| |

| Thursday September 14, 2023 |

|

|

| |

|

If there’s one stock that’s got everyone talking, it’s Resmed. |

|

Shares in the Australian-born medical device giant have been pounded since early August, hosed down by the GLP-1 mania. |

|

GLP-1 is being hailed as the weight loss drug to rule them all. Most obstructive sleep apnoea is linked to excess body weight, so drugs that reduce obesity could reduce long-term demand for ResMed’s products. |

|

Short sellers are piling in, seeing Resmed CDI’s short-interest ratio triple since May. But not everyone is running for the hills. In fact, local fundies are buying into the selloff. “I don’t think there’s an Aussie fund manager that’s not buying Resmed,” fund manager Matt Williams told a group of investors earlier this week. “It’s not often you can buy a company of that quality, of that size, that’s 30 per cent off in the space on the month.” |

|

As often happens when shock information comes into focus, investors rush for the exit, fears compounded by analysts issuing downgrades, as UBS did last week. But then the contrarians emerge. It’s not as bad as everyone fears, they say, and at these prices, the stock is a steal. |

|

“We estimate that the current share price implies material uptake and continuation of GLP-1 RA treatment, well ahead of real-world data,” Macquarie researchers said last week, noting that some patients experience “significant weight regain” after coming off the treatment. |

|

Any investor looking to take sides this early in the piece is sticking their neck out, at least until the “Swiss Army Knife” of drugs hits the mainstream. |

|

As Plato long-short fundie David Allen has said of the drug: “Fortunes are going to be made, fortunes are going to be lost, and lives for many individuals will be improved rapidly.” |

|

|

| Emma Rapaport Co-editor, Street Talk |

|

|

|

|

- Macquarie says the Origin takeover price needs to beboosted towards $10 a share, Angela Macdonald-Smith writes.

- Citigroup CEO Jane Fraser admitted in unusually frank terms that the bank was headed in the wrong direction and changes are pending, The New York Times reports.

- D1 Capital Partners’s massive exposure to private bets is weighing on returns, making it one of the year’s worst-performing crossover funds, Bloomberg News reports.

|

|

|

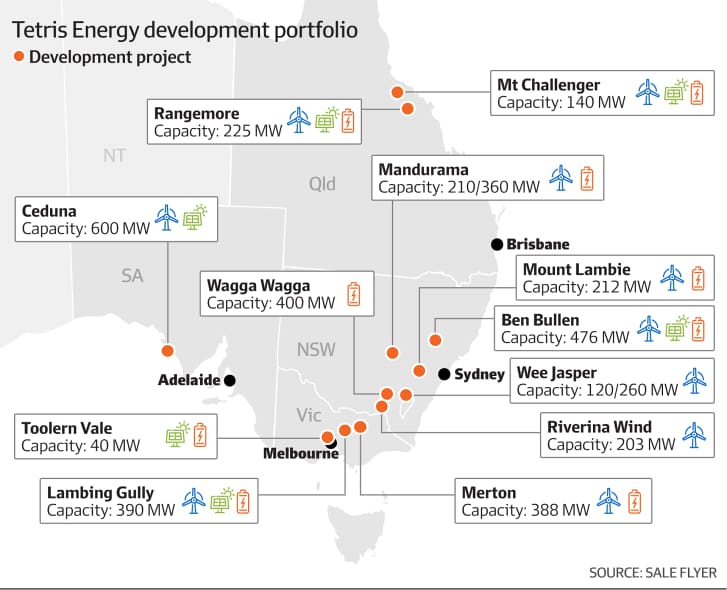

Nearly 70 per cent of the Tetris portfolio is wind projects in National Energy Market regions in NSW and Queensland. About 18 per cent of the portfolio is battery storage; 11 per cent in solar. |

|

|

|

|

|

|

|

| |

|

| |