| Plus, Iran scenarios and the Fed’s next move. |

| |

| Welcome back to The Forecast from Bloomberg Weekend, where we help you think about the future — from next week to next decade. After a very busy news week, this Sunday we’re looking at the economics of political unrest. The analysis below is about the Los Angeles protests and Donald Trump’s response — but on Saturday two Democratic Minnesota lawmakers and their spouses were shot. Meanwhile, anti-Trump “No Kings” protests took place in hundreds of US cities, coinciding with a military parade in Washington, DC and Trump’s 79th birthday. We’re also looking ahead to the Fed’s imminent interest rate decision — plus, what will consultants do with themselves once AI makes their PowerPoints for them? First, though, Israel and Iran. What to Watch for on Israel and Iran |

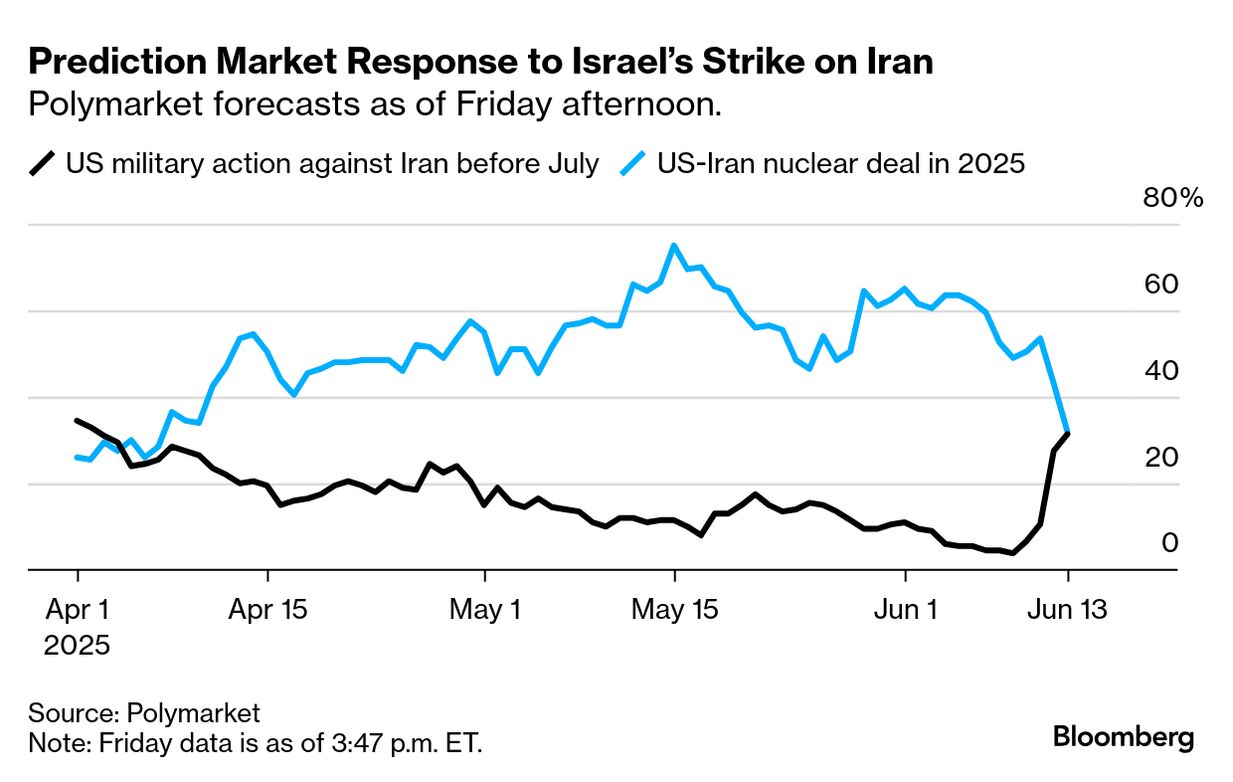

In an analysis early on Friday, Dina Esfandiary of Bloomberg Geoeconomics outlined three scenarios for what could happen next. Later on Friday, Israel retaliated against Iran. In Esfandiary’s first and most likely scenario, that’s where it stops, without an attack on the US. In a second scenario, Iran also retaliates against the US but with warning, and so avoids US casualties. Then there’s the worst-case scenario in which “Iran targets US positions in the region, and potentially even closes the strait of Hormuz… That leaves the US with no choice but to join the war on Israel’s side, leading to a larger regional war.” If the strait is closed “we estimate oil could go as high as $130,” she writes. (Terminal subscribers only.) Without US military assistance, Israel’s “ability to harm Iran’s main uranium-enrichment sites is more limited,” Bloomberg News notes. On Saturday, Israel extended its attacks and Iran fired back, as diplomatic talks between the US and Iran were canceled. For more, here’s Bloomberg’s explainer on the conflict and you can follow our ongoing coverage on Bloomberg.com. Prediction Markets We trust readers to interpret the prediction markets we cite each week cautiously; they’re useful but imperfect, and just one input among many. But this week deserves even more caution than usual: A lot of the relevant information is not public and outcomes may hinge on a few key decision makers. That makes this sort of crowd forecasting more difficult than usual. With that caveat in mind, on Polymarket the chance of a US-Iran nuclear deal dropped from roughly 50-50 on Thursday to 32% as of 3:30 p.m. ET on Friday. Meanwhile, the chance of US military action against Iran before July went from 10% to 32%. On Saturday, the prediction market for US military action against Iran reached as high as 62.5%, before falling again. As of Saturday evening at 5:45 p.m. ET it was bouncing around 38%. |

|

The Economics of Political Unrest |

|

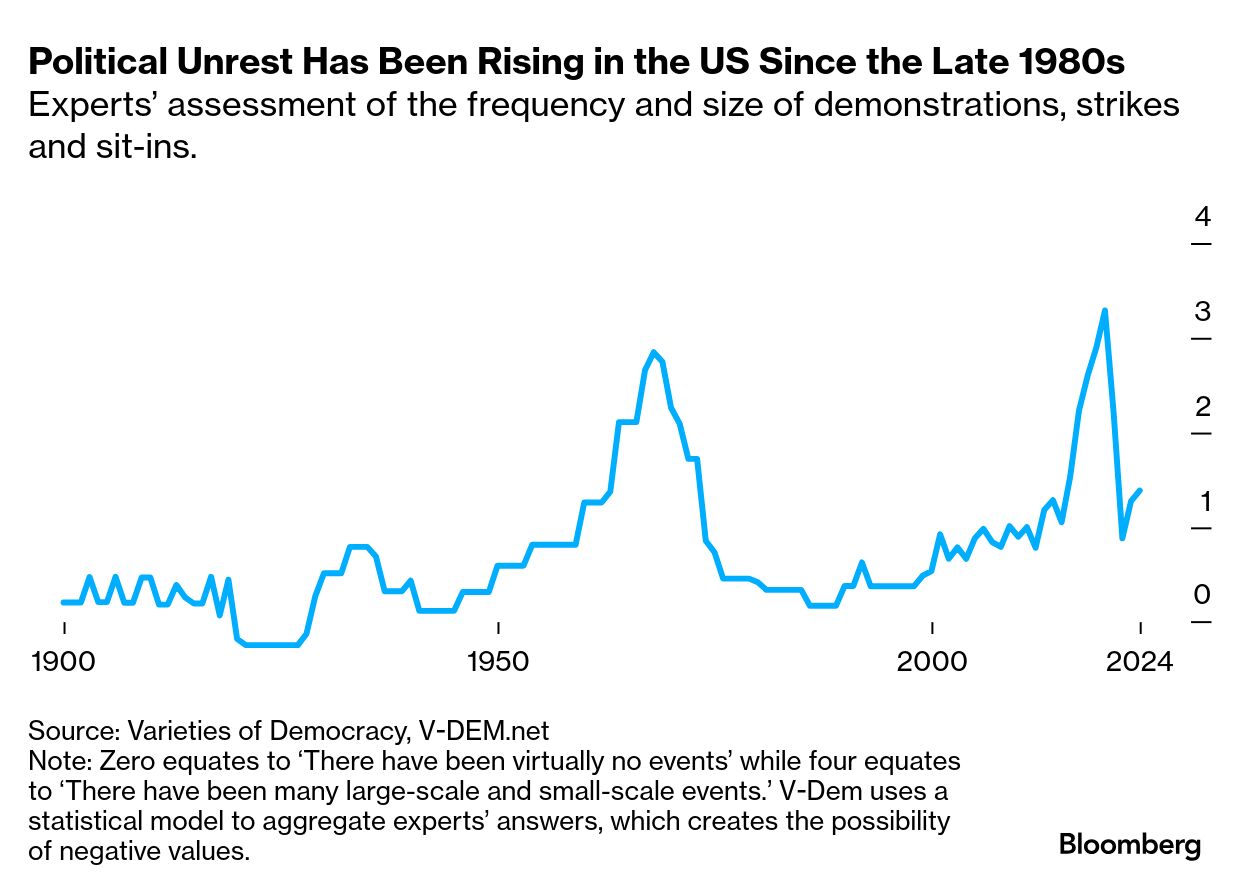

| Before the escalation in the Middle East, one of the biggest stories of the week was US President Donald Trump’s June 7 decision to deploy the National Guard in Los Angeles, a response to largely peaceful protests that the administration called a “rebellion” against the US government. It was the first time a US president deployed the National Guard without a state governor’s request since 1965. A few days later, 700 Marines were also on their way to LA, and the protests themselves spread to other US cities. But US markets have largely shrugged off the unrest, with the S&P 500 closing Thursday up about 75 basis points from last Friday, driven by tariffs and inflation news. Israel’s attack on Iran’s nuclear facilities caused stocks to fall on Friday, but the domestic unrest didn’t seem to rate. “From the outside [it’s] kind of counter-intuitive,” said Nick Hallmark, an economist at Bloomberg Economics. Political instability seems like the kind of thing that would spook investors and dent economies, but this week Hallmark published an analysis (Terminal subscribers only) suggesting that hasn’t historically been the case in the US. Hallmark’s analysis relied on data from a political science dataset called V-Dem, which asked experts “how frequent and large… events such as demonstrations, strikes and sit-ins” have been. He compared that data to both annualized GDP growth and growth in the S&P 500, going back nearly a century. Neither economic measure correlated with the protest figures. Years where the US saw more political protest and mass mobilization were neither particularly bad or good for markets and growth. Internationally, the story is very different. Research from the IMF has linked social unrest to lower GDP growth, lower stock market returns and weaker IPOs. Why the disconnect? In Shocks, Crises, and False Alarms, BCG economists Philipp Carlsson-Szlezak and Paul Swartz provide a helpful, back-to-basics way to think about such a question. In their chapter on geopolitics they remind readers that, “If a geopolitical shock is to impact the macroeconomy, it must work through real, financial, and/or institutional linkages.” In other words, to have an economic impact, political unrest has to actually constrain supply, demand or lending — or change how the government operates. On that last point, the IMF’s research concludes that the degree to which unrest translates into weaker financial performance depends on what the researchers refer to as the “quality of institutions.” Countries with less corruption, more political stability and secure rule of law tend to absorb protests and social unrest with fewer economic consequences. To date, that’s included the US. — Walter Frick, Bloomberg Weekend |

|

| |

| Consultants won’t need to make PowerPoints anymore. Accenture is using AI “to replace rote tasks like compiling presentations,” while “McKinsey & Co.’s consultants are increasingly drafting proposals and making PowerPoint slides using the firm’s generative artificial intelligence platform.” — Meg Short, Francine Lacqua and Omar El Chmouri, Bloomberg News Nicotine pouches will expand beyond dudes. “Selling to women will help startups and Big Tobacco alike capture a bigger share of the booming nicotine pouch market.” — Jonas Ekblom, Bloomberg News “Pandemic inflation is over. Note that I do not say, ‘Inflation is over.’ Between tariffs and lower immigration, higher inflation is likely. But… inflation has stabilized at a higher yet still tolerable level.” — Allison Schrager, Bloomberg Opinion The market for dollar-linked stablecoins could reach $2 trillion, says US Treasury Secretary Scott Bessent. — Jarrell Dillard, Bloomberg News India’s air conditioners won’t be allowed to be set lower than 68F (20C) according to a plan, in its initial stages, that would standardize the appliances so as to reduce energy use. — Rajesh Kumar Singh, Bloomberg News Superintelligent AI will arrive soon, but life “may not be wildly different.” Normally we stick to Bloomberg links here, but we couldn’t resist adding OpenAI CEO Sam Altman’s somewhat peculiar predictions, on his blog, about AI in the 2030s. Flat design is dead. Skeuomorphic design, where icons mimic 3D objects, is in the early stages of a comeback. — Austin Carr, Bloomberg Weekend Soon your orange juice will have even less real orange in it, replaced by “flavor packs” not listed on the ingredient label. — Ilena Peng, Bloomberg Weekend (Close readers will recall: We’ve covered end-of-orange-juice predictions before.) |

|

| |

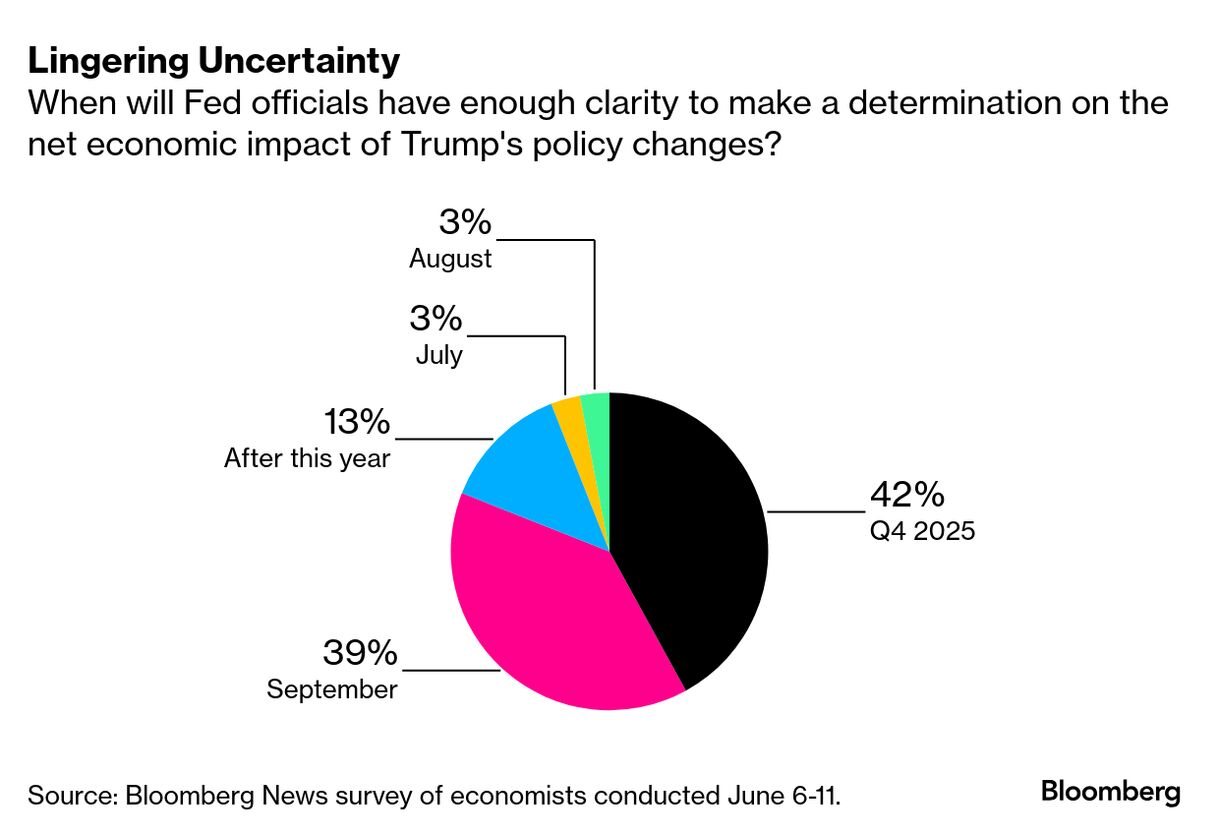

| What Would It Take for the Fed to Cut? With Federal Reserve officials signaling an extended hold on interest rates, investors and economists will look to Fed Chair Jerome Powell this week for clues on what could eventually prompt the central bank to make a move, and when. Trump has repeatedly called on the Fed to lower borrowing costs amid softer inflation data. But several Fed officials have made clear they can’t adjust rates until they know more about Trump’s final plans for tariffs, immigration and taxes. Meanwhile, the economy remains stable. Investors are betting the US central bank won’t lower borrowing costs until September at the earliest, according to pricing in futures contracts. The president’s tariffs are expected to raise prices and slow growth. Yet, so far the economy isn’t flashing any warning signs that would prompt the Fed to intervene anytime soon. Recent data showed only gradual cooling in the labor market while inflation has softened. New economic forecasts and rate projections from policymakers this week will be the first since Trump's “Liberation Day” tariff announcements, and could offer additional guidance on where officials see the economy headed. — Jonelle Marte, Bloomberg News |

|

What Are the Chances... | | 33% | | The chance Scott Bessent is nominated by Trump to be the next Fed chair, according to Kalshi. This week Bloomberg reported that the current Treasury secretary was emerging as a contender for the job. But bettors on Kalshi put former Fed official Kevin Warsh’s chances higher, at 44%. And Polymarket gives the best odds to Kevin Hassett, Trump’s current director of the National Economic Council. Forecasts as of 4 p.m. ET on Friday. |

|

|

| |

| |

| |

| Sunday: The G-7 Summit begins in Kananaskis in the Canadian Rockies. Monday: China publishes retail sales and production data; Nigeria and Italy report CPI. Tuesday: US reports retail sales; Japan’s and Chile’s central banks are both expected to leave interest rates unchanged; the US Senate resumes debate on the House tax bill; the UN General Assembly begins a summit on a Palestinian state. Wednesday: The Fed is expected to hold rates steady, as are the Central Bank of Brazil and the Bank of Indonesia; in Sweden, the Riksbank is expected to cut by a quarter point; the UK and South Africa report CPI. Thursday: The Bank of England will likely hold while the Swiss National Bank cuts a quarter-point; New Zealand reports GDP; US equity and Treasury markets are closed for Juneteenth. Friday: Japan reports CPI; the UK and Canada report retail sales. |

|

| Have a great Sunday and a productive week. — Walter Frick and Kira Bindrim, Bloomberg Weekend; Jonelle Marte, Bloomberg News |

|

| Enjoying The Forecast? Check out these newsletters: Explore all newsletters at Bloomberg.com. |

|

| |

Like getting this newsletter? Subscribe to Bloomberg.com for unlimited access to trusted, data-driven journalism and subscriber-only insights. Before it’s here, it’s on the Bloomberg Terminal. Find out more about how the Terminal delivers information and analysis that financial professionals can’t find anywhere else. Learn more. Want to sponsor this newsletter? Get in touch here. |

|

| You received this message because you are subscribed to Bloomberg's The Forecast newsletter. If a friend forwarded you this message, sign up here to get it in your inbox. |

|

|