| Week ending October 13, 2017 |

The MPI undergoes its sharpest drop since early June

|

The latest data from commodity markets reaffirm our outlook of limited upside risk in the near term.

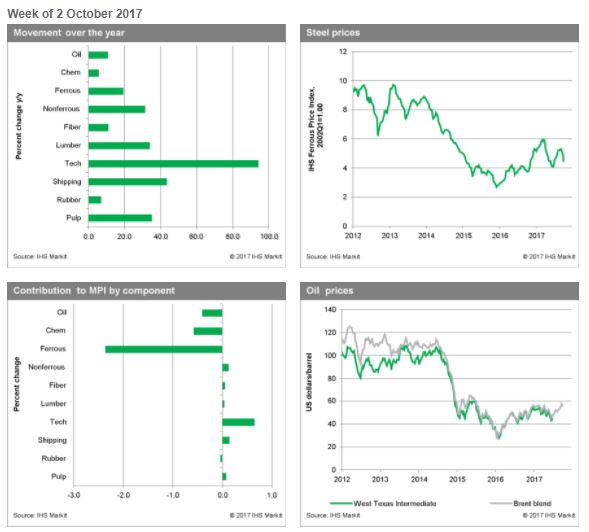

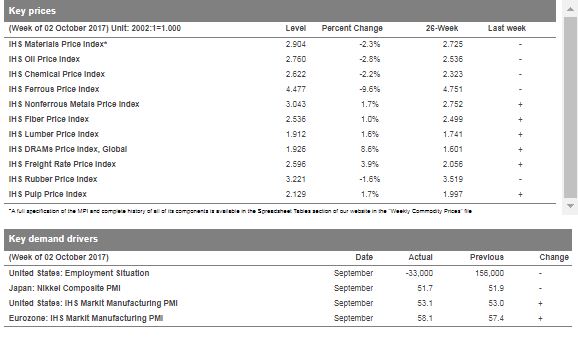

The IHS Markit Materials Price Index (MPI) fell by 2.3% last week, its largest decline since early June. Only four subindexes, principally ferrous metals and oil, fueled the fall. Ferrous metals plummeted 9.6%, while oil prices fell 2.8%. Alternatively, the DRAM subindex surged 8.6%, dulling the price declines in other commodity markets. Indeed, this latest movement in the MPI further indicates that upside risk is limited, a trend that has begun to emerge.

Ferrous metals prices reached levels beyond what market fundamentals dictated, as a speculative spike in China created a bubble; that bubble is now popping as ore prices are falling sharply and scrap prices are following suit. As for DRAMs, supply constraints are keeping the market tight, pushing up prices. Furthermore, buyers are transitioning from lower density, less expensive DRAMs to higher density, more expensive DRAMs, putting upward price pressure on the subindex.

Data releases reflected the tepid mood in global markets last week. In the United States, the Department of Labor reported that nonfarm payrolls declined by 33,000 in September, a stark contrast to our expectation of an addition of 80,000 jobs. While nonfarm payrolls declined, wages surged by 0.5% month on month (m/m), the strongest gain of the expansion. Meanwhile, the IHS Markit US Manufacturing PMI report met expectations, coming in at 53.1. In Japan, the Nikkei Composite PMI fell to 51.7, as stronger conditions in the manufacturing sector were outweighed by weakness in the services sector. In the Eurozone, our Manufacturing PMI report was a bit brighter, as it came in at a strong 58.1. We expect upside risk for commodities will remain limited in the near term, as Chinese growth slows and oil prices continue to fall.

|

|

|

| | IHS Materials Price Index |  |

|

| |

| Market Insight

For an overview of the IHS Materials Price Index, view this video.

Get the Materials Price Index delivered to your in-box weekly.

Subscribe here.

|

|  |

| | |

|

| Industrial Materials: Prices |  |

| Key Prices & Demand Drivers |  |

Construction Costs Rise to Highest Point in Past Year, IHS Markit says

|

Construction costs rose to the highest point in the last year in September, according to IHS Markit and the Procurement Executives Group (PEG). |

The headline IHS Markit PEG Engineering and Construction Cost Index registered 58.4, up from 54.0 in August. Both material/equipment and labor sub-indexes registered rising prices. Ocean freight, both from Asia to the U.S. and Europe to the U.S. were among the largest movers compared to last month.

“Global demand for marine transportation is improving, both in the bulk segment and in the container segment,” said Paul Robinson, associate director, Pricing and Purchasing at IHS Markit. “On the bulk side, the primary driver is food products, on the container side, intraregional trade is driving some of the gain, especially in East Asia. Buyers outside of the United States should avoid locking in rates until prices pull back in 2018.”

| | Learn More |

|

| About IHS Pricing & Purchasing | | The IHS Pricing & Purchasing Service | The IHS Pricing & Purchasing Service enables supply chain cost savings by providing timely, accurate price forecasts and cost analysis. Armed with a better understanding of suppliers' cost structures and market dynamics, organizations can effectively negotiate prices, strategically time buys, and boost the bottom line.

With a database of more than 80,000 historic prices and thousands of price, wage and input cost forecasts, IHS offers more coverage than any other provider in the market. IHS has been providing forecasts of key commodity, labor, and input costs since 1970 -- helping define the purchasing advice industry. | | Learn More |

|

| Commodity Price Forecasts & Supply Chain Cost Benchmarking. Learn More | | |

|

|

|