| Seeing Through the Illusion of Last Week’s Gold and Silver Selloff |

Tuesday, 11 June 2024  | | By Brian Chu | | Editor, Gold Stock Pro and The Australian Gold Report |

|

[8 min read] | In this Issue: - How we lost our way with the petrodollar system

- The legacy of zero-interest rate policy

- Creating an economic illusion

- China paused buying gold last month, big deal?

- A perfect storm that’ll blow over fast

- The new credit-based dollar created a credit-based economy.

|

|

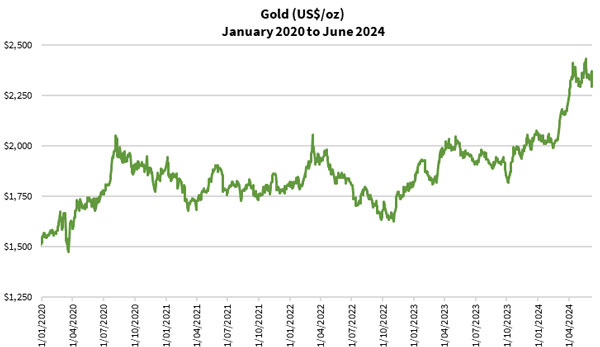

Dear Reader, Did gold and silver’s spectacular run just end last Friday? As Australians headed to bed, gold was still trading well over US$2,350, and silver was over US$31. While we slept, a selling wave took over gold and silver, plunging it by almost 3.5% and almost 7%, respectively. This was quite a move and something we haven’t seen for a while. The last time it fell by more than this amount was on 17th June 2021 when it dropped almost 4.5% from US$1,856 to US$1,773. Gold’s moves in the past four years have been impressive. Since breaching US$2,000 for the first time in August 2020, it traded between US$1,610 to US$2,050 for three years. It suddenly broke out of that range in mid-March this year after the US Federal Reserve announced it could cut rates three times this year. The pace in which gold rallied was nothing short of breathtaking as you can see below:

Meanwhile, silver traded in a similarly tight range until it broke out in March 2024 and breached its 12-year resistance level of US$30 in May:

While precious metals enthusiasts have geared themselves up for what could be a stellar year in 2024, could this latest drop cast a shadow on these hopes? I believe that four major news announcements contributed to gold and silver selling off. The first is the Bank of Canada being the first major economy to cut rates last Wednesday to 4.75%. The European Central Bank moved next the day after, reducing the interest rate to 4.25%. Next was the release of the US non-farm payrolls data that beat consensus estimates. And the fourth was an announcement by the People’s Bank of China that it had paused buying gold last month. In today’s article, we’ll break down these four catalysts and examine to what extent these could affect gold and silver’s levels in the coming months. But first I’ll provide some context to our financial system so you can see why these announcements matter. How we lost our way with the

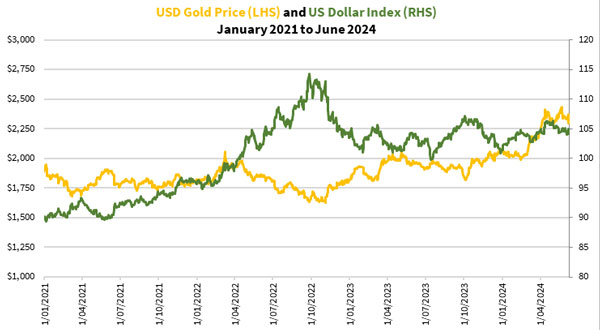

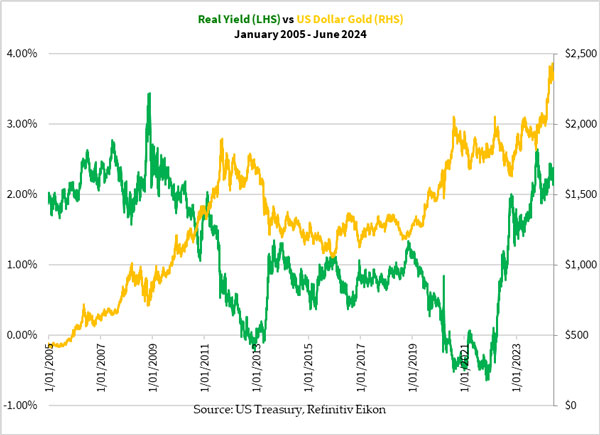

petrodollar system Most of you know I’m a sound monetary system advocate. I also am particularly critical of the petrodollar system that we currently live with. Our system involves central banks, governments, financial institutions and households participating through saving, borrowing and investing. The currencies we use are created artificially by government decree (fiat currency) and borrowed into existence from central banks. It comes with interest attached. Central banks set the interest rate to help regulate the flow of funds in the economy. Since the creation of the US Federal Reserve in December 1913, we have seen a gradual shift from a monetary standard that uses gold as backing to one that relies on the US dollar. As the US government (and other governments for that matter) failed to balance their budgets, they borrow more, causing the currency supply to skyrocket. To date, the US government debt stands at US$34.8 trillion. That doesn’t include household and corporate debt as well as unfunded liabilities for retirement. Including those would amount to over $100 trillion. This number is staggering. And it’s just the US. Imagine what the rest of the world is like. So on one end, you have governments borrowing to fund spending. On the other you have the central banks setting the interest rate to try to regulate economic activity. Theoretically, if governments and central banks are independent of each other, you have some form of checks and balances. Of course it’s not that simple. We’ve seen how government officials appoint people to sit on the central bank boards. Case closed. The legacy of zero-interest rate policy We’ve experienced an economy living on nearly 0% interest rate for much of the last 15 years. It only started rising significantly since mid-2022. Before that, we’ve seen the biggest debt creation ever seen in our history. You can imagine why. Some of you may’ve participated in this too as you borrowed to buy your home and even built your property portfolio. At the same time, the huge increase in the supply of currency led to a period of inflation. Prices of almost everything rose as more currencies flowed around the system. The rising price of gold and silver are just two examples. Creating an economic illusion Now let’s delve into how the rate cuts by the Bank of Canada and the European Central Bank played a big role in causing gold and silver to fall. The proxy for the petrodollar system's health lies in the US dollar's value. It becomes increasingly worthless when the price of everything else rises in US dollar terms. We’ve seen the failure of the Weimar Republic, Zimbabwe and Venezuela as their currencies plummeted. The price of gold is a good proxy indicator. Some of you recall how the price of gold moves in the opposite direction with the US Dollar Index [DXY] and the inflation-adjusted yield of long-dated US Treasury bonds:

The US Dollar Index measures the relative exchange rate of the US dollar against major currencies. The higher the index, the more valuable the US dollar is relative to these currencies. However, it’s a relative measure. Next is the relative interest rates paid by different economies. With Canada and the European Union cutting their interest rates, the US dollar looks more attractive. Debt in US dollars pays a higher return, assuming all these economies have a similar level of inflation. And a higher US Dollar Index placed selling pressure on gold and silver. Next is the non-farm payrolls data release last Friday. The aggregate number of jobs created exceeded consensus estimates. Furthermore, the inflation-adjusted hourly earnings increased modestly. On the surface, it fuelled the narrative that the US economy is moving in the right direction. This gave the US Federal Reserve a pretext to delay cutting interest rates. Of course, delving deeper into the report reveals major issues with the types of jobs created and underemployment. But the narrative stood, and the market responded accordingly. China paused buying gold last month,

big deal? The final kick in the guts of gold and silver came from the People’s Bank of China announcing last Friday that it didn’t buy any gold during May. It had been buying gold in the 18 months before that. The markets took that as another reason to sell precious metals. One of the biggest proponent nations for gold stopped buying gold! Better sell now! But I believe this was a red herring. Just because the People’s Bank of China didn’t officially buy gold, it doesn’t mean the Chinese economy is shunning gold. Far from it. Firstly, gold enters the country through different ways, and it’s unlikely to leave it after. Secondly, there could be other reasons for China pausing the purchase of gold that may strengthen the case for gold. Perhaps the Chinese economy is facing a major demographic problem and a housing debt crisis? Hence, the priority of the PBOC and the government is to spur the economy rather than buy more gold. And those who want to protect themselves from this economic weakness may seek refuge in gold. A perfect storm that’ll blow over fast I hope you can see how these four announcements combined to create a perfect storm for gold and silver to take a dump. The timing of these announcements also seemed coordinated to achieve the effect of dressing up the US dollar and the failing petrodollar system. Delving deeper into each case, you’ll see many holes with which may weaken the narrative. Furthermore, I believe the market will see through this trick, especially the US jobs data. Therefore, this could be a temporary selloff for gold and silver. And don’t be surprised that other central banks will rush to take one for the team to help the US Federal Reserve delay the inevitable rate cut. This appears to be their playbook. Rather than fear the selloff, you might want to consider capitalising on this opportunity to get into precious metals or build your holdings.

Let me help you get started with a comprehensive plan to build a precious metals portfolio with my investment newsletter, The Australian Gold Report. Find out more by clicking here! God bless,

Brian Chu,

Editor, Gold Stock Pro and The Australian Gold Report Brian Chu is one of Australia’s foremost independent authorities on gold and gold stocks, with a unique strategy for valuing big producers and highly speculative explorers. He established a private family fund that only invests in ASX-listed gold mining companies, possibly the only such fund in Australia, putting his strategy and research skills to the test under public scrutiny. He currently writes two gold-focused investment advisories. In his Australian Gold Report, Brian shows you a strategy for building long-term wealth in physical gold, along with a select portfolio of hand-picked stocks, mainly producers with proven revenue streams, chosen for their balance of risk and reward. In his more specialised Gold Stock Pro service, Brian helps readers trade some of the most exciting, speculative gold mining plays on the ASX. He uses his proprietary system — based on the famous Lassonde Curve model, which tracks the life cycle of mining stocks. His aim is to help you get ready to trade the next phase of gold and silver’s anticipated longer-term bull market for opportunities to benefit. Advertisement: JUST RELEASED AND ONLY AVAILABLE FOR A LIMITED TIME: ‘The End of Electric Vehicles’ Greg Canavan reveals why Australia’s EV revolution is doomed to fail… And how it creates a big investment opportunity — if you can see the writing on the wall. Learn more here. |

|

| | By Bill Bonner | | Editor, Fat Tail Daily |

|

[3 min read] Dear Reader, The proposition on the table is provocative. And illuminating. What if we Americans aren’t nearly as rich as we think we are? As outrageous as it seems, ‘fictitious wealth’ appears to explain why the richest country in the world still can’t pay its bills or win its wars.

Simply put... the idea is that America’s fake money — introduced in 1971 — led to an economy with a lot of fake wealth. In short, much of US stock, bond, and real estate wealth... and much of the US economy itself (GDP)… was ‘f’-ed up --…fictitious, fraudulent, or fantasy.

The new credit-based dollar created a credit-based economy... which grew by borrowing money that didn’t exist. Real money must represent goods, services, and real assets. But this new money represented nothing. It was just hollow credit, brought forth by the feds and the banks, and lent out at artificially low rates.

It boosted GDP, stocks, bonds, and real estate... giving us the impression of great wealth... but the flip side of credit is debt... and the US now has almost $100 trillion of it. And as it increases, the interest expense rises too. Now, the US spends more on interest than on the Pentagon — an amount equal to half of the deficit for 2024.

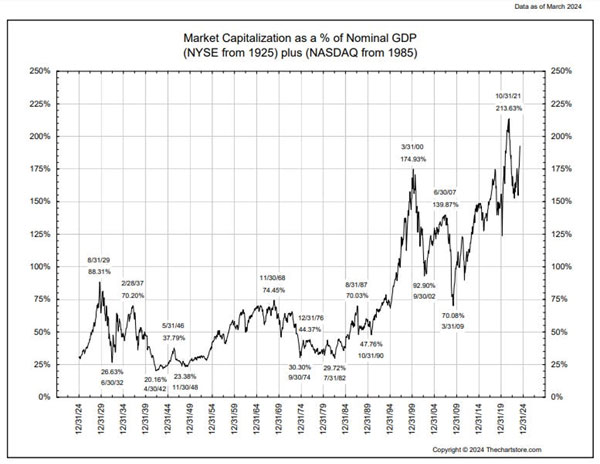

Much of the new credit-money was borrowed by the feds themselves. The part of the economy directly controlled (by spending), or be-muddled (by state, local or federal regulations), by government rose from barely 10% in 1930 to closer to 50% today. Government spending is included in GDP figures... 100% of it. But very little government spending or regulation produces the kind of real wealth you need to pay off past debt and contribute to current prosperity. We’ve seen, too, that much of the wealth in the stock market is an illusion. Using very round numbers to avoid the pretence of precision, the market capitalisation (the total value of all public companies) to GDP ratio for US stocks is historically around 80%.

Today, the measure is closer to 200% (see chart above). And if that traditional relationship between US output and the companies that produced it were restored, about $20 trillion in ‘fictitious’ stock market wealth would have to be stripped from the asset side of the nation’s ledger.

That is just the stock market. If you’ll recall, the bond market topped out in July 2020. The downturn — in which the phony value in bonds is being erased — has been underway for almost four years. Charlie Bilello reports:

‘The US bond market is in a very different place than the stock market. While the S&P 500 has been hitting 25 all-time highs this year, the Bloomberg Aggregate Bond Index remains 11% below its peak from the summer of 2020. At 46 months and counting, this is by far the longest bond bear market in history.’

Adjusting current values to inflation (as measured by gold, not the CPI) we see that the real value of America’s debt has declined by about 75% since 1999 and by nearly 30% since bonds topped out in July 2020.

US bonds are supposed to be the safest credits in the world.

But — again — we see that the ‘face’ value... beef-caked up by trillions in credit money... is very different from the scrawny real value.

But it’s not just Treasury bonds that pretend to have value they don’t actually have. All across the fixed-return world, there are unrecognised losses and make-believe wealth.

We’ll take a look tomorrow...

For now, Tom (our research analyst) thinks the death spiral has begun. More and more borrowing drives up interest rates... making debt payments even harder to keep up with. What follows is a debt crisis, when much of what we thought was wealth is marked down, written off, or inflated away.

We don’t know exactly when, what or how this will play out. But we’re willing to bet that many of our ‘here today’ assets will be ‘gone tomorrow.’

As for what happens to the nation’s political and social life, we leave you to use your imagination. Brookings says a third of the country lives ‘hand to mouth’ already. What happens when the mouth discovers that the hand is empty?

More to come... Regards,

Bill Bonner,

For Fat Tail Daily All advice is general advice and has not taken into account your personal circumstances. Please seek independent financial advice regarding your own situation, or if in doubt about the suitability of an investment. |

|

Advertisement: ‘GOLD FEVER’ The founder of The Australian Gold Fund believes the temperature in the gold market is set to spike in 2024.

Get the details on three gold stocks that could be perfectly positioned to ride the anticipated bull market: CLICK HERE FOR ALL THE DETAILS |

|

|