| Week ending March 10, 2017 |

Rubber and lumber slump as market exuberance finally begins to crack following strong gains over the last four months

|

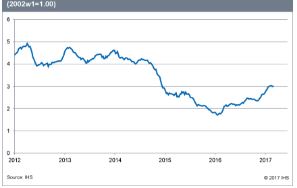

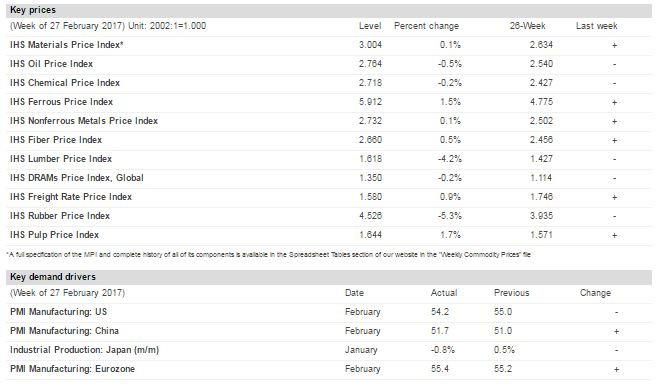

The IHS Materials Price Index (MPI) rose fractionally last week, following the first fall in more than four months the week before. The headline index was up 0.1% as strong falls in rubber and lumber, down 5.3% and 4.2% respectively, were offset by gains in the ferrous and pulp markets.

Rubber markets had been on an exceptional run over the past three months, with supply worries the reason for much of the gains. However, following the announcement that the Thai government, taking advantage of high prices, is to sell off inventory, supply fears have eased with prices slipping. In contrast, ferrous markets gained last week, up 1.5%, as strong demand for steel scrap pushed prices higher following a lull in buying during February.

Last week's macroeconomic releases provided a boost for commodities, with strong data recorded in several regions. In the Eurozone, the February IHS Markit Composite purchasing managers' index (PMI) rose to 56.0, closed in on a six-year high, with confidence in future business activity reaching a new record. US data were also robust, with the February IHS Markit Manufacturing PMI maintaining an expansionary level at 54.2, while the US president reaffirmed his call for a large infrastructure spending package. In China, the Caixin Manufacturing PMI climbed to 51.7 during February, still only slightly above the neutral mark of 50 but an increase from January. The one fly in the ointment was more hawkish comments from the US Federal Reserve (Fed), which clearly put a March interest rate increase on the table. It will be interesting to see how commodity markets react should the Fed indeed raise rates next week. |

| | IHS Materials Price Index |  |

|

| | | Market Insight | | For an overview of the IHS Materials Price Index, view this video. |

|  | | |

|

| Industrial Materials: Prices |  |

| Key Prices & Demand Drivers |  |

| Copper-Based Wire and Cable Prices at Highest Level in Almost Five Years | Construction costs rose again in February, recording the fourth consecutive month of price recovery.

|

The headline IHS PEG Engineering and Construction Cost Index registered 55.2 in February, down from 57.7 in January. Strength was evident for materials markets, though for labor markets, the headline index tipped below the neutral point. The materials/equipment price index came in at 58.0 in February, with the materials sub-index showing rising prices in 10 of the 12 categories tracked. Ocean freight from Europe to the U.S. recorded another month of falling prices and electrical equipment prices were flat. The copper-based wire and cable index experienced the highest escalation compared to January. The last time the copper index registered this level was back in March 2012. "Copper prices are reacting to the closure of two of the world's largest mines: Grasberg in Indonesia, because of a dispute with government over its export permit, and Escondida in Chile, because of a strike,” said John Mothersole, research director at IHS Pricing and Purchasing. “Both events are temporary, though they do tighten the market and support higher prices, at least for a time.”

| | Learn More |

|

| About IHS Pricing & Purchasing | | The IHS Pricing & Purchasing Service | The IHS Pricing & Purchasing Service enables supply chain cost savings by providing timely, accurate price forecasts and cost analysis. Armed with a better understanding of suppliers' cost structures and market dynamics, organizations can effectively negotiate prices, strategically time buys, and boost the bottom line.

With a database of more than 80,000 historic prices and thousands of price, wage and input cost forecasts, IHS offers more coverage than any other provider in the market. IHS has been providing forecasts of key commodity, labor, and input costs since 1970 -- helping define the purchasing advice industry. | | Learn More |

|

| Commodity Price Forecasts & Supply Chain Cost Benchmarking. Learn More | | |

|

|

|