| -- | June 12, 2017 US Oil Production Makes Waves By George Friedman and Jacob L. Shapiro There’s no end in sight to slumping oil prices—good news for consumers but a dire development for major oil producers like Saudi Arabia and Russia. And now, rising US oil production and exports are contributing to the slump. Last week, oil prices reached new lows for 2017, with Brent crude dipping below $48 per barrel and West Texas Intermediate dipping below $46. The drop has been attributed to an unexpected increase in US crude inventories, which rose by 3.3 million barrels last week (according to the US Energy Information Administration), despite expectations that it would drop by 3.5 million barrels. The rise in production is compounded by rising US oil exports, since the US lifted a 40-year ban on these exports in 2015. This led to modest increases in oil exports in 2016 but substantial increases so far in 2017. This is a key reason prices will remain low in the long term. Ebbs and Flows in US Exports It is worth remembering why the United States banned oil exports in 1975 (exceptions were allowed at the discretion of the president). 1970 set a record for the highest crude oil production in the US, though this record will likely be broken in the next two years. The US was producing a lot, but it was also consuming a lot, forcing it to import more from OPEC states, which produced about 55% of the world’s oil in 1973. This meant that OPEC could essentially control prices. And after the US backed Israel in the 1973 Yom Kippur War, OPEC retaliated by raising oil prices. This created a fourfold jump in prices and a global oil shock. One of the many ways the US responded was the 1975 Energy Policy and Conservation Act. This was designed to decrease its reliance on imports by banning oil exports, ensuring US-produced oil would only be consumed domestically.

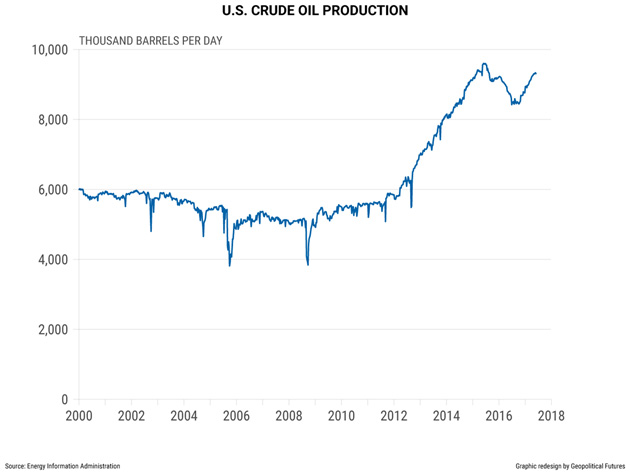

Click to enlarge Fast-forward to today, and supply is no longer as big a concern. The US has weaned itself off foreign oil, partly through technologies like hydraulic fracturing and horizontal drilling. In 2013, the US started producing more oil than it imported, and it hasn’t looked back. US crude oil production has almost doubled since 2010 and is already surpassing forecasts for 2017. In late 2016, the US Energy Information Administration estimated that the United States would produce 8.7 million barrels per day on average in 2017. New estimates suggest it will produce 9.2 million barrels per day in 2017 and up to 10 million barrels per day in 2018.

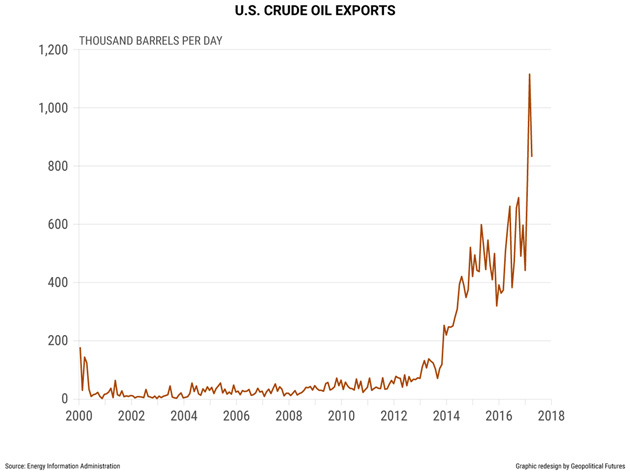

Click to enlarge But it’s not just the US production numbers that are making waves: It’s the spike in US crude oil exports. The US exported 830,000 barrels of crude per day in March, a whopping 64.2% increase year over year. In February, it exported 1.1 million barrels per day, a nearly 200% increase year over year. According to The Wall Street Journal, the February numbers are closer to the new norm, as it expects the US to export, on average, roughly 1 million barrels per day in 2017. A Disaster for Oil Producers This is a huge challenge for major oil producers, especially Saudi Arabia and Russia. In December 2016, OPEC and its oil-producing partners agreed to cut production by about 1.8 million barrels per day, or roughly 1.5% of global crude production at the time. OPEC, led by the Saudis, has largely made good on this pledge, reducing production by 1.1 million barrels per day in the first quarter of 2017. The Russians have played with the numbers cutting production compared with December 2016 levels but not in year-over-year terms. The OPEC deal managed to stabilize oil prices around $50 per barrel, and last month the cuts were extended for another nine months. If it were still 1973, that might have caused a jump in oil prices. But in 2017, OPEC produces only about 40% of the global supply, and the US is among the top three producers in the world. The price of Brent crude spiked to $54.15 per barrel after the cuts were extended but has since dropped almost 12% and may continue to fall.

Click to enlarge This means that even the combined forces of OPEC and non-OPEC producers can’t prop up oil prices unless they are willing to slash production more severely. It also means that there is enough oil on the market, partly from the US, to satisfy demand, even when major producers limit their supply. Maintaining prices at current levels is the best outcome these producers can hope for. But even this comes with the downside of losing market share to competitors, without getting oil prices back to the levels that Russia and Saudi Arabia would need to stabilize their economies.

Click to enlarge When we discuss US power in the world, we often trot out a few key points: The US economy accounts for just under a quarter of global gross domestic product; it has a military force without peer in the world; and its economy is not dependent on exports. We can now add the following points to this list: The US is the third-largest oil producer in the world; it is less dependent on oil imports than at any point in the last 40 years; and it is stealing customers from Russia and Saudi Arabia even with prices as low as $50 per barrel. Even a few years ago, US shale producers would have found it hard to make a profit at that price, but they are succeeding at that now. Oil prices are going down, US oil exports are going up, and the ramifications will be global.

George Friedman

Editor, This Week in Geopolitics

| Prepare Yourself for Tomorrow with George Friedman’s This Week in Geopolitics

This riveting weekly newsletter by global-intelligence guru George Friedman gives you an in-depth view of the hidden forces that drive world events and markets. You’ll learn that economic trends, social upheaval, stock market cycles, and more... are all connected to powerful geopolitical currents that most of us aren’t even aware of. Get This Week in Geopolitics free in your inbox every Monday. |

Share Your Thoughts on This Article

Not a subscriber?

Click here to receive free weekly emails from This Week in Geopolitics.

Use of this content, the Mauldin Economics website, and related sites and applications is provided under the Mauldin Economics Terms & Conditions of Use. Unauthorized Disclosure Prohibited The information provided in this publication is private, privileged, and confidential information, licensed for your sole individual use as a subscriber. Mauldin Economics reserves all rights to the content of this publication and related materials. Forwarding, copying, disseminating, or distributing this report in whole or in part, including substantial quotation of any portion the publication or any release of specific investment recommendations, is strictly prohibited.

Participation in such activity is grounds for immediate termination of all subscriptions of registered subscribers deemed to be involved at Mauldin Economics’ sole discretion, may violate the copyright laws of the United States, and may subject the violator to legal prosecution. Mauldin Economics reserves the right to monitor the use of this publication without disclosure by any electronic means it deems necessary and may change those means without notice at any time. If you have received this publication and are not the intended subscriber, please contact service@mauldineconomics.com. Disclaimers The Mauldin Economics website, Yield Shark, Thoughts from the Frontline, Patrick Cox’s Tech Digest, Outside the Box, Over My Shoulder, World Money Analyst, Street Freak, Just One Trade, Transformational Technology Alert, Rational Bear, The 10th Man, Connecting the Dots, This Week in Geopolitics, Stray Reflections, and Conversations are published by Mauldin Economics, LLC. Information contained in such publications is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The information contained in such publications is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. The information in such publications may become outdated and there is no obligation to update any such information. You are advised to discuss with your financi al advisers your investment options and whether any investment is suitable for your specific needs prior to making any investments.

John Mauldin, Mauldin Economics, LLC and other entities in which he has an interest, employees, officers, family, and associates may from time to time have positions in the securities or commodities covered in these publications or web site. Corporate policies are in effect that attempt to avoid potential conflicts of interest and resolve conflicts of interest that do arise in a timely fashion.

Mauldin Economics, LLC reserves the right to cancel any subscription at any time, and if it does so it will promptly refund to the subscriber the amount of the subscription payment previously received relating to the remaining subscription period. Cancellation of a subscription may result from any unauthorized use or reproduction or rebroadcast of any Mauldin Economics publication or website, any infringement or misappropriation of Mauldin Economics, LLC’s proprietary rights, or any other reason determined in the sole discretion of Mauldin Economics, LLC. Affiliate Notice Mauldin Economics has affiliate agreements in place that may include fee sharing. If you have a website or newsletter and would like to be considered for inclusion in the Mauldin Economics affiliate program, please go to http://affiliates.ggcpublishing.com/. Likewise, from time to time Mauldin Economics may engage in affiliate programs offered by other companies, though corporate policy firmly dictates that such agreements will have no influence on any product or service recommendations, nor alter the pricing that would otherwise be available in absence of such an agreement. As always, it is important that you do your own due diligence before transacting any business with any firm, for any product or service. © Copyright 2017 Mauldin Economics | -- |