| Week ending April 13, 2018 |

Trade developments and lackluster Chinese data weigh on commodity prices

|

ANNOUNCEMENT:

This is the final emailed version of the weekly Pricing Pulse Newsletter. Starting April 19, 2018, please visit our ECR blog to view the weekly Pricing Pulse.

Softening demand from China put downward pressure on commodity prices last week.

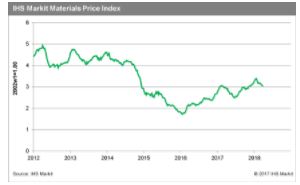

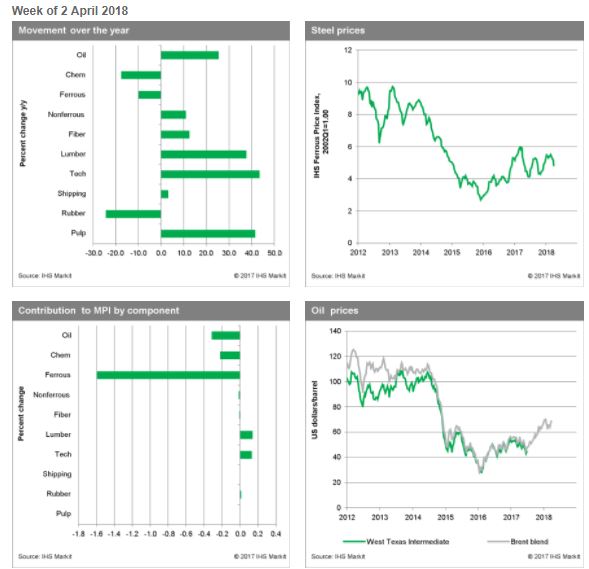

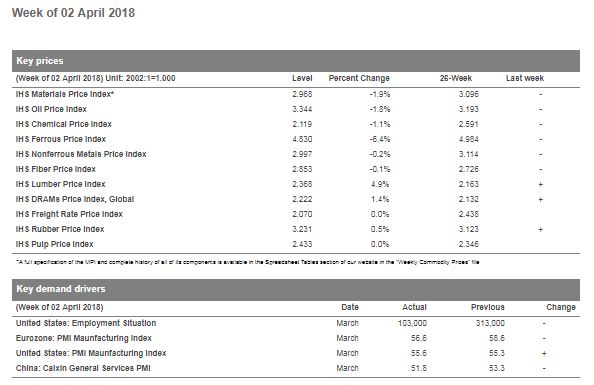

The driver behind the sharp drop in the ferrous index was falling iron ore prices. Iron ore prices took off earlier this year, approaching $80 per metric ton on the expectation of further Chinese stimulus. With the hoped-for stimulus looking less likely, fundamentals are reasserting themselves. Chinese iron ore port stocks are relatively high, while ore shipments to China have begun to slow—both are signs of weaker demand, which is undercutting prices.

Signs of decelerating growth are also beginning to surface in Chinese macroeconomic data. The Caixin General Services PMI fell to 51.8, a decline of 1.5 from February, as new order activity fell. This follows the March Caixin PMI Manufacturing Index that also showed a slowdown in growth. Apart from somewhat disappointing Chinese data, markets are also having to deal with more inflammatory rhetoric and actions on the trade front. Tit-for-tat trade actions by the United States and China and additional US sanctions on Russia have continued to unsettle markets. Even though the March PMI manufacturing numbers in the United States and the Eurozone were solid, this good news was not enough to reassure markets that are growing increasingly nervous about a possible full-blown trade war. Indeed, commodity markets are signaling that trade developments may soon threaten the expansion.

|

|

|

| | IHS Materials Price Index |  |

|

| |

| Market Insight

For an overview of the IHS Materials Price Index, view this video.

Get the Materials Price Index delivered to your in-box weekly.

Subscribe here.

|

|  |

| | |

|

| Industrial Materials: Prices |  |

| Key Prices & Demand Drivers |  |

Construction Labor Costs Reach Highest Level in Almost Three Years, IHS Markit Says

|

Construction costs rose again in November, according to IHS Markit and the Procurement Executives Group (PEG). |

The current headline IHS Markit PEG Engineering and Construction Cost Index registered 60.2, supported by strong figures in both the materials/equipment and labor sub-indexes. The materials/equipment price index was 60.9 in November, moving up from the October figure of 58.9. Price increases were widespread. Current subcontractor labor prices rose at a fast pace in November: the index figure came in at 58.5, the highest reading since December 2014. “Subcontractor rates continued to accelerate over November and expectations for future increases reached a five-year high,” said Emily Crowley, principal economist - pricing and purchasing, IHS Markit. “Tightening labor market conditions combined with an uptick in activity are driving expectations of future rate increases. Currently the U.S. South and West are having the most trouble finding workers leading to stronger wage escalation, whereas the end of major projects in Eastern Canada are keeping pressure off of wages in that region.”

| | Learn More |

|

| About IHS Pricing & Purchasing | | The IHS Pricing & Purchasing Service | The IHS Pricing & Purchasing Service enables supply chain cost savings by providing timely, accurate price forecasts and cost analysis. Armed with a better understanding of suppliers' cost structures and market dynamics, organizations can effectively negotiate prices, strategically time buys, and boost the bottom line.

With a database of more than 80,000 historic prices and thousands of price, wage and input cost forecasts, IHS offers more coverage than any other provider in the market. IHS has been providing forecasts of key commodity, labor, and input costs since 1970 -- helping define the purchasing advice industry. | | Learn More |

|

| Commodity Price Forecasts & Supply Chain Cost Benchmarking. Learn More | | |

|

|

|