Note: Use ‘Link to PDF’ to view the full array of high-frequency, economic, and financial charts covered in this report

Link to PDF: Real-Time Insights, Economic and Financial Pulse

Real-Time Insights |

Highlights |

· Subway ridership in New York City is less than half its pre-pandemic level, with the seven-day moving average ticking up to ~2.1m. Subway usage remains below the levels attained at the end of 2021, prior to the omicron wave of infections. Could companies use the shift to remote work to offset rising energy and gas prices? |

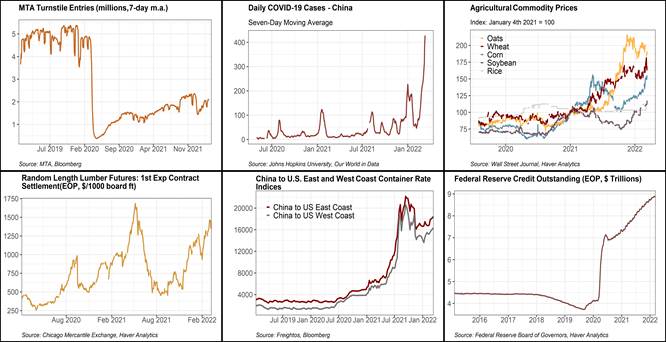

· Daily COVID-19 cases in China have spiked to their highest level since the initial outbreak in Wuhan. China is rigidly sticking to its "zero covid" strategy, and over the weekend imposed lockdowns in the technological and manufacturing hub, Shenzhen, in response to rising infections. Further lockdowns in other cities are possible and will likely exacerbate supply chain disruptions. |

· Agricultural commodity prices have soared in the wake of Russia's invasion of Ukraine and remain elevated despite softening over the last week. Rising food prices will lift headline inflation and may threaten food security across large swathes of the developing world, particularly if the U.S. dollar continues to strengthen. |

· Lumber prices have surged ~27% ytd to just over $1,400/ thousand board ft, reflecting sustained robust demand paired with continued disruptions to Canadian lumber production and distribution. Thus far, builders have been able to pass on increased construction costs to home buyers. |

· Shipping costs from China to the U.S. east and west coasts ticked up and remain well above their pre-pandemic levels, reflecting a mix of concerns over rising energy commodity prices and a spike in COVID-19 infections in China. Elevated shipping costs and the potential for worsening distribution bottlenecks may accentuate upward pressure on goods prices. |

· The Fed's balance sheet has swelled to almost $9 trillion in the wake of the Fed's large scale asset purchase programs conducted over the course of the pandemic. A critical question the Fed will need to address in the near term is the pace and composition of its balance sheet runoff, which, for the most part, will be implemented by capping the reinvestment of maturing assets (treasuries and MBS). There are $870 billion of treasuries on the Fed's balance sheet maturing between April and December 2022. |

Week ahead: Empire Manufacturing, PPI (Mar 15); FOMC March Meeting, Retail Sales (Mar 16); Industrial Production, Housing Starts, Building Permits (Mar 17); Existing Home Sales (Mar 18) |

Link to PDF: Real-Time Insights, Economic and Financial Pulse

Mickey Levy, mickey.levy@berenberg-us.com

Mahmoud Abu Ghzalah, mahmoud.abughzalah@berenberg-us.com

© 2022 Berenberg Capital Markets, LLC, Member FINRA and SPIC

Remarks regarding foreign investors. The preparation of this document is subject to regulation by US law. The distribution of this document in other jurisdictions may be restricted by law, and persons, into whose possession this document comes, should inform themselves about, and observe, any such restrictions. United Kingdom This document is meant exclusively for institutional investors and market professionals, but not for private customers. It is not for distribution to or the use of private investors or private customers. Copyright BCM is a wholly owned subsidiary of Joh. Berenberg, Gossler & Co. KG (“Berenberg Bank”). BCM reserves all the rights in this document. No part of the document or its content may be rewritten, copied, photocopied or duplicated in any form by any means or redistributed without the BCM’s prior written consent. Berenberg Bank may distribute this commentary on a third party basis to its customers.