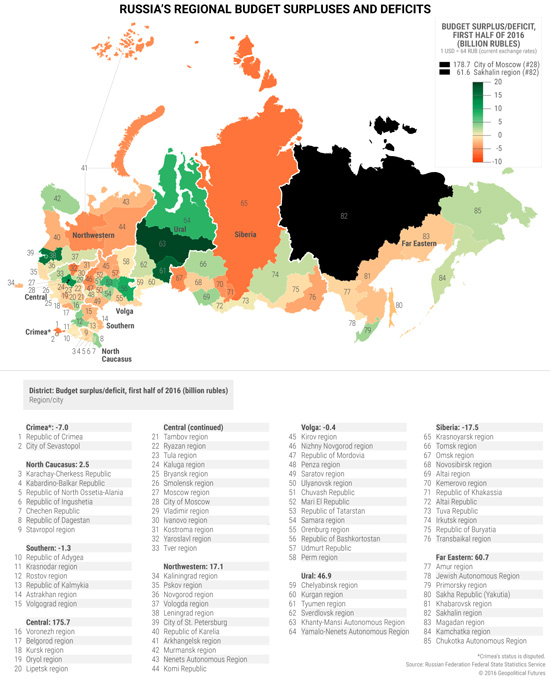

| Forecasting Russia in 2017 Dec 14, 2016 By George Friedman and Jacob L. Shapiro One of the biggest challenges in writing forecasts is clearly communicating our predications for the coming year. There is a certain level of background and analysis that goes into forecasting geopolitics, but often, that background and analysis can serve as either an intellectual crutch or a way of using a lot of words without actually making a call one way or another. That’s why our annual forecasts go through multiple phases of editing. Our forecast for 2017 was published just this week. But our work on the forecast began in early October, with a massive 50-page document filled with questions, research, and findings. This master document was then scrutinized, debated, and whittled down, sharper and sharper… until what was left (hopefully) was a concise description of the world in 2017, as we see it. We aim for accuracy, and as you can see from previous report cards on our work, we are pretty good at what we do. Our full report card for 2016 will be published next week, but in the meantime, subscribers can check out our mid-year evaluation here. But another aim that is almost as important is to be very clear about what we are forecasting. We would rather be wrong and have made a clear forecast than offer a vaguely worded “prediction” that is unfalsifiable. Therefore, we spend less time explaining how we arrived at a given conclusion, and more time clearly stating what we think is going to happen and how that will shape the world. A forecast is not an analysis—it is the culmination of analysis. That means that a certain amount of information about how we arrived at a particular forecast is always left out. If it weren’t, the forecast would read like a volume of Tolstoy, and no matter how brilliant Tolstoy was, his writing style is not well suited for forecasting. So, for the next four or so installments of This Week in Geopolitics, we’re going to take a closer look at some of our most important forecasts for 2017. You can read all of them in our 24-page, subscribers-only report, The World in 2017—yours free of charge if you try a Geopolitical Futures subscription today. To keep things fair for our paid subscribers, we won’t go into great depth on the actual forecasts here—instead, we’ll focus on the analysis and research that led us to some of our most important conclusions. We’ll kick off this series by looking at the current situation in Russia, which we believe is in for a difficult year. Russia’s Military Capability We began the forecasting process with Russia by looking at the country’s military capability. Russia has intervened in Syria to great fanfare, and while it has demonstrated undeniable improvements in some of its capabilities, the Russian military is far weaker than most make it out to be. Our 2016 forecast predicted a frozen conflict in Ukraine, and we came to the conclusion that this frozen conflict will be formalized in 2017 by answering a very basic question: What is the Russian military capability in Ukraine and in general? The answer is found not by looking at events pertaining to the Ukrainian revolution in 2014, but rather the performance of the Russian military in the 2008 Georgia War. Russia achieved all of its strategic objectives in that five-day war, but serious deficiencies in Russian capabilities were revealed. Operational and tactical logistics left much to be desired, as the Russians had serious difficulties maintaining supply lines for food, fuel, and ammunition. Much of Russia’s military equipment was old and falling apart, Russian suppression of enemy air defenses (SEAD) and electronic warfare capabilities were deficient, and use of precision-guided munitions was rare. Joint operational planning between different services was either nonexistent or ineffective. After the war, Russia set out on an ambitious and vast military modernization program, reforming everything from doctrine to training to weapons. Russia set clear goals for reducing the number of conscript soldiers to professionalize the force. The 10-year State Armaments Program, announced by President Vladimir Putin in 2010, allocated 19.4 trillion rubles (worth $698.4 billion at the time) to revamp the equipment and weapons used by the Russian armed forces, and Russia’s military expenditures have been increasing both in absolute terms and as a percent of Russia’s GDP ever since. Russia has taken some impressive steps forward. In 2008, it is unlikely Russia could have fielded a force and deployed it in Syria as it did in 2015. Of all the weapons Russia used in Syria, roughly 20% have been precision-guided munitions, which shows progress… but it also shows how much room Russia has to grow. Russia has deployed unmanned aerial vehicles to help with intelligence gathering, and both SEAD and joint inter-service operations have improved. According to Russian military officials, conscripts in the military have been reduced from roughly 600,000 in 2011, to 200,000 by the end of 2016. These improvements and the media campaign around the Russian intervention, however, obscure the two most important elements to consider in evaluating the Russian military. First, despite these improvements, Russia has neither the military capability nor the political capital to conquer Ukraine, even if it wanted to. Russia beat Georgia because Georgia is a small country and Russia could overwhelm the Georgians with larger numbers. Ukraine is eight times the size of Georgia in terms of total land and can field a much larger infantry force. Many of Russia’s Rapid Reaction Forces that would be mobilized in such an action still consist of significant numbers of conscripts. Even if Russia could blitz its way to Kiev, it couldn’t hold the country, considering the long supply lines and Ukraine’s large, hostile population. And if the US or NATO decided to intervene, Russia would require even greater forces. Second, Putin and the Russian government are aware of these limitations. Since 2008, they have been doing everything possible to modernize the Russian armed forces and to reach, if not parity, then a level of strength that could give them more strategic options. That has meant increasing military spending. While Russia was flush with oil money, that was a perfectly logical plan. But Russia was not expecting oil prices to collapse in 2014. Russia had planned a budget on the then-conservative estimate that oil wouldn’t fall below $82 a barrel. Oil has averaged between $34 and $35 a barrel in 2016, and there’s no reason to expect the oversupplied market to give Russia significant relief in the coming year. Modernizing Russia’s forces is one of the top priorities for the government in the next three years, but it’s not clear if Russia has the money to spend. The Russian Economy The main issue for Russia in 2017 is not going to be a military one. Russia does not want to get bogged down in Syria, so it will be looking to extricate itself from that conflict. Russia cannot fix its Ukraine problem through force, so it will try to reach a settlement that will allow the status quo to remain in place. As long as Kiev remains neutral and not a basing point for major US and NATO assets, the Russians will be content, though uncomfortable. The problem for Russia is that its economy is in a shambles, and it is trying to pour money into modernizing the military at the same time that disturbing cracks in the Russian economy are beginning to show. Let’s look at two graphics that demonstrate just how challenging the current situation is.  This is a simple chart of the exchange rate between the ruble and the dollar in the last five years. Since July 2014, the ruble has lost almost 50% of its value. In 2010, Putin promised to spend 19 trillion rubles on upgrading the Russian military, which was equivalent to almost $700 billion at the time. Today, 19 trillion rubles is worth only $303 billion. Real wages have been declining since 2014. Inflation, at this time last year, was almost 13%, and though it has stabilized around 6% in recent months, the ruble is still under a lot of pressure.  This graphic shows the current state of Russia’s regional budgets, and the picture is not pretty. Major oil-producing regions as well as Moscow are doing all right, but large swaths of the rest of the country are running regional deficits. The central government in Moscow is also struggling, reportedly cutting all federal ministry budgets by 10%. While spokesmen in Russia’s Defense Ministry have said that defense spending will be cut by 5%, this is impossible to confirm because some parts of the Russian budget are classified and those defense expenses are likely hidden. Russia’s Ministry of Finance says that Russia’s Reserve Fund (which totaled 28.6 billion rubles in 2008) will be fully spent by the end of 2017 and that the country will start dipping into its National Wealth Fund to cover its budget deficits. In addition to these larger indicators, we have seen disturbing smaller indicators of a struggling economy. A few weeks ago, protests occurred in one oil-producing region in Ural Federal District due to economic dissatisfaction, and in another region due to unpaid wages and malfunctioning heating equipment shortly before winter came in earnest. Russia has been shutting down banks at an increasing rate and blaming them for irresponsible lending practices. This has prompted over 2.7 million more people to apply for deposit insurance in the last five years than the previous five years, which could be a sign that the banking sector is under severe pressure. The Forecast These are the basic building blocks, and once they were identified, the forecast essentially wrote itself. Having defined Russian military capabilities, we were able to identify Russia’s political and strategic objectives in Ukraine, Syria, and elsewhere in the year ahead. You’ll read in detail in The World in 2017: - Why the International Monetary Fund is wrong predicting that the country is on the upswing

- The trends that are telling us the Russian economy hasn’t yet hit rock bottom

- Two economic challenges that could push Russians over the edge… and contribute to the country’s collapse by 2040

- What it all means for Russia’s international relationships and actions in the year ahead

- How these events will affect other key players on the world stage in 2017—and why you need to know about it

You’ll get this must-read, 24-page forecast report as a free thank-you gift if you agree to a subscription to Geopolitical Futures today.

George Friedman

Editor, This Week in Geopolitics

| Prepare Yourself for Tomorrow with George Friedman’s This Week in Geopolitics

This riveting weekly newsletter by global-intelligence guru George Friedman gives you an in-depth view of the hidden forces that drive world events and markets. You’ll learn that economic trends, social upheaval, stock market cycles, and more... are all connected to powerful geopolitical currents that most of us aren’t even aware of. Get This Week in Geopolitics free in your inbox every Monday. |

Share this newsletter

Not a subscriber?

Click here to receive free weekly emails from This Week in Geopolitics.

Use of this content, the Mauldin Economics website, and related sites and applications is provided under the Mauldin Economics Terms & Conditions of Use. Unauthorized Disclosure Prohibited The information provided in this publication is private, privileged, and confidential information, licensed for your sole individual use as a subscriber. Mauldin Economics reserves all rights to the content of this publication and related materials. Forwarding, copying, disseminating, or distributing this report in whole or in part, including substantial quotation of any portion the publication or any release of specific investment recommendations, is strictly prohibited.

Participation in such activity is grounds for immediate termination of all subscriptions of registered subscribers deemed to be involved at Mauldin Economics’ sole discretion, may violate the copyright laws of the United States, and may subject the violator to legal prosecution. Mauldin Economics reserves the right to monitor the use of this publication without disclosure by any electronic means it deems necessary and may change those means without notice at any time. If you have received this publication and are not the intended subscriber, please contact service@mauldineconomics.com. Disclaimers The Mauldin Economics website, Yield Shark, Thoughts from the Frontline, Patrick Cox’s Tech Digest, Outside the Box, Over My Shoulder, World Money Analyst, Street Freak, Just One Trade, Transformational Technology Alert, Rational Bear, The 10th Man, Connecting the Dots, This Week in Geopolitics, Stray Reflections, and Conversations are published by Mauldin Economics, LLC. Information contained in such publications is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The information contained in such publications is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. The information in such publications may become outdated and there is no obligation to update any such information. You are advised to discuss with your financial advisers your investment options and whether any investment is suitable for your specific needs prior to making any investments.

John Mauldin, Mauldin Economics, LLC and other entities in which he has an interest, employees, officers, family, and associates may from time to time have positions in the securities or commodities covered in these publications or web site. Corporate policies are in effect that attempt to avoid potential conflicts of interest and resolve conflicts of interest that do arise in a timely fashion.

Mauldin Economics, LLC reserves the right to cancel any subscription at any time, and if it does so it will promptly refund to the subscriber the amount of the subscription payment previously received relating to the remaining subscription period. Cancellation of a subscription may result from any unauthorized use or reproduction or rebroadcast of any Mauldin Economics publication or website, any infringement or misappropriation of Mauldin Economics, LLC’s proprietary rights, or any other reason determined in the sole discretion of Mauldin Economics, LLC. Affiliate Notice Mauldin Economics has affiliate agreements in place that may include fee sharing. If you have a website or newsletter and would like to be considered for inclusion in the Mauldin Economics affiliate program, please go to http://affiliates.pubrm.net/signup/me. Likewise, from time to time Mauldin Economics may engage in affiliate programs offered by other companies, though corporate policy firmly dictates that such agreements will have no influence on any product or service recommendations, nor alter the pricing that would otherwise be available in absence of such an agreement. As always, it is important that you do your own due diligence before transacting any business with any firm, for any product or service. © Copyright 2016 Mauldin Economics |