The Dillian Loop I’ve always wanted a cognitive bias named after me. There is probably already a name for this, but it’s hard to search for these things on Google. So let’s take Japan, for example. Japan does quantitative easing. -

If it works, it is declared a success and they do more. -

If it doesn’t work, it means they need to do more.

Japan has done a lot of quantitative easing. I’ll give you another one. Dodd-Frank was really meant to prevent bond traders from earning a million dollars. It has been successful, but as an unintended consequence, it has reduced liquidity. Now the SEC is regulating mutual funds even more to address the liquidity problems. -

If the regulations work, they are declared a success and they write more regulations. -

If they don’t work, it means they need to have more regulations.

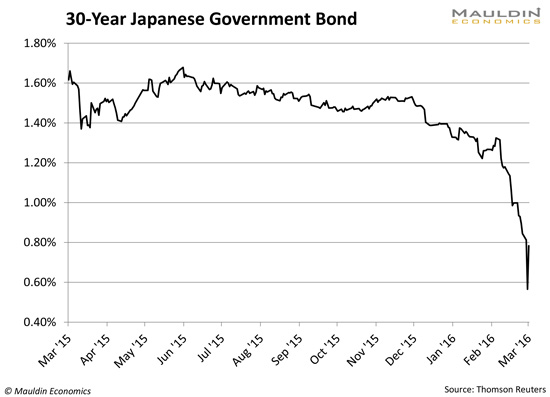

You find many examples of these negative feedback loops in today’s markets. Policymakers will keep doing the same dumb stuff even though it makes the problem worse. It is like they are stuck in some recursive do-loop in Applesoft Basic. I will call this The Dillian Loop. Why This Happens There are a couple of reasons why this happens. The biggest is that policymakers hate losing face more than anything. They are unwilling to admit that a course of action is bad, so they will keep slamming on the square peg to get it in the round hole over and over again until the hammer breaks. There are countless more examples. Raising taxes raises progressively less revenue, so consequently, you raise taxes even more. You keep doing what doesn’t work, even if it doesn’t work. This is allegedly an Einstein quote: “The definition of insanity is doing the same thing over and over again and expecting a different result.” The problem is, there are no controlled experiments in finance. Japan will never know how things would have worked out without Abenomics. Publicly, they will say it would have been worse. But there is no way to know! After all, see how Depression-era history is taught in the United States. The New Deal saved the world. What if we didn’t have the New Deal? Maybe things would have been better? After all, the crash happened in 1929 and the economy didn’t recover until 1946. Warren Harding’s response to the (very severe) recession of 1921 was to do nothing, and the economy recovered in less than two years. Interventionism is always praised after the fact. Nobody ever says doing nothing did something. So the second aspect of this is that policymakers need to be seen doing something. They can’t be seen doing nothing, because that would mean they are not doing their job, even if their job might be staying out of the way. The concept of laissez-faire seems pretty quaint nowadays. Japan is dealing with some pretty serious consequences of its interventionism. JGB yields dropped 25 basis points in a day, flattening the yield curve and rendering the banks possibly insolvent (and then went back up 24 hours later).  The Dillian Loop is really just an elaborate argument for laissez-faire, the idea that constant interventionism in a complex system yields results that are highly unpredictable and often deleterious. In this writer’s opinion, the best possible response to the housing crash, the financial crisis, the Great Recession, would have been to do—nothing. Liquidity Gone, Never to Return Back when I was trading 10 years ago, liquidity was abundant. You could sell infinite amounts of stuff without having any impact at all. Bond desks nowadays are reduced to trading odd lots and sitting around the rest of the time, while compliance reads their email. You can regulate the markets a million different ways, but the last thing you want to do is screw with liquidity (a financial transactions tax would reduce what’s left of the capital markets to rubble). The government doesn’t realize that it alone is responsible for the liquidity problems and that additional regulation will only serve to reduce liquidity even more. I wouldn’t be surprised if 40 Act high yield mutual funds disappeared in a few years, which by the way, would mean a higher cost of capital for everyone. That can’t possibly have any negative economic consequences. But since we are caught in the Dillian Loop, what is the chance that we will get out of it? I’d say very slim. I’d say we could easily spend another 10-20 years in the Dillian Loop. The only thing that gets you out of the Dillian Loop is when you reach rock bottom, the point of maximum pain, and people are so disgusted with years of ineptitude that they are willing to try something different. They might even get so desperate, they will try capitalism.

Jared Dillian

Editor, The 10th Man

Jared's premium investment service, Street Freak, is available now. Click here for our introductory offer. Jared Dillian, former head of ETF Trading at one of the biggest Wall Street firms and author of the highly acclaimed book, Street Freak: Money and Madness at Lehman Brothers, shows you how to pick and trade trends, and master your inner instincts. Learn how to use “Angry Analytics” as a leading indicator of budding trends you can profit from… and how to view any market situation through the lens of a trader. Jared’s keen insight into market psychology combined with an edgy, provocative voice make Street Freak an investment advisory like no oth er. Follow Jared on Twitter at @dailydirtnap. Share this newsletter

http://www.mauldineconomics.com/members

Use of this content, the Mauldin Economics website, and related sites and applications is provided under the Mauldin Economics Terms & Conditions of Use. Unauthorized Disclosure Prohibited The information provided in this publication is private, privileged, and confidential information, licensed for your sole individual use as a subscriber. Mauldin Economics reserves all rights to the content of this publication and related materials. Forwarding, copying, disseminating, or distributing this report in whole or in part, including substantial quotation of any portion the publication or any release of specific investment recommendations, is strictly prohibited. Participation in such activity is grounds for immediate termination of all subscriptions of registered subscribers deemed to be involved at Mauldin Economics’ sole discretion, may violate the copyright laws of the United States, and may subject the violator to legal prosecution. Mauldin Economics reserves the right to monitor the use of this publication without disclosure by any electronic means it deems necessary and may change those means without notice at any time. If you have received this publication and are not the intended subscriber, please contact service@mauldineconomics.com. Disclaimers The Mauldin Economics web site, Yield Shark, Thoughts from the Frontline, Tony Sagami's Rational Bear, Stray Reflections, Outside the Box, Over My Shoulder, World Money Analyst, Street Freak, Just One Trade, Transformational Technology Alert, and Conversations are published by Mauldin Economics, LLC. Information contained in such publications is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The information contained in such publications is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. The information in such publications may become outdated and there is no obligation to update any such information. John Mauldin, Mauldin Economics, LLC and other entities in which he has an interest, employees, officers, family, and associates may from time to time have positions in the securities or commodities covered in these publications or web site. Corporate policies are in effect that attempt to avoid potential conflicts of interest and resolve conflicts of interest that do arise in a timely fashion. Mauldin Economics, LLC reserves the right to cancel any subscription at any time, and if it does so it will promptly refund to the subscriber the amount of the subscription payment previously received relating to the remaining subscription period. Cancellation of a subscription may result from any unauthorized use or reproduction or rebroadcast of any Mauldin Economics publication or website, any infringement or misappropriation of Mauldin Economics, LLC’s proprietary rights, or any other reason determined in the sole discretion of Mauldin Economics, LLC. Affiliate Notice Mauldin Economics has affiliate agreements in place that may include fee sharing. If you have a website or newsletter and would like to be considered for inclusion in the Mauldin Economics affiliate program, please go to http://affiliates.pubrm.net/signup/me. Likewise, from time to time Mauldin Economics may engage in affiliate programs offered by other companies, though corporate policy firmly dictates that such agreements will have no influence on any product or service recommendations, nor alter the pricing that would otherwise be available in absence of such an agreement. As always, it is important that you do your own due diligence before transacting any business with any firm, for any product or service. © Copyright 2016 Mauldin Economics |