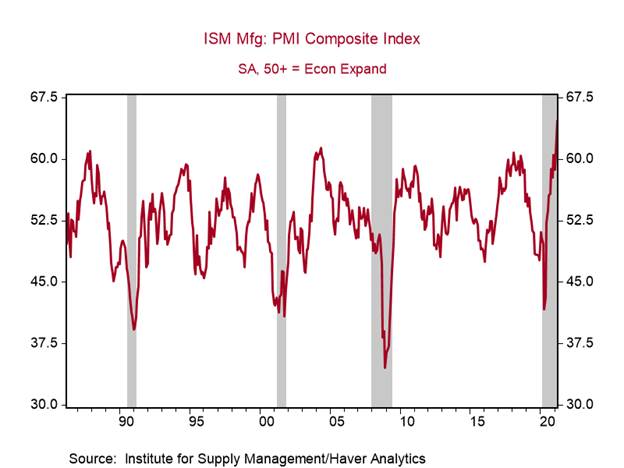

Robust ISM manufacturing survey for March highlights surging production

*The ISM manufacturing survey for March rose to 64.7, the diffusion index’s highest reading since 1983, versus an already strong 60.8, indicating extraordinary strength in virtually all categories and painting a picture of U.S. manufacturers functioning at very high levels, striving to meet strong product demand while dealing with low inventories at the consumer level, production bottlenecks, and higher prices (Chart 1).

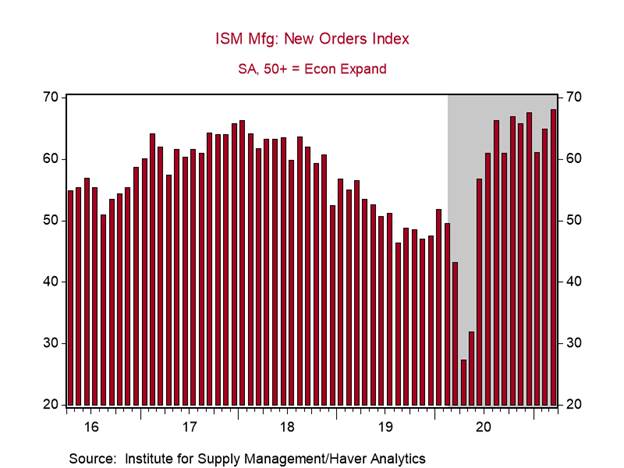

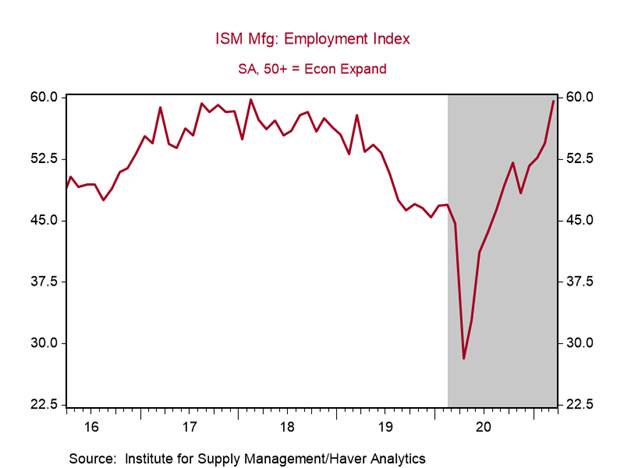

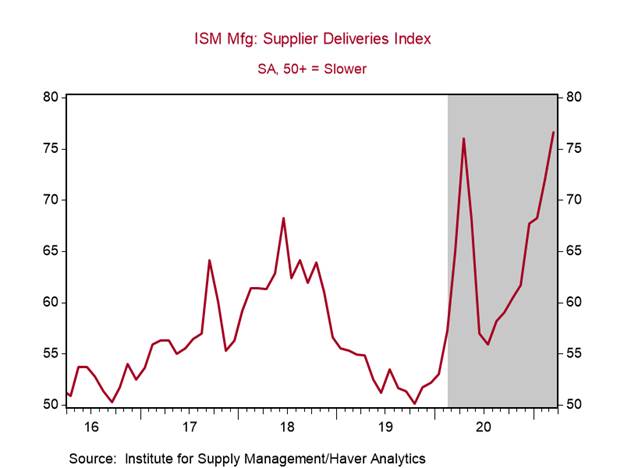

*All five of the ISM manufacturing components—new orders (68.0), production (68.1), employment (59.6), supplier deliveries (76.6), and inventories (50.8, 29.9 for consumer goods)—showed strength (the ISM index weighs each of them equally). These high responses for March follow strong responses in prior months.

*The new orders index of 68.0 is the highest since 2003. Of the manufacturers surveyed, 94.5% responded saying they were experiencing the same or higher new orders, while only 5.5% were experiencing declining new orders, the lowest recording on record (Charts 2-4).

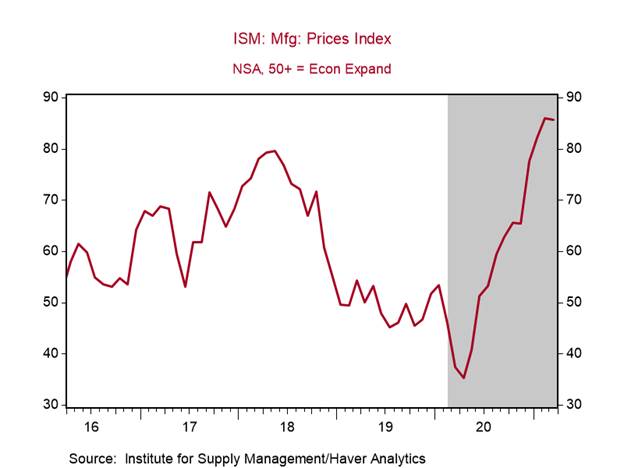

*The prices index in the ISM manufacturing survey remained extraordinarily high, at 85.6 versus 86.0 in February, with 99.5% responding that prices are the same or higher while 0.5% responded that prices were declining (Chart 5).

The ISM manufacturing survey indicates that manufacturers are operating virtually all-out. Despite strong production, rapid increases in demand and a high backlog of orders have extended delivery times to a 47-year high.

Many industries are experiencing shortages of commodities and supplies and disruptions in global supply and distribution chains that are constraining production and resulting in higher prices. Other manufacturers indicate labor shortages.

We are not surprised by this robust ISM survey: it is consistent with the robust gains in consumption and production of goods experienced so far during the recovery, and also in line with our expectation that U.S. economic data is at the early stage of a surge as the economy reopens.

The persistently high index of prices in the ISM survey is consistent with higher costs of production. We anticipate that sustained product demand as the economy reopens will lead more businesses to raise product prices in order to maintain margins, which should result in higher measured inflation.

Chart 1.

Chart 2

Chart 3.

Chart 4.

Chart 5.

Mickey Levy, mickey.levy@berenberg-us.com