| | | | Welcome to Deep Dives, where we explore interesting companies in the alt investment space. | Today’s deep dive is on Arta Finance. | Most investments fall into a few broad categories: stocks, bonds, and options. | But structured products are different. These hybrid assets combine properties from distinct categories to create a truly unique risk-reward structure. | Check out the full issue even if you’re not accredited. It’s free, you'll learn a ton |

| |

| | |

|

Today, I'm exploring how you can invest in a slice of the structured products market with Arta Finance. |

Arta does structured products much differently than the big banks. Rather than hawking off-the-shelf products, Arta builds curated assets designed to capitalize on current market conditions. |

And as we’ll see, these offerings cater to a diverse range of investor needs — whether you’re a FIRE enthusiast pursuing high-growth opportunities or a retiree looking for different types of income streams. |

Last year I reviewed Arta — covering their digital wealth platform as a whole. Today, I'm diving deep into their structured products offering. Stick around to learn: |

How structured products can both protect downside and amplify upside potential, How Arta is addressing a huge gap in the market with accessible & tailored products, How Arta is bringing fee transparency to a market riddled with hidden costs, And how you can start assembling your own structured product allocation.

|

Note: This issue is sponsored by our friends at Arta. Arta's offerings are for accredited investors, but even if you're not accredited, read on — you'll learn a ton. As always, we think you'll find this very informative and fair. |

Let's go 👇 |

What is a Structured Product? |

It's best to avoid investing in things you don’t understand. - Warren Buffett |

If you’re unfamiliar with structured products, we can forgive you for being a bit wary. |

Under the surface, however, structured products are probably more familiar than you realize. These assets are built entirely from traditional investments – they’re just combined in a unique way. |

For instance, imagine that you have a $1,000 portfolio that consists of: |

A $900 zero-coupon bond with a face value of $1,000 and one year to maturity. And a $100 call option tied to the performance of the S&P 500.

|

As long as the bond doesn’t default, this portfolio will always be worth at least $1,000 in a year, even if the option ends up worthless. Since the portfolio was originally worth $1,000, our principal is protected. |

But if the S&P 500 booms, our option might be worth lots of money — so we have the potential to participate in stock market gains. |

In effect, we’ve just manufactured a type of structured product known as a principal-protected equity-linked note. We did this using nothing more than a few basic financial instruments that you may already be familiar with. |

| The process of creating a structured product is not unlike cooking. By combining ingredients in just the right manner, you can create something more valuable than the sum of its parts. Image: Monika Grabkowska |

|

Once you understand the power of combining financial assets like this, the sky is the limit. Start mixing in things like stocks, puts, and futures, and the types of payoffs you can manufacture are literally endless. |

That’s the what of structured products – but what about the why? Who are these investments good for, and what benefits can they offer? |

Structured products: Risks & rewards |

There are huge benefits... |

The main benefit of structured products is allowing investors to target specific investment outcomes tied to their unique preferences. |

That’s a mouthful, but the logic is intuitive: if you have unique goals, then you’ll need unique assets to achieve them. |

Some investors have simple goals, like wanting broad exposure to the US equities market. For investors like this, vanilla products may work just fine. |

But other investors have more sophisticated preferences, such as: |

Capping downside losses at a specific percentage to minimize risk, Generating a fixed yield in certain cases and a variable return in others, Amplifying returns to boost portfolio performance.

|

Goals like these are where structured products shine, allowing investors to access unique payoffs tailored to their preferences. |

| The value proposition of structured products is sort of like a customized workout plan. If you just want to get in better shape, a basic routine is fine - but a tailored plan can target specific goals. Image: Victor Freitas |

|

But there are also some risks... |

As non-traditional assets, structured products also come with non-traditional sources of risk. |

Liquidity risk is the biggest and most obvious one. Structured products typically have a fixed maturity anywhere from six months to several years. While it’s generally possible to liquidate your position beforehand, it’s not always ideal. |

But there are also other, less obvious risks involved |

Credit risk |

Since structured products are technically debt issued by a financial institution, they come with credit risk tied to the issuer, just like a bond. While it’s unlikely that a major investment bank would default on its obligations, it is possible. |

Call risk |

Some structured products can be “called away” early if specific conditions are met. This results in call risk, which occurs if you have to redeploy capital earlier than anticipated. |

The Structured Product Market |

While structured products are less well-known than other investments, this market is growing rapidly. |

In the US, issuance of new structured products already exceeds $100 billion per year. For comparison, US IPOs raised about $40 billion in 2024. |

And these assets are even more popular worldwide. All told, the global structured products market is estimated at about $3 trillion. |

| While the US structured product market is growing, it still lags other regions. Financial centers like Hong Kong have made structured products an $800 billion market in Asia. Image: Diego Delso |

|

Not all structured products are created equal, however. |

In the US, the market is largely bifurcated into two distinct categories — calendar products and custom products. |

While structured products are enormously useful in theory, both of these categories come with significant drawbacks in practice. |

Calendar Products |

Calendars are off-the-shelf structured products issued by banks on a pre-set schedule, typically monthly (hence the name). Although buyers can give feedback on the products they want to see, banks ultimately decide what to issue. |

Calendars are more widely available and typically have minimums of around $1,000. However, they’re designed based on what the bank wants to sell, not what investors want to buy. |

Custom Products |

Customs, meanwhile, are truly custom structured products. These assets are manufactured by banks based on requests from ultra-high-net-worth investors and their advisors. |

Customs allow you to tailor exposure to exactly what you want – but they’re far more expensive. Explicit fees of more than 1% annually (plus potential hidden costs) and minimums exceeding $500K are common. |

Historically, there’s been a big gap in the market. What’s missing is buyer-focused, low-cost, and accessible structured products. |

And it’s exactly this gap that Arta Finance is trying to address with their own structured product offerings. |

How Arta Does Structured Products |

We discussed Arta Finance last year in a deep dive covering the company as a whole. |

(Psst — check out that article for a deeper discussion of Arta’s capabilities, including blue-chip private markets investing, direct indexing, and estate & investment advisory services.) |

But in a nutshell, Arta is a digital private wealth service focused on dramatically expanding access to the types of sophisticated financial tools previously reserved for the ultra-wealthy. |

|

Today, I'm going to focus on their structured products offerings, which are uniquely designed to solve the problems plaguing the existing market. |

What sets Arta’s structured products apart? |

There are three main advantages setting Arta’s structured products apart from the rest of the market: |

|

Read the full issue at Alts.co |

Expertly crafted for the current environment |

Arta’s team of market experts and traders constantly survey the market, generating ideas for structured products that can add value to investor portfolios. |

Typically, the team executes one or two of their very best ideas each month. |

This team is made up of people who have traded tens of billions of dollars of these assets at banks like Morgan Stanley and JPMorgan. |

Take it from me, I've spoken with them. They're absolute experts on this stuff and they’ve seen how the sausage is made. |

Now, they can use that knowledge on behalf of Arta users. This expertise is a strong contrast with other providers, who are populated by derivatives salespeople who only think they know what they’re doing. |

Competitive fees |

Arta takes the team’s best ideas and works with major banks to build them into products. By conducting an auction between major banks (typically about a dozen), Arta is able to secure ultra-competitive terms and low fees. |

Arta charges a transparent 0.50% annual fee on their products. That’s less than half of the 1%+ industry standard (plus whatever hidden fees advisors tack on). |

This fee structure also ensures that Arta’s team doesn’t have the same perverse incentives as banks, where salespeople are often motivated to offset whatever trades the bank happens to be on the wrong side of. |

Highly accessible |

Arta’s products have a minimum investment of just $25k and are accessible on a rolling basis through their platform. |

Like calendars, this process allows Arta to capture economies of scale to make structured products more widely available. |

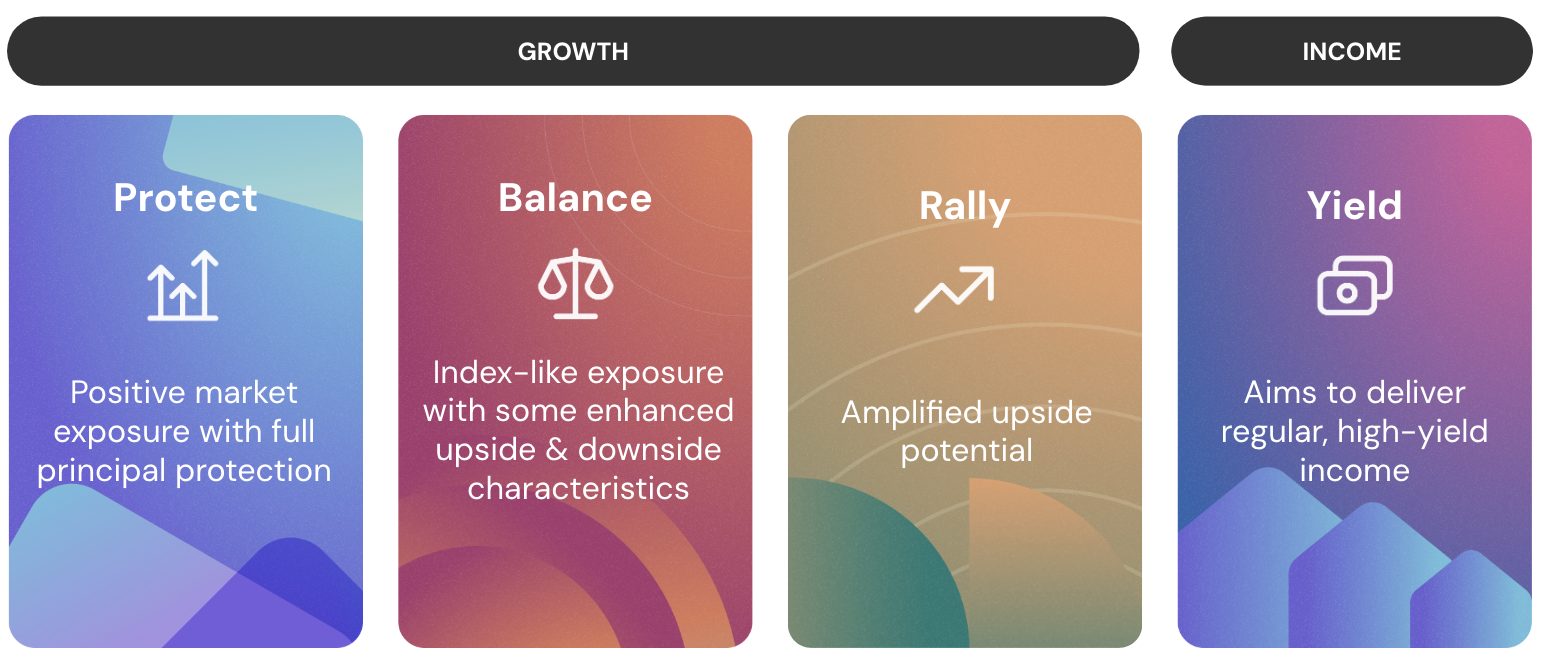

Arta’s four product configurations |

Arta’s team of experts build products that fall into one of four distinct categories: Protect, Balance, Rally, and Yield. |

|

Each individual product is unique, but these names help group products that are trying to achieve similar goals: |

Protect products are built to provide principal protection while also participating in equity gains. These are similar to the structured product we constructed in the first section. Balance seeks to blend different traits to capture unique risk/reward structures. Balance June 2024, for instance, had 10% loss protection on the S&P 500 while magnifying upside gains. Yield products aim to generate high income, often tied to the performance of assets not generally associated with yield plays. Yield November 2024, for instance, offered a fixed 29.60% annual yield based on the performance of Tesla and Palantir. Finally, Rally products are designed to amplify upside potential—like a leveraged ETF but without some of the downsides like volatility decay.

|

To dig into Arta’s offerings, we’ll explore a recently closed Rally product as a case study. |

|

Investing in Structured Products with Arta |

Interested in investing in structured products through Arta? The platform is now open to accredited investors worldwide – Arta launched globally last year, meaning they can now serve investors beyond the US. |

What’s more, new users can get fees waived on their first $100K (subject to some terms & conditions). Here are some of the finer details of investing in their US structured products offering: |

Minimum investment: $25k Accreditation: Accredited investors only Fees: Flat 0.5% annual fee with no hidden costs Custody: Held in the investor’s name at BNY Pershing, one of the largest custody banks in the world Issuing partners: Major investment-grade banks like UBS and Morgan Stanley

|

You can sign up today to see Arta’s latest products. |

And don’t forget to explore all the other offerings that make Arta a full-service wealth platform, including investment advisory, private markets, and wealth-building through sophisticated life insurance strategies (a topic we’ll have much more to say about soon – stay tuned). |

|

That's it for today. |

Join the discussion in the Alts community |

See you next time, Brian |

Disclosures from Alts |

This issue was sponsored by Arta Finance Neither the author, nor Altea holds any interest in Arta offerings

|

Disclosures from Arta |

This article is sponsored by Arta Finance Wealth Management LLC. Alts.co is not a client of Arta and has been provided cash compensation for the endorsement. The opinions expressed are based on the author's knowledge of Arta's services and are not indicative of future results. This article is for informational purposes only and should not be considered investment advice or a recommendation to buy or sell any particular security. |

|