| -- | November 8, 2018 Mutual Funds vs. ETFs  My name is Jared Dillian, I used to be a big deal in the ETF industry. And I’m here to tell you to that I like open-end mutual funds better than ETFs—mostly because ETFs are misused. Slow down, Turbo. What’s this all about? I am not mad at ETFs or anything. On ETFs, I actually agree with Jack Bogle. He never wanted Vanguard to issue them, because they encouraged short-term trading rather than long-term investing. He is right! It’s because of a subtle difference in the structure. With a mutual fund, you mail them a check (or the electronic equivalent) and you buy shares of that particular investment company at the net asset value, determined once daily. You can’t watch it during the day—it doesn’t do anything. Sure, you can guesstimate where they will end up at the end of the day based on market action, but that isn’t very productive. In the old days, you would look at your mutual funds in the newspaper (really), once every couple of weeks or so. That is how it is supposed to be done. An ETF, you can watch… second by second, tick by tick. I don’t care what kind of market psychology ninja you think you are—when you see something trading tick by tick, it’s a lot different than something that prints once at the end of the day. If it starts to go down, you might feel compelled to sell it, which pretty much goes against anything and everything a financial advisor will tell you. Leave it alone, and let it compound. It’s what we do at ETF 20/20. But if you’re going it alone, it’s not so easy when you can pull it up on your Robinhood app and stare at it. Some people think of ETFs as short-term money, and mutual funds as long-term money. That’s a dumb way of looking at it, because both should be thought of as long-term money. I am the psychology guy. My core belief is that investor psychology drives the majority of returns. If you think about it, an active ETF should roughly equal an active mutual fund, and a passive ETF should roughly equal a passive mutual fund. But because they’re structured very differently, investors treat them very differently—all because of psychology. For better or worse, people typically use ETFs for speculation, partly because ETF issuers encourage speculation. Blockchain, cannabis, double-inverse leveraged volatility, etc. The mutual fund industry is still pretty boring. And that is a good thing. Implicit in the ETF vs. mutual fund debate is the active vs. passive debate, because most mutual funds are active and most ETFs are passive. | | | | - | | FREEDOM PAYS Your no-fee IRA from a bank, broker, or mutual fund may be convenient... But it’s a no-freedom IRA. It blocks you from the higher profits and faster growth possible when you have full control over your IRA investments. It’s not hard to gain that control and start piling up the rapid tax-free returns you want for your IRA. Learn How » |

| - |

|

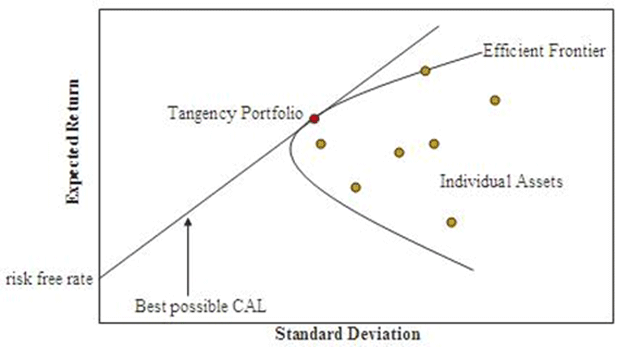

Pick Bad Mutual Funds First of all, I’m a big proponent of active management. Active management has the potential to deliver good returns while minimizing volatility. Remember, if you invest in an index, you get the volatility of an index. But there’s actually more to it than that. Hardcore finance people will be familiar with the term “efficient frontier.” It is the set of portfolios that deliver the highest level of returns for a defined level of risk. In the old days, this used to be an academic concept. But with the addition of some brainpower and some computational power, it is not hard to get yourself a portfolio on the efficient frontier. In fact, one of the big brokerage houses will do it for you.

Source: Wikipedia Funny thing about everyone getting portfolios on the efficient frontier. The trade tends to get a bit crowded. Finance is a non-ergodic system, which means roughly that people’s individual behavior has an effect on the overall environment. Lots of people individually choosing a portfolio on the efficient frontier has the potential to create a system that is unstable and subject to, well, getting flushed. In a situation like this, it might be better to pick an objectively bad portfolio than a popular portfolio. By bad, we mean: something with worse risk/return characteristics. Something off the efficient frontier. By picking a bad mutual fund, you will exhibit lower correlation with other funds and the rest of the market. I bet you never had someone tell you to pick bad mutual funds. I’m being serious, go to Morningstar and look at the one, two, and three star funds. Besides, Morningstar’s track record on predicting which funds will outperform isn’t so great. It’s mainly a marketing tool. Manager Risk There is one important thing to know about actively-managed funds: the portfolio manager matters. There is serial correlation. Someone who is doing a good job will likely continue to do a good job. Someone who is doing a bad job will likely continue to do a bad job. Unless the market environment changes dramatically, at which point good managers become bad managers and bad managers become good managers. I can’t seem to find the article right now, but I seem to remember the Wall Street Journal writing about a mutual fund firm during the financial crisis. The firm, which some had considered to have the worst mutual funds, suddenly had the best mutual funds. The funds were mostly invested in banged-up small cap tech companies, which suddenly went into favor while everything else was getting s---housed. This is why it is not such a good idea to chase good performance and good managers. Financial security usually comes from doing the opposite of what everyone else is doing, but you’ve probably heard that from me before. Don’t Worry, New ETF 20/20 Subscribers Every criticism I’ve made here of ETFs is really more about investor behavior around ETFs. As I said, I’m not mad at ETFs, so to the hundreds of you who have joined ETF 20/20 in the last couple of weeks… you made a great decision. We invest in ETFs in an intelligent, long-term fashion. No double-inverse leveraged volatility in sight. (If you didn’t join, you still can—you’ll pay full price, but it’s still inexpensive for what you get.) Now, you might remember that a few weeks ago, I said here that I was working on some big changes. All of these changes are now in place. The philosophical question I wanted to answer was: “If ETF 20/20 offers what every investor needs—a balanced, core portfolio—how can I give readers more of what they want?” As we all know, what you need and what you want are often very different things. I’ve been working on this question for months, and I’m happy to say that I now I have the answer(s). I’ll be telling you much more about it tomorrow—please watch out for an email from me.

Jared Dillian

Editor, The 10th Man

ETF 20/20: Your solution for intelligent ETF investing. Jared’s introductory service, helps investors use ETFs to make more money in the markets with less volatility. ETF 20/20 is a newsletter for every investor—order your subscription now | | Other publications by Jared Dillian: Street Freak: Jared’s monthly newsletter for self-directed stock pickers. Learn how to pick and trade trends, and master your inner instincts here. The Daily Dirtnap: Want to read Jared every day of the week? Hear his daily thoughts on the markets, investor sentiment, central banks, and a dose of dark wit. Thousands of sophisticated investors, Wall Street traders, and market participants read Jared’s premier service, The Daily Dirtnap. Get it here. |

Share Your Thoughts on This Article

Was this email forwarded to you?

Click here to get your own free subscription to The 10th Man.

Use of this content, the Mauldin Economics website, and related sites and applications is provided under the Mauldin Economics Terms & Conditions of Use. Unauthorized Disclosure Prohibited The information provided in this publication is private, privileged, and confidential information, licensed for your sole individual use as a subscriber. Mauldin Economics reserves all rights to the content of this publication and related materials. Forwarding, copying, disseminating, or distributing this report in whole or in part, including substantial quotation of any portion the publication or any release of specific investment recommendations, is strictly prohibited.

Participation in such activity is grounds for immediate termination of all subscriptions of registered subscribers deemed to be involved at Mauldin Economics’ sole discretion, may violate the copyright laws of the United States, and may subject the violator to legal prosecution. Mauldin Economics reserves the right to monitor the use of this publication without disclosure by any electronic means it deems necessary and may change those means without notice at any time. If you have received this publication and are not the intended subscriber, please contact service@mauldineconomics.com. Disclaimers The Mauldin Economics website, Thoughts from the Frontline, The Weekly Profit, The 10th Man, Connecting the Dots, Transformational Technology Digest, Over My Shoulder, Yield Shark, Transformational Technology Alert, Rational Bear, Street Freak, ETF 20/20, In the Money, and Mauldin Economics VIP are published by Mauldin Economics, LLC Information contained in such publications is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The information contained in such publications is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. The information in such publications may become outdated and there is no obligation to update any such information. You are advised to discuss with your financial advisers your investment options and whether any investment is suitable for your specific needs prior to making any investments.

John Mauldin, Mauldin Economics, LLC and other entities in which he has an interest, employees, officers, family, and associates may from time to time have positions in the securities or commodities covered in these publications or web site. Corporate policies are in effect that attempt to avoid potential conflicts of interest and resolve conflicts of interest that do arise in a timely fashion.

Mauldin Economics, LLC reserves the right to cancel any subscription at any time, and if it does so it will promptly refund to the subscriber the amount of the subscription payment previously received relating to the remaining subscription period. Cancellation of a subscription may result from any unauthorized use or reproduction or rebroadcast of any Mauldin Economics publication or website, any infringement or misappropriation of Mauldin Economics, LLC’s proprietary rights, or any other reason determined in the sole discretion of Mauldin Economics, LLC. Affiliate Notice Mauldin Economics has affiliate agreements in place that may include fee sharing. If you have a website or newsletter and would like to be considered for inclusion in the Mauldin Economics affiliate program, please go to http://affiliates.ggcpublishing.com/. Likewise, from time to time Mauldin Economics may engage in affiliate programs offered by other companies, though corporate policy firmly dictates that such agreements will have no influence on any product or service recommendations, nor alter the pricing that would otherwise be available in absence of such an agreement. As always, it is important that you do your own due diligence before transacting any business with any firm, for any product or service. © Copyright 2018 Mauldin Economics | -- |