January 17, 2025

The Liquidity Injection We’ve Been Looking for May Be Here

Dear Subscriber,

|

| By Juan Villaverde |

The current bull cycle has been going strong for over two years now.

If you’re familiar with my crypto cycles, then you’ll know that bull markets typically last about three years.

That means this is likely the final year for the current bull run.

Don’t let that get you down. The final year is also typically the most exhilarating. So much so that I call it the “Bigger Bull” year.

This is when I expect to see the biggest gains of this bull cycle.

Of course, the size of this next rally will be dependent on global liquidity improving, as well. And there are a few compelling signs that’s exactly what we should expect to see.

The Case for Liquidity Reversal

What I’m seeing in the macroeconomic landscape today looks eerily similar to the conditions I saw back in late 2022 and early 2023.

You know, the very period that kick-started the current crypto bull market.

In late 2022, liquidity conditions were so tight that bond markets worldwide began to crack. Yields surged week after week, causing sovereign bond markets to teeter on the brink of collapse.

Nowhere was this more evident than in the U.K. gilt market, where a full-blown meltdown was only narrowly averted in October 2022.

As I’ve pointed out many times, today’s sovereign bond markets cannot survive without a steady inflow of new money. Central banks may hit pause on moneyprinting from time to time. But eventually, they will be forced to intervene.

That’s exactly what happened in the fourth quarter of 2022. Because the pressure became unbearable.

Yet central banks rarely admit when they print to bail out debt-ridden governments. It’s bad optics. Instead, they wait for a "legitimate" excuse.

In early 2023, the U.S. Federal Reserve found one when America’s banking sector began to unravel.

Faced with skyrocketing bond yields, banks’ fixed-income portfolios were eviscerated. At the same time, panic withdrawals by depositors triggered liquidity shortfalls across the sector.

What resulted was the banking crisis of March 2023 as Fed officials reacted the only way they could — by injecting vast amounts of liquidity into the system.

Of course, they dressed it up with plenty of euphemisms. But the markets weren’t fooled … and neither was I.

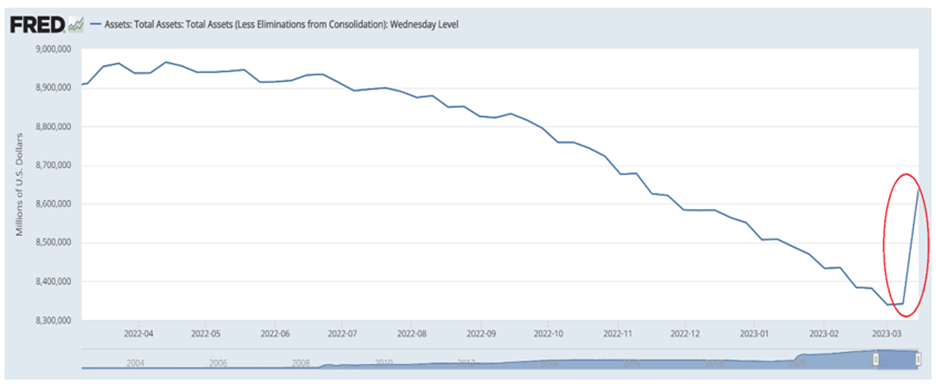

Just two weeks after the banking crisis began, I showed you this chart:

It shows the Federal Reserve’s balance sheet from the time.

See the red oval at the far right-hand side?

That is over $300 billion freshly printed dollars in a week! Enough to reverse several months of quantitative tightening. As you can see, the Fed went right back to old-fashioned money printing to prevent systemic collapse, plain and simple.

Fast forward to today, and the situation looks strikingly similar. Only this time, banks won’t be at the epicenter of the crisis.

Instead, all eyes will be on insurance companies.

A “Bank Run” on Insurance Companies?

The financial burden this puts on insurance companies is crushing. And not just because they’re on the hook for billions in expected claims, though those are noteworthy.

Just consider the wildfires raging through Southern California.

My heart goes out to everyone living through such a heartbreaking situation. And I hope that anyone who needs to will be able to rely on their insurance to help them on the other side of this tragedy.

Though that may be a tall order.

Until now, the most expensive wildfire in U.S. history occurred in 2018, with damages totaling $12.5 billion. This year’s fires have already exceeded that amount by more than 10-fold.

Current estimates run $150 to $200 billion … and rising every day the fires rage.

But there’s a thorn in the side of these insurance companies: Rising interest yields are hammering their bond portfolios.

Just like what happened to the banks in 2023.

What if they’re forced to sell them to generate cash to pay out claims? Well, that would lock in massive losses, dragging many companies to the brink of insolvency.

With both the banks in 2023 and insurance companies today, a cratering bond market combined with an unforeseen external calamity was enough to send seismic shocks to the very foundation of the financial sector.

The solution back then was clear. And it’s the same today: print money. Lots of it. The Fed’s playbook hasn’t changed.

In 2023, Fed officials acted decisively to stop the contagion, even as they obscured the real reasons for this action under layers of technical jargon.

If insurance companies start to topple under the weight of this year’s natural disasters, I expect to see a similar response. Indeed, the pieces are all already in place — even if we haven’t quite hit the critical breaking point just yet.

That means the next wave of liquidity is already brewing. And it could emerge from an unexpected corner of the financial system.

Whether ostensibly triggered by insurance claims, bond market stress or some other external jolt to the system, the result will likely be the same …

Central banks stepping in with fresh injections of cash.

And you already know what happens to asset prices when the floodgates open.

But I don’t anticipate this latest round to just stabilize the crypto markets. I believe it will fuel the next major leg of the crypto bull market.

So, stay alert, and stay tuned in to Weiss Crypto Daily for all my updates on this evolving situation.

Best,

Juan Villaverde