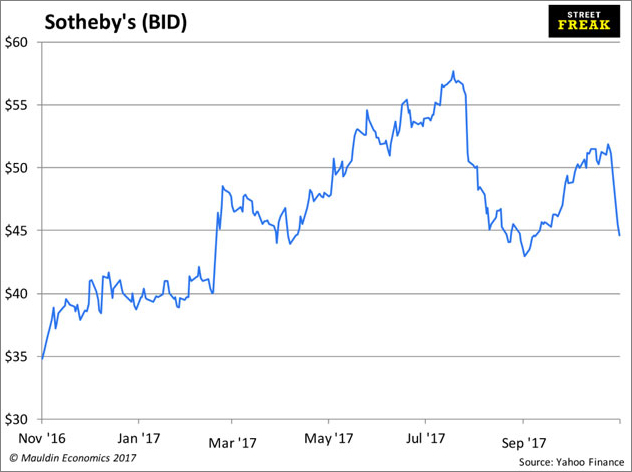

| -- | November 9, 2017 The Evidence Is Piling Up  I have been a bond bear for a while. Back in the summer of 2016, I spoke at a small conference out in San Diego. My topic: how interest rates were going to go up. It didn’t go over very well with people. One guy in the front row got really upset, and started sputtering about how I was totally wrong. He seemed pretty angry. I was actually a bit scared. I’ve been to some conferences where people were scratchy, but I never before thought I was going to get my ass kicked. I haven’t been invited back to speak, which is too bad—because I was right. When I gave that talk, yields on 10 year notes were about 1.6%. Today they are about 2.4%. That may not seem like a lot, but it is. The evidence is starting to pile up that yields may be going even higher. Quantitative Tightening As you know by now, the Fed is letting assets roll off the balance sheet. A little at first, but more later. This is not a small thing! New Fed Chairman Jay Powell wants this to be smooth as a gravy sandwich, but let’s see how it plays out before we take any victory laps. Meanwhile, the ECB is tapering, and will taper more… The BOJ has pegged the yield curve and buys bonds when the market forces them into it… The Bank of England seems to be finally lifting off… What had once been a flood of global liquidity is now starting to run in reverse. So, if you remember all the complaints about central banks, that: 1) They had inflated asset prices 2) And worsened inequality Then you can expect: 1) Asset prices to deflate 2) And rich people to get poorer This is what you have been waiting for, right? Rich people to lose money?  Rich people will lose money because asset prices will deflate. What kind of assets? Financial assets—stocks and bonds. Yes, in the next bear market, stocks and bonds will likely go down together. People have become accustomed to an inverse relationship between stock and bond prices. Funny thing about stock-bond correlation. The long-term average is zero. But sometimes it is 1, and sometimes it is -1. There are a lot of people holding 70/30 or 60/40 portfolios of stocks and bonds, thinking they are diversified. They are probably not diversified. To be diversified today, you need to be a bit more imaginative about what asset classes you include in your portfolio—and have a healthy dose of cash (we talk a lot about portfolio construction in ETF 20/20). Anyway, a pretty good leading indicator of asset prices deflating and rich people getting poor is Sotheby’s, the auction house. Quantitative easing didn’t just fluff up stocks and bonds, it fluffed up art and crap as well.  The chart is making lower highs. We might be onto something. FANG and Bitcoin The Chicago Mercantile Exchange is listing futures on FANG and bitcoin. You probably heard. And when I say FANG, I mean a small basket of stocks including Facebook, Amazon, Netflix, and Google. Most people would objectively say that FANG and bitcoin are bubbles. There might be some disagreement, but not much. The CME is getting pretty far away from its mission of providing a mechanism for managing or mitigating price risks in commodities. These products are purely for speculation. We’re not even sure that bitcoin serves any economic purpose. Let’s look at the history of listing derivatives on bubbles. The listing of ABX led to the destruction of the subprime mortgage market. The listing of CMBX led to the destruction of commercial mortgage-backed securities. Heck, even the Nikkei futures were listed right near the top of Japan, in 1989. And lots of people think that tulip futures are what did the tulips in. I was talking with a good friend the other day, a bond salesman who has been around for a while. He is fifty, and has quite a bit of grey in his beard. We were talking about how cool it was that 1 year Treasury bills yielded almost 1.5%, and how you can get 1.5% in an online savings account. I said to him, are you listening to us? We’re talking about T-bills. Nobody talks about T-bills. But in 1981, everyone was talking about T-bills. We will get back there eventually.

Jared Dillian

Editor, The 10th Man

| Get Thought-Provoking Contrarian Insights from Jared Dillian

Meet Jared Dillian, former Wall Street trader, fearless contrarian, and maybe the most original investment analyst and writer today. His weekly newsletter, The 10th Man, will not just make you a better investor—it's also truly addictive. Get it free in your inbox every Thursday. |

Jared's premium investment service, Street Freak, is available now. Click here for our introductory offer. Jared Dillian, former head of ETF Trading at one of the biggest Wall Street firms and author of the highly acclaimed books, Street Freak: Money and Madness at Lehman Brothers , and All the Evil of This World , shows you how to pick and trade trends, and master your inner instincts. Learn how to use “Angry Analytics” as a leading indicator of budding trends you can profit from… and how to view any market situation through the lens of a trader. Jared’s keen insight into market psychology combined with an edgy, provocative voice make Street Freak an investment advisory like no other. Follow Jared on Twitter at @dailydirtnap. Share Your Thoughts on This Article

http://www.mauldineconomics.com/members

Use of this content, the Mauldin Economics website, and related sites and applications is provided under the Mauldin Economics Terms & Conditions of Use. Unauthorized Disclosure Prohibited The information provided in this publication is private, privileged, and confidential information, licensed for your sole individual use as a subscriber. Mauldin Economics reserves all rights to the content of this publication and related materials. Forwarding, copying, disseminating, or distributing this report in whole or in part, including substantial quotation of any portion the publication or any release of specific investment recommendations, is strictly prohibited.

Participation in such activity is grounds for immediate termination of all subscriptions of registered subscribers deemed to be involved at Mauldin Economics’ sole discretion, may violate the copyright laws of the United States, and may subject the violator to legal prosecution. Mauldin Economics reserves the right to monitor the use of this publication without disclosure by any electronic means it deems necessary and may change those means without notice at any time. If you have received this publication and are not the intended subscriber, please contact service@mauldineconomics.com. Disclaimers The Mauldin Economics website, Yield Shark, Thoughts from the Frontline, Patrick Cox’s Tech Digest, Outside the Box, Over My Shoulder, World Money Analyst, Street Freak, Just One Trade, Transformational Technology Alert, Rational Bear, The 10th Man, Connecting the Dots, This Week in Geopolitics, Stray Reflections, and Conversations are published by Mauldin Economics, LLC. Information contained in such publications is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The information contained in such publications is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. The information in such publications may become outdated and there is no obligation to update any such information. You are advised to discuss with your financial advisers your investment options and whether any investment is suitable for your specific needs prior to making any investments.

John Mauldin, Mauldin Economics, LLC and other entities in which he has an interest, employees, officers, family, and associates may from time to time have positions in the securities or commodities covered in these publications or web site. Corporate policies are in effect that attempt to avoid potential conflicts of interest and resolve conflicts of interest that do arise in a timely fashion.

Mauldin Economics, LLC reserves the right to cancel any subscription at any time, and if it does so it will promptly refund to the subscriber the amount of the subscription payment previously received relating to the remaining subscription period. Cancellation of a subscription may result from any unauthorized use or reproduction or rebroadcast of any Mauldin Economics publication or website, any infringement or misappropriation of Mauldin Economics, LLC’s proprietary rights, or any other reason determined in the sole discretion of Mauldin Economics, LLC. Affiliate Notice Mauldin Economics has affiliate agreements in place that may include fee sharing. If you have a website or newsletter and would like to be considered for inclusion in the Mauldin Economics affiliate program, please go to http://affiliates.ggcpublishing.com/. Likewise, from time to time Mauldin Economics may engage in affiliate programs offered by other companies, though corporate policy firmly dictates that such agreements will have no influence on any product or service recommendations, nor alter the pricing that would otherwise be available in absence of such an agreement. As always, it is important that you do your own due diligence before transacting any business with any firm, for any product or service. © Copyright 2017 Mauldin Economics | -- |