (the others being slower growth in China and lower oil prices) that will check a strong sustained rally in commodity prices.

|

|

|

| | IHS Materials Price Index |  |

|

| |

| Market Insight

For an overview of the IHS Materials Price Index, view this video.

Get the Materials Price Index delivered to your in-box weekly.

Subscribe here.

|

|  |

| | |

|

| Industrial Materials: Prices |  |

| Key Prices & Demand Drivers |  |

Construction Costs Rise for 10th Consecutive Month

|

Construction costs rose again in August, according to IHS Markit and the Procurement Executives Group (PEG).

|

The headline IHS Markit PEG Engineering and Construction Cost Index registered 54.0, up from 51.3 in July. Both material/equipment and labor sub-indexes registered rising prices.

The materials/equipment price index registered 54.2 in August, slightly higher than the July figure of 52.4. Price increases were uneven. Copper-based wire and cable increased once again, approaching the index figures last seen at the beginning of 2017.

“Commodity prices have risen strongly in the past seven weeks, with copper on the London Metal Exchange, jumping 14 percent between early June and August,” said John Mothersole, director Pricing and Purchasing, IHS Markit. “Better data from China, a softer U.S. dollar and new fears about mine supply disruptions have combined to lift prices. The market, however, looks overbought. If possible, we would avoid purchases at the moment and await what we believe will be a modest correction.”

| | Learn More |

|

| About IHS Pricing & Purchasing | | The IHS Pricing & Purchasing Service | The IHS Pricing & Purchasing Service enables supply chain cost savings by providing timely, accurate price forecasts and cost analysis. Armed with a better understanding of suppliers' cost structures and market dynamics, organizations can effectively negotiate prices, strategically time buys, and boost the bottom line.

With a database of more than 80,000 historic prices and thousands of price, wage and input cost forecasts, IHS offers more coverage than any other provider in the market. IHS has been providing forecasts of key commodity, labor, and input costs since 1970 -- helping define the purchasing advice industry. | | Learn More |

|

| Commodity Price Forecasts & Supply Chain Cost Benchmarking. Learn More | | |

|

|

|