|

| The Weekend Edition is pulled from the daily Stansberry Digest. The Digest comes free with a subscription to any of our premium products.

| ||||||||||||

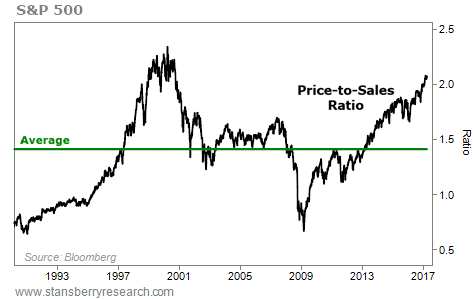

| Stocks are expensive. But we remain cautiously bullish for now. Yes, large-cap U.S. stocks are now trading at higher levels than any other time in history, outside of the Internet bubble. But as Porter explained in the April 7 Digest, valuation alone is not a reason to get bearish…

History shows investors can come up with all kinds of convincing – but ultimately foolish – reasons why "this time is different." For example, in the late 1990s, everyone loved tech stocks. If you were an investor at the time, you may remember people had plenty of reasons why they believed these stocks weren't expensive and could only go higher. Back then, they said profits didn't matter in the "new economy." It was all about "clicks and eyeballs." In the mid-2000s, everyone loved housing… And there were plenty of reasons to buy. "They aren't making any more land," they said. "And home prices never go down." We were reminded of this while reading the Wall Street Journal this week. In an article titled, "This Time Is Different: Two Reasons Not to Be Alarmed by the Nasdaq Record," the authors presented a simple argument…

In other words, tech stocks aren't that expensive because they're still cheaper than they were at the peak of one of the biggest manias in history. How's that for an investment thesis? ----------Recommended Link---------

In recent months, we've shown how default rates for auto loans, student loans, and even high-yield "junk" corporate debt have been quietly ticking higher. Now, we have new evidence that one of the riskiest corners of the credit markets is rolling over, too… This week, Capital One Financial (COF) – one of the country's largest credit-card lenders – reported first-quarter earnings. And they weren't good… The firm reported a stunning 20% year-over-year decline in net income, far worse than analysts had predicted. And it said larger-than-expected credit-card losses were to blame. As the Journal reported…

As they explained in the December 2015 issue, where they warned about the rising risks to credit-card lenders for the first time…

Unfortunately, Capital One's own management team still doesn't appear to understand the magnitude of these problems. More from the Journal (emphasis added)…

As you may know, this is our friend Meb Faber's free weekly podcast. Meb is the co-founder and Chief Investment Officer of Cambria Investment Management, and one of brightest investment minds we know. If you're a fan of Steve's work, you don't want to miss this episode. This wide-ranging conversation covered a ton, including… How Steve got started in finance… what he learned from his worst-ever trade… what Steve is seeing in the investment world today… his latest thoughts on stocks, bonds, housing, and gold… the biggest mistake his subscribers make… and much more. Check it out for yourself right here. You can also learn more about Meb and his podcast at www.MebFaber.com. As regular DailyWealth readers know, Steve is incredibly bullish on China today. But he says there's a new "wrinkle" to the story… In short, three recent changes have "fast tracked" his big China prediction. Steve says this story could play out even quicker than he originally believed possible. On Wednesday, May 3 at 8 p.m. Eastern time, Steve will be going live on-air to explain it all… He'll explain why you're not hearing much about this news in the financial media… why President Trump is "powerless" to stop what's coming… and what this situation means for his "Melt Up" prediction for U.S. stocks. Steve will even give you the name and ticker symbol of one of his favorite China recommendations just for attending. This event is absolutely free for Stansberry Research readers. Simply click here to reserve your spot. Regards, Justin Brill Editor's note: One of the most powerful money groups in the world could soon make an announcement that will dramatically alter your financial future… But only if you play it right. To help you prepare, Steve is holding a free live briefing on Wednesday at 8 p.m. Eastern time. Plus, he's giving away one recommendation to anyone who shows up. Save your spot by clicking here. |

| ||||||||||||||||||||||

| Home | About Us | Resources | Archive | Free Reports | Privacy Policy |

| To unsubscribe from DailyWealth and any associated external offers, click here. Copyright 2017 Stansberry Research. All Rights Reserved. Protected by copyright laws of the United States and international treaties. This e-letter may only be used pursuant to the subscription agreement and any reproduction, copying, or redistribution (electronic or otherwise, including on the world wide web), in whole or in part, is strictly prohibited without the express written permission of Stansberry Research, LLC., 1125 N Charles St, Baltimore, MD 21201 LEGAL DISCLAIMER: This work is based on SEC filings, current events, interviews, corporate press releases, and what we've learned as financial journalists. It may contain errors and you shouldn't make any investment decision based solely on what you read here. It's your money and your responsibility. Stansberry Research expressly forbids its writers from having a financial interest in any security they recommend to our subscribers. And all Stansberry Research (and affiliated companies) employees and agents must wait 24 hours after an initial trade recommendation is published on the Internet, or 72 hours after a direct mail publication is sent, before acting on that recommendation. You're receiving this email at newsletter@newslettercollector.com. If you have any questions about your subscription, or would like to change your email settings, please contact Stansberry Research at (888) 261-2693 Monday – Friday between 9:00 AM and 5:00 PM Eastern Time. Or if calling internationally, please call 443-839-0986. Stansberry Research, 1125 N Charles St, Baltimore, MD 21201, USA. If you wish to contact us, please do not reply to this message but instead go to info@stansberrycustomerservice.com. Replies to this message will not be read or responded to. The law prohibits us from giving individual and personal investment advice. We are unable to respond to emails and phone calls requesting that type of information. |