| This 'Obama Retirement Account' Is Dead – Good Riddance | | By Dr. David Eifrig, editor, Retirement Millionaire | | Tuesday, September 12, 2017 |

| Seventy million dollars... down the drain.

The government wasted a massive amount of money with President Obama's myRA retirement savings account. In late July, the Treasury Department finally shut it down.

Good riddance.

The myRA accounts were structured like Roth IRAs, but with far fewer earnings for savers. The savings in a myRA could only earn the Treasury rate of return, which was extremely low. MyRA investors would have earned around 2% per year since the January 2014 launch.

In the meantime, the S&P 500 stock market index earned more than 40% with dividends reinvested (for 10.4% per year) – more than four times the myRA return.

These accounts simply won't do for folks saving for retirement...

----------Recommended Link---------

---------------------------------

Missing out on the returns of stocks and bonds makes it difficult to build up a nest egg, especially with the constant threat of inflation. The promise was that these accounts could help folks with low incomes get started saving – but apparently they weren't interested.

All told, about 20,000 folks opened myRA accounts... And participants only contributed $34 million. That's right... the government spent $70 million to get folks to save $34 million.

Spending $2 to save $1 never works out in the long run. And another 10,000 folks opened an account and never contributed a dime.

If you did have a myRA, you can roll your assets over to a Roth IRA – a far better choice for retirement savers. Smart IRA and 401(k) decisions can mean the difference between living a comfortable retirement filled with abundance... or just barely getting by in your old age.

If you don't have an IRA or a Roth IRA, you're leaving money on the table...

Opening one is as easy as opening any other brokerage account. You can do it with any broker. I like TD Ameritrade and Fidelity, but I've also heard good things about Interactive Brokers. Of course, we don't have a financial relationship with any broker – we work for you.

When registering, you simply select either a traditional IRA or a Roth IRA as the account type...

| • | A traditional IRA most benefits people who expect to be in a lower tax bracket when they retire than when they are working.

|

| • | A Roth IRA works best for people in the opposite situation. If you expect that your taxes will be higher as a retiree than as a working person, a Roth is perfect for you. |

We often recommend opening both a traditional and a Roth IRA if you are unsure what your tax situation will be in your retirement. That way, you get the benefits of both methods.

Alternatively, a more advanced strategy is to convert a traditional IRA to a Roth. You won't need to pay income taxes on subsequent withdrawals, but you will need to pay a lump-sum tax when you do the conversion. This can get tricky, so we recommend talking with your financial planner about your options.

Opening an IRA will save you tens or even hundreds of thousands of dollars over just a decade or two of retirement savings. That's the real benefit...

When you put money in a traditional IRA, you get a tax deduction for the initial deposit... And the government defers taxes on the money until you withdraw it, typically sometime between ages 59 and a half and 70 and a half.

Deferring taxes saves more than you think...

If there are two people, each with $10,000, and one invests in an IRA while the other invests in a trading account and pays taxes, we can see the power of not paying taxes. After 30 years, the tax-deferred account will be worth $996,964. The taxed account will be worth $791,347. That's more than $200,000 extra just by avoiding taxes.

If you've been on the fence about opening an IRA, it's time to ask yourself one question: "What am I waiting for?"

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig

Editor's note: President Trump is planning a "One-Day Cash Event" that could deliver cash to your mailbox before Thanksgiving. If you had taken advantage of this the last time the government offered it back in 2012, you could have collected separate, one-time payments of $3,620... $2,844... and $1,383... while barely lifting a finger. Get the details here. |

Further Reading:

Back in May, Dave shared five simple tricks you can use to boost your savings. "No matter how skilled you are as an investor," he writes, "upping your savings rate is more powerful to your wealth than either increasing your income or increasing your investment returns." Read more here: Wealth Grows on Its Own... But You Must Plant the Seeds. Dave says the first step to building wealth isn't to increase your income... it's to curb your spending. Get the full story here: The Rich Do Have a Secret. |

|

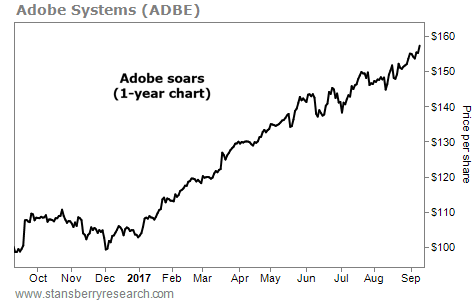

THIS WORLD-CLASS SOFTWARE COMPANY IS BREAKING OUT

Today's chart highlights a leader in the software business... Adobe Systems (ADBE) is a $77 billion computer software giant. The company invented the portable document format, better known as the "PDF." Today, it's one of the most common file types used to exchange information on the web. And its Adobe Acrobat and Reader software are mainstays for viewing and modifying these documents. But Adobe has grown into much more than a PDF company. Two of its other major divisions are its Creativity- and Marketing-Cloud groups. Its Adobe Illustrator and Photoshop applications are extremely popular among graphic designers, architects, and artists. And its Marketing Cloud includes tools businesses use to create and analyze marketing campaigns. Over the past year, Adobe's sales and profits jumped 23% and 68%, respectively. As you can see below, its shares aren't lagging. They're up nearly 60% over the past year... and recently hit a new all-time high. It's a bull market for this tech giant... |

|

| Three steps to make sure you're financially prepared... While you depend on your spouse in certain aspects of day-to-day life, there's no reason to be ignorant of your financial situation... |

Are You a

New Subscriber?

If you have recently subscribed to a Stansberry Research publication and are unsure about why you are receiving the DailyWealth (or any of our other free e-letters), click here for a full explanation... |

|

Advertisement

By investing in these four ideas, you could start turning $500 into $2,070 – or as much as $10,500 – the full story here. |

| Why $6.2 Billion Will Flow Into Alibaba – From Just Two Buyers | | By Dr. Steve Sjuggerud | | Monday, September 11, 2017 |

| | Alibaba trades in the U.S... But it isn't a part of the U.S. benchmark S&P 500 Index because it isn't a U.S. company. So where does it belong? |

| | Gold Just Did This for the First Time Since 2011... Did You Notice? | | By Justin Brill | | Saturday, September 9, 2017 |

| | Gold is quietly leading again... |

| | This Technology Will Upend the Entire Automotive Industry | | By Jeff Brown | | Friday, September 8, 2017 |

| | We are now at the very beginning of this explosive trend, but the potential is enormous... |

| | Profit From the 'Melt Up' and Prepare for the 'Melt Down' | | By Dr. Steve Sjuggerud | | Thursday, September 7, 2017 |

| | What happens after the "Melt Up"? And how do you make money? |

| | What the 'Smart Money' Knows... And the Stock Market Doesn't | | By Porter Stansberry | | Wednesday, September 6, 2017 |

| | We finally have conclusive proof of something we've always believed... |

|

|

|

|