Surge in U.S. job gains indicates economy is reopening

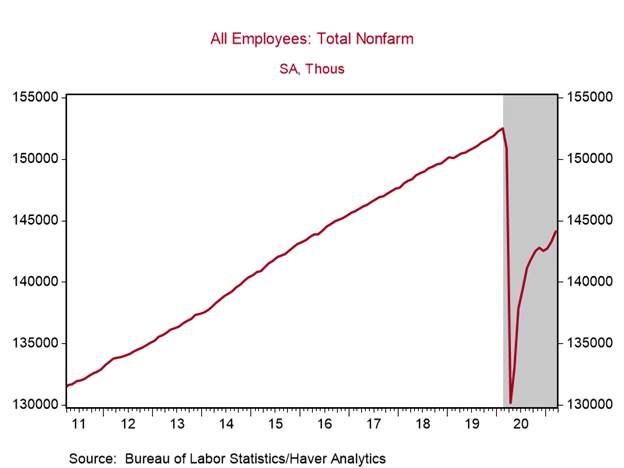

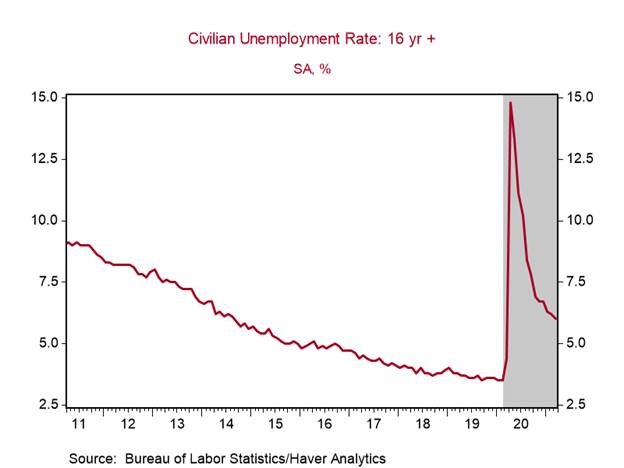

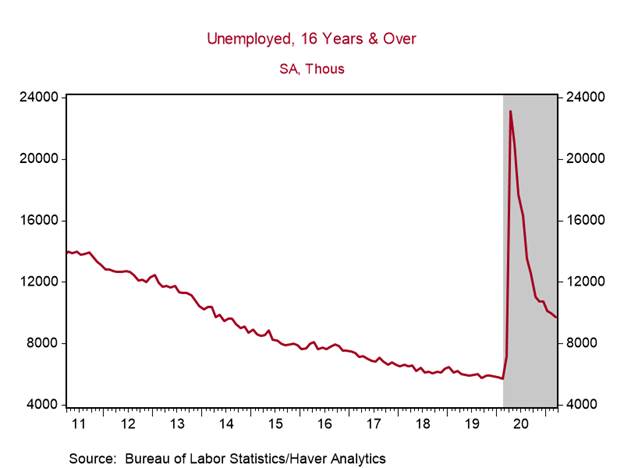

*Establishment payrolls surged 917,000 in March and February job gains were revised up 89k to 468,000, while the number of unemployed fell 262k and the unemployment rate receded to 6.0% from 6.2% (Charts 1-3). Although the gains still leave payrolls 8.4 million below their pre-pandemic level, the breadth and magnitude of the improvement in the Employment Report highlight the strong effects of the reopening of the economy and point to substantial gains in the coming months.

*The increase in jobs was widespread. There were gains of 110k in construction and 53k in manufacturing that lifted employment in the goods producing sectors, and gains of 597k in the service-producing sectors (following an upwardly revised gain of 602k in February), with net new jobs of 297k in leisure and hospitality, 101k in education and healthcare, and 48k in transportation and warehousing.

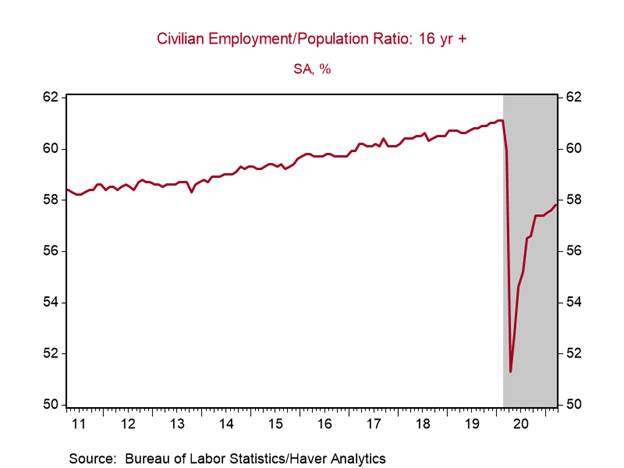

*The unemployment rate reflected a decline in the number of unemployed of 262k and an increase of 347k in the measured labor force. This resulted in a tick-up in the labor force participation rate to 61.5 and a rise in the employment-to-population ratio to 57.8 from 57.6. These figures show clear improvement but remain well below pre-pandemic levels (Chart 4).

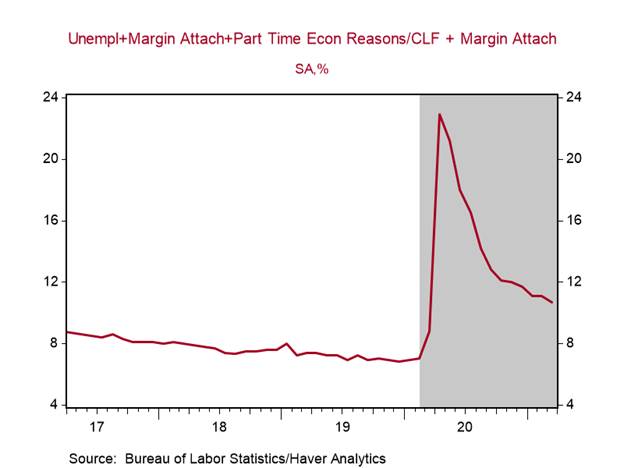

*The unemployment rate of prime age workers (age 25-54) fell to 5.5% from 5.7%. Alternative measures of unemployment also registered gains. U-6, a broad measure of total unemployed plus all marginally attached workers plus part-time workers for economic reasons, fell to 10.7% from 11.1% (Chart 5).

*Average hourly earnings continue to be skewed by the rapid changes in the composition of workers, but it is noteworthy that average hourly wages in the leisure and hospitality sectors rose 1.5% in March following a 1% increase in February, lifting the yr/yr increase to 4.6%, even though employment in those sectors is 3.1 million below their pre-pandemic level.

The robust Employment Report for March is consistent with other data showing a decided strengthening in economic activity. As the economy reopens in coming months, labor markets are expected to improve substantially further in both the goods producing and service producing sectors. This would fuel gains in wages and salaries, supporting increases in disposable income and consumer purchasing power.

Chart 1.

Chart 2.

Chart 3.

Chart 4.

Chart 5.

Mickey Levy, mickey.levy@berenberg-us.com