Producer price pressures persist in December

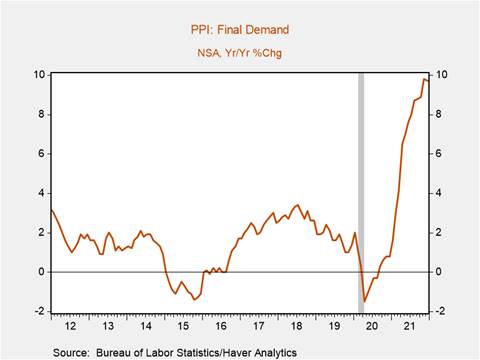

*The U.S. Producer Price Index (PPI) for final demand rose a modest 0.2% m/m in December following an upwardly revised 1% m/m increase in November, but this reflected a temporary decline in energy and food prices. The core measure of the PPI accelerated on a three-month annualized basis, and although the yr/yr increase in the headline PPI declined to 9.7%, it is just 0.1pp below November’s all-time high of 9.8% (Chart 1). In the near term continued supply bottlenecks and mounting labor and input costs are likely to continue to put upward pressure on prices, while the omicron variant and associated surge in COVID-19 cases may further skew inflationary risks to the upside.

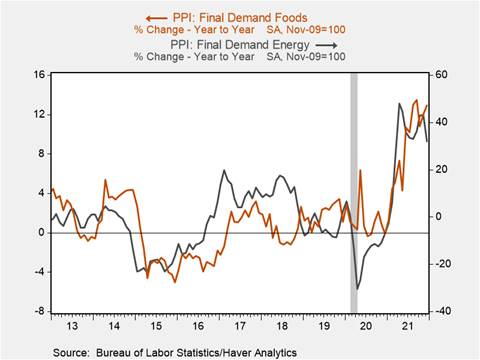

*Declines in food and energy prices weighed down the m/m increase in the headline index, with the PPI for final demand food and final demand energy declining 0.6% m/m and 3.3% m/m respectively. Despite the moderation in December, final demand food and energy prices have increased substantially over the last year rising 12.9% and 31.9% respectively, and recent increases in energy commodity prices are not yet reflected in the PPI (Chart 2).

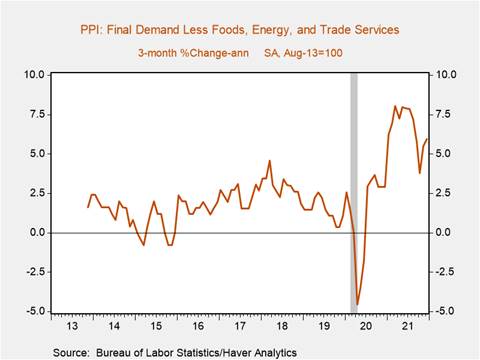

*Core PPI (excluding food, energy, and trade services) which is generally a better gauge of underlying price trends rose 0.4% m/m and 6.9% yr/yr, and has accelerated relative to late 2021, rising 6% on a three-month annualized basis (Chart 3).

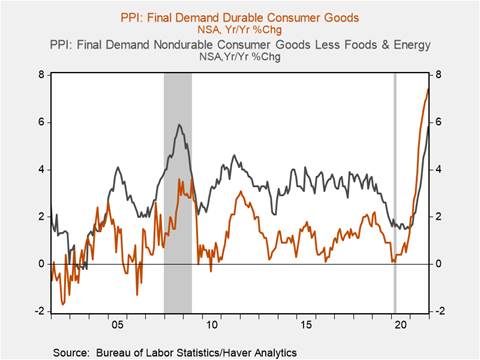

*Durable and nondurable goods (excluding food and energy) prices both rose 0.6% m/m, lifting their yr/yr increases to 7.4% and 5.8% respectively (Chart 4). There are some indications goods inflation is easing: on a three-month annualized basis durable goods prices rose 4.8%, a sharp decline from July’s 11.2%. As supply constraints dissipate and the public health situation improves, the readjustment of demand back towards services through 2022 is likely to lead to a further moderation in goods inflation, particularly for durables.

*The PPI for final demand services rose 0.5% m/m in December on the heels of a 0.9% m/m increase in November, lifting its yr/yr increase to 7.9%. There were notable m/m price increases for final demand transportation and warehousing (+1.7%) and trade services (+0.8%), reflecting strong product demand and supply chain disruptions that have sharply raised distribution costs.

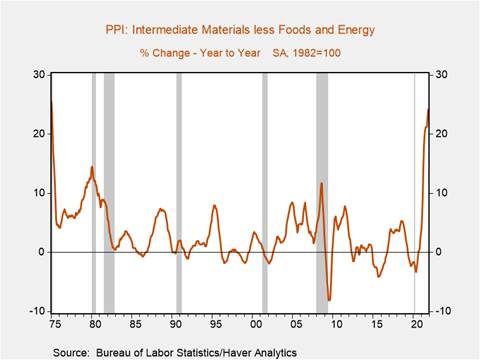

*The price of intermediate inputs (excluding food and energy) rose 0.7% m/m and have increased 26% since February 2020 (Chart 5). Thus far, strong product demand has provided businesses with the flexibility to pass on increased costs to consumers, reflected in the 14% increase in the PPI for final demand over the same period. Anecdotal evidence suggests sustained increases in labor and input costs are increasingly affecting businesses’ inflationary expectations and price setting behavior.

*In the January Beige Book, numerous regional Fed banks reported businesses in their districts were raising prices in response to rising wages and intermediate input costs. For example, FRB Cleveland noted “Firms continue to indicate that they raised prices to offset higher nonlabor input costs and protect margins. Also, contacts more frequently reported that they were factoring in the cost of higher wages in pricing strategies as well”.

Chart 1.

Chart 2.

Chart 3.

Chart 4.

Chart 5.

Mickey Levy, mickey.levy@berenberg-us.com

Mahmoud Abu Ghzalah, mahmoud.abughzalah@berenberg-us.com

© 2022 Berenberg Capital Markets, LLC, Member FINRA and SPIC

Remarks regarding foreign investors. The preparation of this document is subject to regulation by US law. The distribution of this document in other jurisdictions may be restricted by law, and persons, into whose possession this document comes, should inform themselves about, and observe, any such restrictions. United Kingdom This document is meant exclusively for institutional investors and market professionals, but not for private customers. It is not for distribution to or the use of private investors or private customers. Copyright BCM is a wholly owned subsidiary of Joh. Berenberg, Gossler & Co. KG (“Berenberg Bank”). BCM reserves all the rights in this document. No part of the document or its content may be rewritten, copied, photocopied or duplicated in any form by any means or redistributed without the BCM’s prior written consent. Berenberg Bank may distribute this commentary on a third party basis to its customers.