| | | | Welcome to Deep Dives, where we explore interesting companies in the alt investment space. | Today we've got a deep dive on Heron Finance — the private credit industry’s first robo-advisor | With Heron, you’re not directly purchasing shares of a private credit fund. Instead, you’re buying contingent payment notes backed by equity in third party private credit funds — and you receive cash dividend distributions. | It’s complicated. But being a Heron Finance client is trusting their ability to make it simple for you. |

| |

| | |

|

Good morning! |

With the Fed finally cutting interest rates, the gravy days of attractive bond yields are likely on their way out. |

So where do you go now if you’re looking for better income generation? |

If you’re an affluent investor who’s open to looking beyond what’s traditional, private credit could be an attractive alternative investment option. |

The challenge: Unless you work on Wall Street, it’s incredibly difficult to find, evaluate, invest in and manage these opportunities on your own. |

Fortunately, you don't have to. San Francisco-based Heron Finance claims that it enables investors to build a customized portfolio of exposure to private credit loans that reflects their unique yield requirements and risk profile. |

|

Heron Finance is not a private credit fund that locks up investors’ money for years. It's an SEC-registered investment advisory firm, who is required by law to always act solely in your best interests. |

It's the industry’s first private credit robo-advisor |

But before we take both a bird’s eye view and deeper dive into Heron, let’s spend a minute discussing private credit in general. |

Let's go 👇 |

Note: Jeffrey Briskin is a veteran Boston-area financial writer and marketing consultant. His past work with Alts include deep dives on Life Time Fitness, Sensate, and Geoship. Jeffrey is also the author of the best-selling Biblical crime novel, Bethlehem Boys. This issue is sponsored by our friends at Heron Finance, with research & due diligence performed by the Alts team. As always we think you'll find it very informative and fair. |

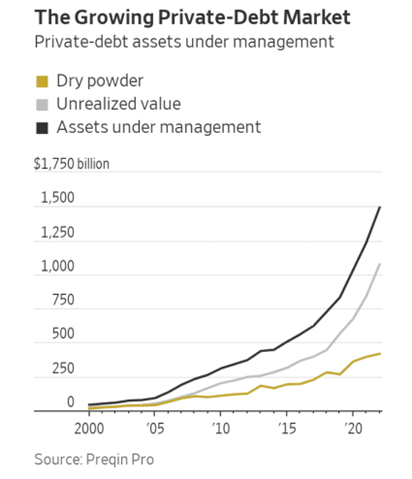

A growing, $1.5 trillion opportunity |

As discussed in a previous article, the private debt market has exploded in recent years, rising to $1.5 trillion in 2023 and representing 14% of all non-financial corporate debt in the U.S. |

| The post-pandemic period has been a good one for private borrowers. Source: The Wall Street Journal. |

|

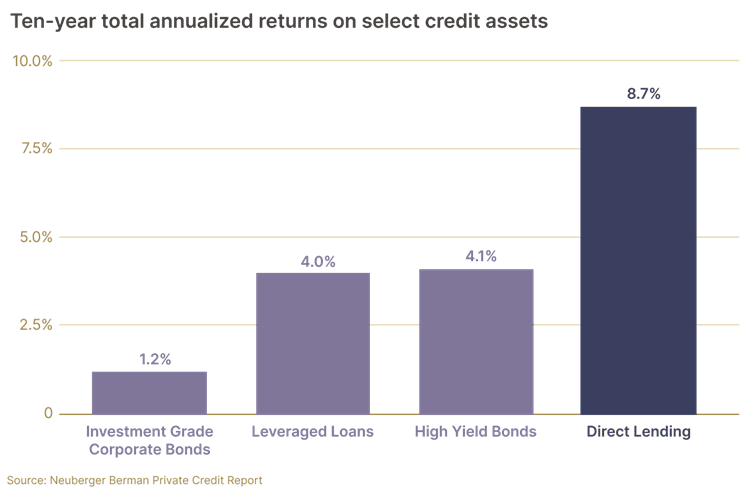

And, according to Neuberger Berman, private debt has delivered better 10-year returns than other credit classes. |

| If you believe Neuberger Berman, private credit has delivered more than twice the returns of other credit classes. |

|

Here’s how it works |

Many private companies want to avoid the hassles of dealing with bank lenders. |

| When it comes to considering loan requests for private companies, many bank managers act like Mr. Potter from It’s a Wonderful Life. |

|

Instead they seek funding from non-bank lenders like private credit firms, including Business Development Companies (BDCs). |

Funding private companies often entails greater risks, which is why borrowers generally are willing to pay significantly higher interest rates to creditors. |

These higher interest rates can result in higher returns than stocks and bonds for investors. |

Heron Finance claims that the loan exposures in its clients’ portfolios could consistently generate annual yields between 7%-12%, net of fees. |

(The operative word here is “could.” More on this later.) |

Is now a good time for private credit investing? |

Unlike fixed-rate corporate bonds, most private credit loans have floating interest rates that rise or fall with prevailing interest rates. This benefit can make them more attractive relative to some fixed-rate bonds when interest rates rise. |

However, this also forces private companies to make higher payments when the Fed raises interest rates, as it’s done for the past few years. |

If the Fed follows through on its goal of additional interest rate cuts, this could be good news for private borrowers. They’ll be able to lower their monthly payments, which should give them greater financial breathing room. |

And if President-elect Trump and his congressional allies follow through on their plans to extend or expand tax cuts for the wealthiest Americans, this will put a lot more money in the hands of investors who are looking for ways to broaden their exposure to private companies. |

Why private credit funds are a safer alternative for most investors |

High-net-worth and institutional investors often invest in private credit funds which then lend money to individual companies. |

It takes a high level of time and expertise to evaluate the risk/reward potential of lending funds to private companies, which is why many wealthy investors invest in private credit funds rather than directly lend to companies. |

Bundling loans into a commingled investment |

The role of a skilled private credit manager is to seek out and finalize lending agreements with private companies. |

These arrangements may include secured and unsecured loans, which are then bundled into private credit funds.. |

Investing in individual funds may not be the best option |

Most private credit funds are not SEC-registered, and therefore aren’t subject to the regulations and reporting requirements that govern most mutual funds and ETFs. |

Many of these funds may require you to lock up your money for years, only returning your principal when they close. Interval funds may only allow you to request redemptions once per quarter or even longer. |

In some cases, private credit funds are “exclusive” offerings of specific broker/dealers. If you want to own many different private credit funds, you might have to work with several different brokers, which can create a logistical hassle, especially when tax time comes around. |

Heron Finance claims it offers a better alternative. |

|

A government-regulated private credit adviser |

Heron Finance isn’t a private credit fund that locks up investors’ money for years. It’s not a broker/dealer that earns huge commissions selling private credit funds. |

It’s an investment advisory firm whose mission is to invest clients’ money in a customized portfolio of high-quality, institutional private credit funds. |

Heron’s fees are paid only by clients. Unlike broker/dealers, it doesn’t receive compensation or commissions from the funds it uses. |

The industry’s first private credit robo-advisor |

You probably already know what a robo-advisor is. You invest a certain sum with a company like Betterment or Wealthfront, and the platform’s algorithms allocate your money to stock, bond and money market funds and ETFs based on your investment objectives, timeframe and risk tolerance. |

Heron Finance does the same thing with private credit. |

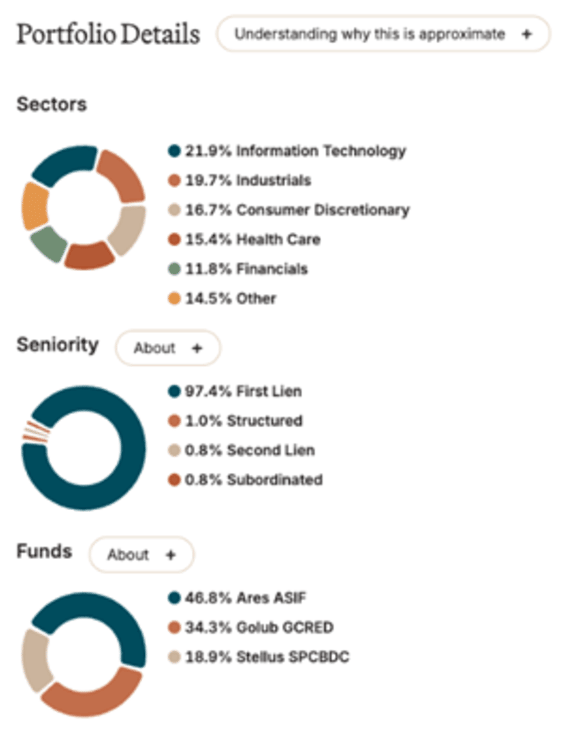

Its robo-advisor takes your initial investment to build a personalized portfolio that gives you exposure to a variety of institutional-grade private credit funds based on your financial goals and risk profile. |

| A hypothetical Heron Finance client portfolio based on a moderate risk stance. |

|

Your portfolio will also provide exposure to various sectors of the economy, which can help reduce overall risk when some industries face difficulties in challenging economic or geopolitical environments. |

Not the same as investing in a mutual fund |

When you become a Heron client, you’re not directly purchasing shares of a private credit fund. |

Instead, according to Heron, your investment buys you a quantity of contingent payment notes issued by Heron that are backed by equity interest in third party institutional-quality private credit funds managed by leading investment firms. |

On either a monthly or quarterly basis, Heron receives a cash dividend from the BDCs, which it distributes to investors based on their exposure to these BDCs. |

Sounds complicated? |

It is. One aspect of being a Heron Finance client is trusting their ability to manage the complexities of the private credit space. |

|

Proven private credit credentials |

Established in 2024, Heron Finance is the brainchild of Mike Sall and Blake West, co-founders of Goldfinch, an open-source, blockchain-based credit protocol that enables decentralized lending in emerging credit markets. Since Goldfinch was founded in 2021, it has facilitated over $110 million in private loans across more than 20 countries. |

| Sall and West founded Heron Finance as a completely separate entity from Goldfinch. That’s intentional, for their mission in hatching Heron was to leverage their expertise in the private credit world to make this alternative asset class available to affluent investors in a more traditional, regulated robo-advisory platform. |

|

Leading Heron’s private credit vetting process is Chief Credit Officer Khang Nguyen, who has nearly two decades of private credit research and investment experience. |

According to Nguyen, Heron’s credit team combines fundamental research and technical analysis to evaluate, monitor and score third-party private credit funds. |

Some of the criteria that Heron uses to review private credit funds include: |

At least a decade of experience structuring and managing loans across business cycles.· Several billion dollars of assets under management. Strong returns and consistent distributions. Low non-accruals and realized losses. High allocations to first-lien loans. Low to moderate use of leverage.

|

Only those funds that meet Heron’s exacting criteria are added to its “approved fund” lists. |

But the process doesn’t stop there. If the factors that got the fund onto the list begin to falter, they’ll remove it—even if this means shifting investors’ assets to another fund. |

Not for everybody |

To become a Heron Finance client, you must be an accredited investor. To qualify you must meet at least one of these requirements: |

You must have an annual income of $200,000 or more ($300,000 joint income if married) for the past two consecutive years. You must have at least $1 million in investable assets, not including your primary home. You must be an investment adviser or broker who is licensed to work in the private investment space. You should also be a sophisticated investor who fully understands the unique risks of participating in private markets.

|

These requirements aren’t unique to Heron. Most private equity and credit funds also limit participation to accredited investors. |

Applying and onboarding |

You can get the process rolling by applying online. |

You start by answering questions to determine whether you meet the qualifications for an accredited investor. Be honest, because they’ll ask you to prove it later. |

You then answer a few questions to determine which kind of yield range you’re looking for and your unique risk tolerance. |

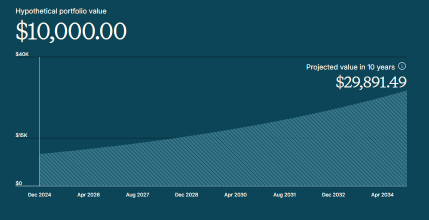

After submitting a request to open an account (and verifying it via email) you’re presented with a chart showing the hypothetical growth of your portfolio over a time range you’ve chosen. |

| This chart reflects hypothetical returns based on an “aggressive” risk tolerance profile and a 10-year timeframe. |

|

You’re all set to invest, right? |

Wrong. Like any investment adviser, Heron Finance must follow industry-standard “Know-Your-Client (KYC)” requirements. |

You’ll need to enter personal information like your name and Social Security number and eventually upload documents that verify your identity, income, net worth and other factors. |

|

Once this information has been verified and your account has been established, you should be able to make your initial investment through an electronic funds transfer. |

Once Heron receives the funds, its robo-advisor will suggest an allocation of private credit funds that reflects your yield range and risk profile. Once you accept it, your money will be invested accordingly. |

Rebalancing, redemptions and online access |

Like all robo-advisors, the Heron platform can periodically rebalance your portfolio to its original allocation to keep it aligned with your risk and yield objectives. |

Keep in mind that yours is a taxable account, so rebalancing could result in capital gains. But you won’t have to figure these out on your own, as Heron will provide you with 1099 statements and other documents you’ll need for tax-filing purposes. |

You’ll also be able to access your account online, where you can view current values and performance metrics, make additional investments, or request redemptions. |

That’s right. Unlike other private credit funds, which may lock up your money for years, you can request a redemption at any time. |

However, due to the generally illiquid nature of the private credit funds it invests in, Heron reserves the right to only fulfill these requests on a specific schedule, usually once per quarter. |

It’s also important to reiterate that all investment transactions are conducted by Heron’s robo-advisor. Your portfolio won’t be managed by a human investment adviser and you won’t be able to meet with one. |

However, Heron does have in-house client service representatives who can handle non-investment technical and funding requests and resolve problems. |

Management fees |

Most investment advisers charge annual management fees based on the value of their clients’ accounts. Heron is no exception. Their standard annual fee is 1%, with reduced fees for larger accounts (see their Form CRS for details). |

Heron says that the yield and distributions you’ll see in your portfolio and statement are net of fees. But whether they show the actual fee amounts is unknown. |

And it’s also not clear whether the funds or BDCs Heron uses charge their own fees (like the 12b-1 fees many mutual funds charge), which could be “shaved” from the returns they deliver. |

The reassurance of working with a fiduciary |

As an SEC-regulated investment adviser, Heron Finance is legally required to act as a fiduciary. In practical terms, this means that: |

All investment decisions made by the firm and the robo-advisor must always be in each client’s best interests and reflect their unique investment goals and risk tolerance. Heron doesn’t receive commissions, payouts or other compensation considerations from the private credit funds and BDCs it uses with Heron clients. Instead, revenue comes directly from fees paid by investors. Heron clients receive the same kinds of detailed ongoing reporting that investors with human advisors receive, including quarterly statements and performance reports. If there are possible conflicts of interest that could keep Heron from acting solely in its clients’ best interests, Heron must try to minimize their impact and must also fully disclose them in their Form ADV, which any potential investors should thoroughly review.

|

Are there risks? |

Certainly. Many private credit funds aren’t regulated by the SEC, which means that they don’t need to be as accountable or transparent in their practices as their publicly traded counterparts. |

Many of the companies these funds loan money to may be depending on this capital to remain in business, especially if they’re startups that aren’t generating significant revenue. |

If a long-lasting recession or bear market occurs, many of these companies may see their sources of funding dry up. This may cause many to dissolve, leaving a mob of creditors—including private credit funds--to fight over the few tangible assets that remain. |

Heron claims that its business model helps minimize these risks. |

Requiring funds on its pick list to meet its strict performance, quality, and low-leverage and loss standards could provide a higher level of protection for its clients. |

However, Heron Finance has been in existence for less than a year and it’s only recently started accepting client investments from those other than “friends and family.” |

The firm hasn’t built a track record to prove that its approach works over the long-term, so investors who sign up may need to take a leap of faith in trusting Heron’s ability to deliver solid results year after year. |

How much should you invest with Heron? |

Even if you’re completely sold on the merits of private credit in general and Heron Finance in particular, you won’t want to go all-in with either. |

If you work with an investment adviser, you might want to get their take on Heron before you take the plunge. |

Even if they give Heron the thumbs up, they’ll probably tell you that unless you’re a one-percenter you shouldn’t allocate a huge percentage of your portfolio to alternative investments in general or to any one asset class in particular. |

If you don’t have an adviser and still want to become a Heron Finance client, you might want to start with a small initial investment, see if it provides consistent yield and then add more later if you like the results. |

Ready to fly with Heron? |

You can start the process right now. |

But before you sign up, you should take some time to review their SEC-required disclosures that provide far more details about the company, its business model and its fee structure. |

|

|

That's it for today. Reply with comments, we read everything. |

See you next time,

Jeff |

Disclosures from Alts |

This issue was sponsored by Heron Finance Due diligence was performed by Jeffrey Briskin. Editing was done by Stefan von Imhof. Neither the author, nor the ALTS 1 Fund, nor Altea holds any interest in Heron Finance This issue contains no affiliate links

|

Disclosures from Heron Finance |

Because Heron Finance is a regulated investment adviser, it’s required to add certain disclosures to articles that they pay others to create, even objective reviews like this one. So, here they are (note: most of this language comes from the Heron Finance website, and is what you would see if you went there. |

This is a paid advertisement. Alts.co is a paid publisher and not a client of Heron Finance and receives compensation for this endorsement. Please note there are no material conflicts of interest related to this endorsement. The views expressed in this article do not necessarily reflect the views of other clients. Past performance is not indicative of future results. We encourage you to consider your individual investment objectives and risk tolerance before making any investment decisions. For more detailed information, including our Form ADV, please contact Heron Finance directly. |

The information on Heron Finance’s website does not constitute an offer to sell securities or a solicitation of an offer to buy securities. Further, none of the information contained on Heron Finance’s website is a recommendation to invest in any securities or a recommendation of any interest in any investment. Any financial forecasts or financial returns, whether in the form of dividend yield or capital appreciation displayed on Heron’s website are for illustrative purposes only and are not a guarantee of future results. Private credit investments are subject to credit, liquidity, and interest rate risk. In the event of any default by a borrower, you will bear a risk of loss of principal and accrued interest on such loan, which could have a material adverse effect on your investment. A borrower may default for a variety of reasons, including non-payment of principal or interest, as well as breaches of contractual covenants. Credit risks associated with the investments include (among others): (i) the possibility that earnings of a borrower may be insufficient to meet its debt service obligations; (ii) a borrower's assets declining in value; and (iii) the declining creditworthiness, default, and potential for insolvency of a borrower during periods of rising interest rates and economic downturn. |

Any investment target yield presented here is intended for informational purposes only and does not guarantee future performance or results. This model assumes no variability, including no loan defaults, fluctuations in interest rate, customer withdrawal requests, late payments, or penalties, and our management fees have remained unchanged throughout this projection. Please be aware that all investment involves inherent risks, and past performance is not indicative of future outcomes. Customers are advised to consult their own legal and tax advisers regarding their specific circumstances and needs. Heron Finance does not accept any liability for any loss or damage arising from the use of this information or for any actions taken based on this information without seeking professional advice. |

No communication by Heron Finance or any of its affiliates through its website should be construed or is intended to be investment, tax, financial, accounting, or legal advice. Heron Advisory, Inc., d.b.a. Heron Finance is an SEC-registered investment advisor (RIA). Such registration should in no way imply that the SEC has endorsed the entities, products or services discussed herein. |