| Bloomberg Evening Briefing Americas |

| |

| The miracle that is the post-pandemic US economy keeps chugging along, but there’s a big problem just below the surface, and it’s only getting bigger: debt. Outstanding US consumer debt surged by the most on record in December, reflecting massive increases in credit-card balances and non-revolving credit. Total credit jumped $40.8 billion, according to Federal Reserve data released Friday. The figure, which isn’t adjusted for inflation, topped all estimates in a Bloomberg survey of economists. Outstanding credit-card and other revolving debt increased $22.9 billion in December, more than reversing the prior month’s decline. Non-revolving credit, such as loans for vehicle purchases and school tuition, climbed $18 billion, the most in two years. The delinquency rate has risen, too, with some 3.5% of card balances past due by 30 or more days and 1.8% of accounts delinquent. Both figures are more than double the post-pandemic lows recorded in 2021. —David E. Rovella |

|

What You Need to Know Today |

|

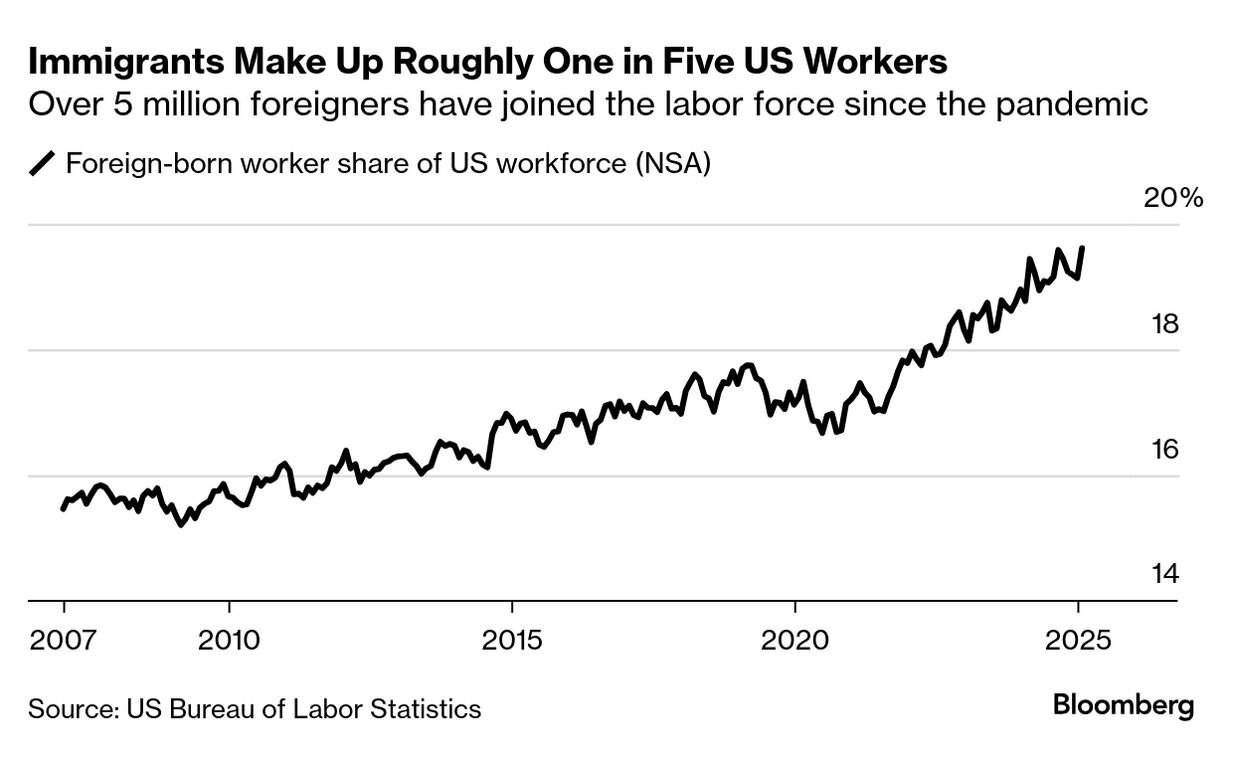

| Still, the US workforce expanded in a major fashion last month. The reason interestingly enough was a jump in immigration. Now, this huge source of job growth is at risk with President Donald Trump’s deportation policies. The US labor force grew by 2.2 million people last month, the most in data from the Bureau of Labor Statistics going back to 1948, and most of that came from foreign-born workers. Immigrants were also a key driver of job growth in 2024, Friday’s report showed. The number of employed foreign-born workers grew by 1.9 million in the year through January, compared to a gain of 766,000 for the native-born population. “The surge in net immigration was a key factor boosting US labor supply in the last couple of years, in turn alleviating the labor shortages that were so prevalent in 2022,” said Brian Coulton, chief economist at Fitch Ratings. |

|

|

| Though courts have blocked Trump’s facially unconstitutional order to pause all federal loans and grants (though it’s unclear if he’s obeying those orders), the damage has already been done when it comes to US banks’ ongoing support for nonprofit community groups all across America. From Wall Street giants like Bank of America and JPMorgan to smaller regional and community lenders, banks have hundreds of billions of dollars in loan exposure to people and groups that rely in some part on federal assistance. They loaned about $150 billion to community development groups and more than $320 billion to borrowers in low-income areas in 2022. Without federal funding, the creditworthiness of those groups suddenly came into focus last week with Trump’s trial balloon (likely headed to a potentially receptive Supreme Court), forcing their bankers to start figuring out a game plan before the order was ostensibly rescinded. |

|

|

| Among Trump’s growing list of potentially illegal or unconstitutional actions, he’s added another attempt to fire someone he doesn’t have the power to fire. He’s also seeking to unilaterally block a portion of the bipartisan infrastructure act, which like the TikTok ban he’s set aside is not his right to ignore, at least legally. Meanwhile, the government upheaval instituted by his multibillionaire assistant continues, with Elon Musk and his young aides, including a teenager previously fired from a company for leaking secrets, expanding their mandate to other agencies. Some employees of their original target, the US Agency for International Development, got a last-minute reprieve Friday thanks to another federal court ruling. Next up is the Consumer Financial Protection Bureau, created in the aftermath of the Wall Street-induced global financial crisis. (Musk has said succinctly: “Delete CFPB.”). More broadly, the administration’s shotgun approach to what closely resembles the Federalist Society’s “Project 2025” playbook moved a step closer to the Supreme Court yesterday, as Trump’s lawyers appealed one of their many district court defeats to the US Court of Appeals. As for the out-of-power Democrats, a senior member of Congress has urged an independent investigation into Musk’s unchecked activities inside the American government, calling the situation a “constitutional emergency.” But wait there’s more. Trump’s tax cut wish list would cost the federal government between $5 trillion and $11.2 trillion in lost revenue over the next decade, according to a new analysis from a budget watchdog group. The Committee for a Responsible Federal Budget, which advocates for shrinking deficits, estimated the bulk of the cost would come from extending portions of the 2017 Republican Party’s tax cuts during Trump’s first term, which largely benefitted the rich and corporations. Those cuts expire at the end of 2025. Trump’s overall tax plan would “explode” the debt and risk “a serious debt spiral,” the group said, unless they are offset with spending cuts or tax increases elsewhere. Maybe private equity can take some of the weight? |

|

|

| |

|

| While Musk and friends root around inside its computer systems, the US Treasury announced that it only has about $133 billion of extraordinary measures left, in addition to its cash pile, to help keep paying the government’s bills. That’s out of a total of $338 billion of authorized measures that were available to keep the government from running out of borrowing room under the statutory debt limit and is down from around $205 billion on Jan. 29. Treasury started taking the special accounting maneuvers as of Jan. 21 to avoid breaching the US debt limit, and urged lawmakers again to take steps to increase or suspend the statutory ceiling. |

|

|

| |

| Ukrainian President Volodymyr Zelenskiy said his team was working with US counterparts to coordinate with the Trump administration after the Republican suggested earlier Friday he’d be willing to meet. Separately, Zelenskiy said he was willing to make a deal to secure more US backing in exchange for some of Ukraine’s rare earths and other minerals, as suggested by Trump. “If we are talking about a deal, then let’s do a deal, we are only for it,” Zelenskiy told Reuters, adding that he was interested in cultivating a partnership with the US rather than giving resources away. The US and Ukraine have discussed storing US liquefied natural gas in underground Ukrainian gas storage sites, Zelenskiy added. |

|

|

| |

What You’ll Need to Know Tomorrow |

|

| |

| |

| |

| Enjoying Evening Briefing Americas? Get more news and analysis with our regional editions for Asia and Europe. Check out these newsletters, too: Explore all newsletters at Bloomberg.com. |

|

| |

Like getting this newsletter? Subscribe to Bloomberg.com for unlimited access to trusted, data-driven journalism and subscriber-only insights. Before it’s here, it’s on the Bloomberg Terminal. Find out more about how the Terminal delivers information and analysis that financial professionals can’t find anywhere else. Learn more. Want to sponsor this newsletter? Get in touch here. |

|

| You received this message because you are subscribed to Bloomberg's Evening Briefing: Americas newsletter. If a friend forwarded you this message, sign up here to get it in your inbox. |

|

|