| The Uranium Opportunity — The Good and the Bad |

Thursday, 30 May 2024  | | By James Cooper | | Editor, Mining: Phase One and Diggers and Drillers |

|

Twitter (X): @JCooperGeo [6 min read] | In this Issue: - Uranium: strong demand but supply gluts loom

- Oil and Gas could be the Goldilocks energy play

- The problem is not a failure of capitalism at all, but the inevitable overreaching of government and the elites that control it.

|

|

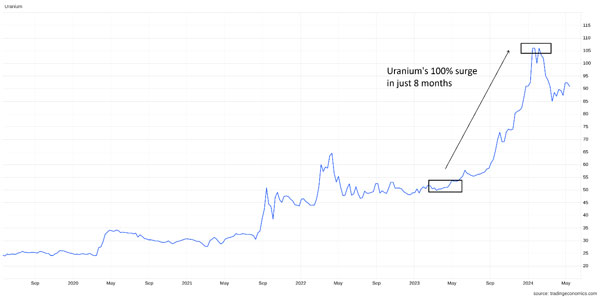

Dear Reader, If you’re late joining the uranium bandwagon, don’t worry; you’re not the only one! Last week, I put together a detailed report on the uranium market, something that’s been a long time in the making. It was part of our monthly recommendation to my paid membership group, Diggers and Drillers, in which we finally pulled the trigger on our first uranium position. But has that come too late? This commodity has already surged from just over US$50 per pound in April 2023 to more than US$100 per pound by January 2024.

Since then, there has been a moderate pull-back; uranium is now consolidating just above US$90 per pound. Can uranium rip higher from these

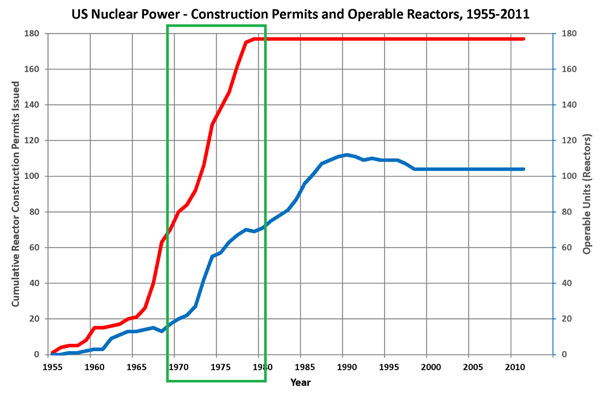

elevated levels? Well, that depends. Last year’s terrific run was driven by strong demand outlooks. Uranium, the fuel for nuclear reactors, has benefitted from renewed interest in building global nuclear capacity. That’s partly due to the push to go green. Here, nuclear power offers baseload power that’s carbon-free and reliable. Whether night or day, cloudy or windless, nuclear provides uninterrupted power. But there’s another important side to the nuclear story: costs are rising. Despite central bankers’ claims to the contrary, inflationary pressures continue to loom. Rising tariffs and trade tensions between the world’s two largest economies, China and the West, threaten to bifurcate global trade. This is highly inflationary and occurs just as the West ramps up broad trade embargoes against Russia, one of the world’s most resource-rich nations. Meanwhile, conflict could erupt at any time in the Middle East. A regional spillover could have drastic implications for global oil supply. This 1970s setup could be good for uranium I’m not the first to draw similarities between today’s inflationary environment and those from the 1970s. Back then, the war in Vietnam helped drive copper prices to extreme levels, above US$15,000 per tonne. Meanwhile, OPEC oil embargoes in the early ’70s caused the price of oil to quadruple in the US. As inflation rocketed higher, households sweated under a cost-of-living crisis. Governments were forced to find solutions. This offered a fertile environment for the nuclear industry to expand. As a source of relatively cheap baseload power, it offered a proven long-term solution to the global energy problem. As you can see below, the US had fewer than 20 nuclear power facilities at the beginning of the 1970s. But by the decade's end, the country had around 75 reactors in operation.

Undoubtedly, nuclear was viewed as a long-term strategy to tackle the 1970s cost-of-living crisis. Not surprisingly, the commodity fuelling these reactors went skyward. Adjusted for inflation, the price of uranium shot past US$200 per pound by the late 1970s. A record that stands today. Today, uranium trades at less than half that price. It begs the question…could we see another record high at some point in the 2020s? If you believe the 1970s offers a blueprint for today’s economy, it’s certainly possible. Inflationary pressures loom large against the backdrop of war, tariffs, embargoes and threats to energy security. The political will to push nuclear expansion will only increase on the back of these drivers. But what about the other side of the

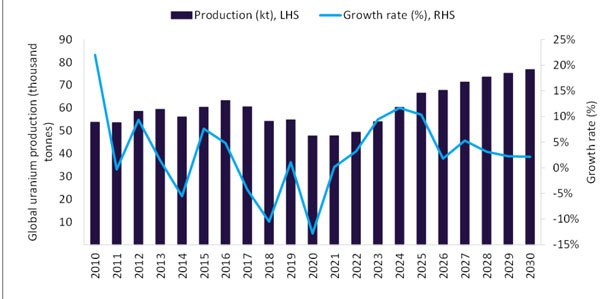

uranium story…supply? As the Canadian mining magnate Robert Friedland once stated, the set-up for higher commodity prices consists of one-third demand and two-thirds supply. So, how does the uranium supply story stack up? The outlook here is slightly less rosy for uranium investors. Kazatomprom, the world’s largest uranium miner, is set to resume full production next year, removing production cuts adopted during uranium’s prolonged bear market following the Fukushima nuclear disaster. Meanwhile, the world’s second-largest miner, Cameco, is looking to ramp up its McArthur River operation in Canada. This will add a further 6.9kt of uranium to the global feedstock. According to GlobalData, worldwide uranium production is expected to grow with a compound annual growth rate of 4.1% from 2024 to 2030, with output reaching 76.8kt by 2030. So, what does that mean? Rising output could defuse uranium’s long-term bullish outlook. Plus, several other sources of new supply are set to hit the market in the coming years… Paladin [ASX:PDN] is underway with restarting its Langer Heinrich uranium mine in Namibia. The mine is expected to deliver 6 million pounds annually at full production, enough to supply over ten 1,000 megawatt nuclear power plants for a year. Then there’s South Australia’s Honeymoon operation. This was Australia’s second operating in-situ recovery uranium mine…the timing was unfortunate; production started alongside the infamous Fukushima disaster in 2011. Operations at Honeymoon were suspended in 2013 due to falling uranium prices. In 2015, Boss Energy [ASX:BOE] acquired the project and finally recommissioned the mine with production resuming earlier this year. Then there’s the Kayelekera Uranium Project in Malawi. Its new owners, Lotus Resources [ASX:LOT], also plan to bring the mine out of care and maintenance. So why is this a potential threat to the uranium market? Fully permitted mines with infrastructure already in place means several operations could come online simultaneously, easing any potential supply squeeze driven by demand. So, should you be getting into this market? For now, investors remain laser-focused on the demand outlook. That means there’s still plenty of room to ride momentum in the uranium market. In the long term, though, demand must overcome higher production threats. A 1970s-like cost-of-living crisis could be exactly the type of high demand scenario bringing more reactors online and more demand for this commodity. But uranium won’t be the only winner in this scenario…oil and gas stocks could emerge from the ashes amid rising energy costs. This is another energy sector that’s worth watching closely. Especially while energy markets remain in a temporary lull. We’ll have much more to say about that next week. Until then.

Regards,

James Cooper,

Editor, Mining: Phase One and Diggers and Drillers James Cooper has been a working geologist in mines across Australia, Canada, and Africa since the early 2000s. He’s led the operations of tiny explorers through to huge producer outfits. He’s seen booms and busts firsthand and he also understands the cyclical nature of individual commodities. For example, James was right there when Barrick Gold launched an enormous $7.5 billion takeover bid for Equinox. That was the peak of the last cycle. With his background as a geo and finance professional, he brings a unique insight and experience to Fat Tail Investment Research. He writes the broader resource-focused investing letter Diggers and Drillers and the ultra-speculative explorer-focused trading service Mining: Phase One. Advertisement: Will this no-name stock rule the ‘Aussie Mining Boom 2025’? It’s showing all the traits, ambition and foresight that Andrew Forrest’s Fortescue Metals had in the early 2000s. Market cap just $270 million. And a gameplan that’s addressing many of the same challenges Fortescue Metals Group faced in the 2000s. This very small company is about to unlock a very big deposit. The largest of its kind IN THE WORLD. Its potential has arrived from nowhere, busting into ‘Tier 1’ status and attracting mining behemoths…including Rio Tinto. This has all the makings of a classic rags to riches story. Click here for the full take. |

|

What Went Wrong

with Capitalism |

| | By Bill Bonner | | Editor, Fat Tail Daily |

|

[3 min read] After driving up above 40,000, the Dow closed yesterday at 38,852.

Where will it go from here?

We don’t know. No one does.

Our bet is that the Primary Trend has reversed...from bull to bear...greed to fear...up to down.

Assets, in other words, are likely to be cheaper — in real terms — than they are now.

And when major turning points are hit...the market usually does not revisit its highs (or lows) until the see-saw has completed its stroke in the opposite direction. From major high...to major low — a roundtrip that can take decades; the Dow is not likely to hit a genuine new high — inflation adjusted — until it bounces off a genuine new low. Currently, adjusting the Dow for inflation would put a new high around 44,000 or 45,000.

In gold terms, the most recent high, recorded in the fall of 2021, had the Dow worth 20 ounces of gold. Returning to that high would mean a Dow of 46,000 today. Anything is possible. But we don’t expect it. Not anytime soon.

Mr. Market can do whatever he wants. Still, it’s best for us to think that he’s following the pattern of the past. Otherwise, we’re totally lost...and even if we turn out to be wrong, it’s still probably best to stick with the program. You might miss a little upside, but you will more likely dodge a lot of downside…including the Big Loss that we want to avoid. Soft slush

Meanwhile... we turn to the Financial Times, the ‘pink paper’. It is always fun to read, reliably wrong on just about everything. Its columnists are often pompous or silly. Their opinions are sometimes pathetically shallow. And the paper’s point of view is anchored in ‘dirigisme’, the soft slush of central planning, which Friedrich Hayek showed, convincingly, doesn’t work.

But the FT is the newspaper you find in government offices, think tanks, embassies and corporate headquarters all over the planet. Its chief economic commentator, Martin Wolf, is widely regarded as one of the world’s most important thinkers. He was called ‘the world’s preeminent financial journalist’ by Lawrence Summers. Even Paul Krugman had nice things to say about him.

Which makes us wonder about how much thinking actually goes on in the world.

What we expect from the FT is educated, smart drivel. But, this past weekend brought a shock. An essay in the paper, written by Rushir Sharma of Rockefeller International, was amazingly sharp and clear. (His analysis of what is going on in the US economy agrees with our own.)

Sharma’s blade slices so deeply into FT positions (going back decades) that we wondered if Mr. Wolf had actually read it before putting it in the paper. Maybe he’s on vacation? But there it was, improbably, on the cover of the STYLE section...with a misleading title. Still, it is amazing they ran it at all. Too much government

‘What went wrong with capitalism’, is the headline. FT regular readers must have perked up...like hounds sniffing a rabbit’s scent. They expected the usual claptrap about how the rich got richer and the climate got hotter thanks to the unrelenting greed of capitalists. This critique would inevitably be followed by earnest recommendations, that the government should do this...or do that...to correct the problems.

How disappointed they must have been. Sharma explains that the real problem is that governments have done far too much already. Sharma:

‘The era of small government [which allegedly took place after the Reagan Revolution] never happened. Government has been expanding for nearly a century in virtually all measurable respects, as a spender, borrower and regulator.’

And remember how ‘deregulation’ followed the Reagan administration and was to blame for the financial crisis of 2008? Only, deregulation never happened either. Sharma:

‘During the past three decades, the bureaucracy eliminated a total of just 20 rules, while adding new ones at an almost metronomic pace of about 3,000 a year, under both parties.’

As government expanded, it provided ‘socialism’ for the rich, poor and everyone in between. Sharma:

‘This is a campaign to inoculate an entire society against economic downturns. Although still widely criticized as the land of the Reaganite capital, America is displacing Europe as the society least tolerant of financial distress for anyone, up to and including the super-rich.’

Growth, recession...war...Republicans...Democrats — through good times and bad, the fat years and the lean ones — the feds kept solving more and more problems. Poverty? The threat of communism? Terrorism? Wrong pronouns? Germs? The China trade? Interest rates too high? Jobs? Chips?

Nearly every day for the last century, politicians and bureaucrats have been at work — often into the late hours of night — solving the many problems that afflict our species. It’s amazing that there are any problems left.

So diligent and determined were they to get the job done that they consistently spent more than their tax revenues. Between 1980 and the end of 2019, deficits averaged 4% of GDP in recessions and 3% in recoveries.

So, you see, the problem is not a failure of capitalism at all, but the inevitable overreaching of government and the elites that control it. And now, they’ve given us a new problem to solve — a $35 trillion debt...and an almost guaranteed debt crisis, dead ahead.

Stay tuned for more on what actually went wrong with capitalism. Regards,

Bill Bonner,

For Fat Tail Daily All advice is general advice and has not taken into account your personal circumstances. Please seek independent financial advice regarding your own situation, or if in doubt about the suitability of an investment. |

|

|