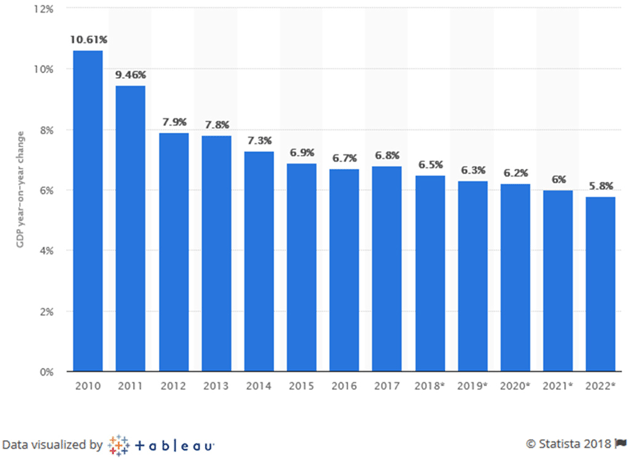

Chinese Growth Spurt By John Mauldin | Sep 15, 2018 Economic reality isn’t black and white. At any given time, both good things and bad things are happening. Ignoring one side because it doesn’t fit your preferred outlook is an excellent way to go badly wrong. So it is with China. We hear a lot about that vast country’s problems and challenges. They are very real and could have major consequences... which we will explore soon… but there’s good news, too. We reviewed some of it last week in China’s Command Innovation. Today, we’ll add a few more positive data points. This letter will be a little different than most. Below you’ll read several short vignettes about positive events in China. They aren’t necessarily related and won’t build to any particular conclusion. My goal is simply to demonstrate that China has good news, and even some fabulously great news, much of it quite compelling. Whether it is enough to overcome the challenges is a different question we will address next time. And frankly, the manner in which they are growing clearly makes Western countries uncomfortable, as it is not our usual playground. First, a quick aside. We have been making an aggressive effort to keep the main body of this letter around 3,000 words, a length most people can read in a few minutes. We’ve had good feedback on it, too. Then in my personal section, I share a great story from Art Cashin from last Monday night. So you can read either part of this letter, or both, as you wish. Now on with our China story. Here in the US we are very excited at the prospect of seeing 3% real GDP growth this year. In China, that would represent an unprecedented crash. Here are the annual changes from 2010-2017, with IMF forecasts for 2018-2022.

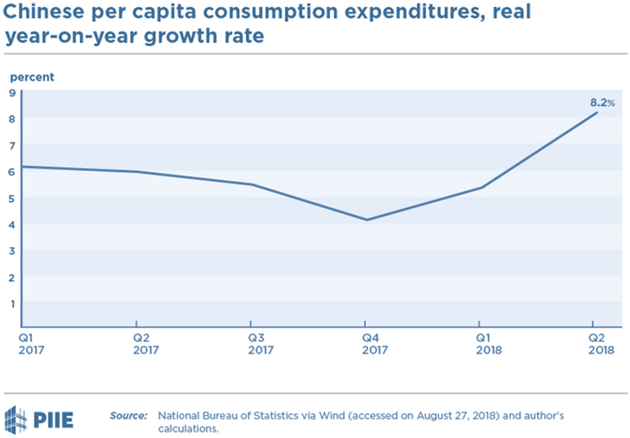

Source: Statista Now, you can fairly ask how reliable this data is. The numbers have a curious way of coming in at exactly the level Beijing expects. But I have no doubt that Chinese growth is far greater than the US or any other developed country has seen in the last decade. And I think the IMF is probably right that it will decline only gradually and remain impressive, by Western standards, well into the 2020s. Much, if not most, of this growth is debt driven, and eventually that debt has to come home to roost. But that doesn’t seem to bother them currently. Yet I constantly hear predictions that China’s growth days are over. Often, this stems from a belief that China’s capital investment has been higher than it actually is, leaving excess capacity. And in some industries that is true—like steel production—but steel factories have been shutting down left and right. Axios reported recently: By the end of the year, some 1.8 million Chinese coal and steel workers will lose their jobs, victims of the government's shift to cleaner industries and a shutdown of small enterprises. To put that in perspective, the two industries employ just 192,000 workers in the US. That is in addition to the millions of coal and steel workers who have already lost their jobs in the last 15 years. The Chinese are ruthlessly eliminating excess capacity. Peterson Institute economist Nicholas Lardy argued last month that most of the “investment growth” we hear about is simply higher prices and real investment barely grew. If so, China may have less spare capacity than we think. In a follow-up article, Lardy further explained that personal consumption data—which is much harder to manipulate—is more in line with economic growth. He says this is more meaningful than retail spending since China’s fast-growing middle class spends much of its income on services like education and healthcare.

Source: Peterson Institute If investment and consumption are both strong, as they appear to be, then the remaining threat to GDP growth would be falling exports. Trade tension might eventually bring that on, but it hasn’t happened yet and China is already working to replace any lost US sales. I’ve talked before about Alibaba (BABA), China’s e-commerce juggernaut that is, if possible, even more dominant than Amazon.com (AMZN). One big question for both companies is how far outside their home countries they can expand. Alibaba took a big step in that direction last week. On the sidelines of a Xi Jinping-Vladimir Putin summit in Vladivostok, Alibaba said it was buying a 10% stake in Russian internet giant Mail.Ru Group. They plan to use the latter’s Russian social networks to build an e-commerce platform. Aside from the benefits it brings to both companies, the platform will be a new conduit for Chinese exports to Russia.

Source: Wall Street Journal Now, it will be a long time before Russian consumers buy enough online goods to replace what China will lose in US exports if the trade war heats up further. The broader point is that Chinese businesses are not at the mercy of US trade policy. They have other options and are actively pursuing them. Combine this with China’s massive “One Belt, One Road” infrastructure initiative, and you can see where the game is going. Alibaba, Tencent, and Baidu will be following the yellow brick, I mean One Belt, One Road, as will other big Chinese companies. Beijing intends to dominate as much of the Asian economy as it can. North America and Western Europe aren’t going anywhere but we aren’t the world’s growth centers anymore. Perhaps strangely, that thought doesn’t bother me. Who’s afraid of a little competition? I think we will do just fine, thank you very much. Artificial Intelligence, or AI, is the new Space Race. This time the US faces China instead of the Soviet Union and the outcome is not nearly as certain. Beijing wants to win and is pouring resources into doing it. A new book, AI Superpowers by Kai-Fu Lee, is a must-read assessment of this battlefield. My friend Peter Diamandis recently shared Lee’s concept of “Four Waves” in AI development. Chinese companies are giving Silicon Valley a run for its money. First Wave: Internet AI. These are the now-ubiquitous online “recommendation engines,” like the products Amazon says you should want, or the “suggested videos” that keep you on YouTube for hours. Those recommendations come from the data we generate with our clicks and other online activity. Lee thinks China’s data advantage gives it a slight lead over US counterparts in this segment. Second Wave: Business AI. This is where we see computers analyzing data to make judgements once reserved for humans: loan underwriting, cancer diagnoses, and so on. AI excels in considering far-flung datapoints that a human analyst would discount or miss completely. Lee says the US has a commanding lead for now but China’s lag may actually help by letting it leapfrog over legacy technologies. The country went straight from cash to mobile payments, for instance, bypassing the clunky credit card apparatus we have difficulty abandoning. Third Wave: Perception AI. You’ve heard about the Internet of Things. The devices around us, once connected to each other, will merge the physical and online environments into one seamless world. China has the lead in sensor technology and is already using it in factories, retailing, and law enforcement. Already they have stores where you literally scan your face to pay the bill. No card, no device, just the face that’s always with you. That’s where we are all going and China is going there first. Fourth Wave: Autonomous AI. Machines that can both make decisions and sense the world around them will eventually operate independently. Autonomous vehicles are the most familiar example but it won’t end there. Imagine drone swarms extinguishing forest fires or painting your house. Chinese scientists are working on such things. These are controversial and sometimes risky capabilities. They will face opposition in the US but less so in China, if that is what the government wants. Hence, I think China will probably gain the lead and possibly hold it for a long time. Even without AI, Chinese manufacturers are automating fast. This is partly out of necessity: the country lacks skilled workers, especially young ones who can work long hours. Competition from lower-cost Asian neighbors makes raising wages difficult. The best answer is to get more efficient via automation. Increasingly, the same companies that once thrived by reverse-engineering and copying Western goods are building their own advanced products. The government’s “Made in China 2025” initiative helps with generous loans and subsidies. For instance, The Wall Street Journal recently profiled a heavy machinery maker called Sany Group. Among other things, Sany makes the pump trucks that blast cement to the top of tall buildings, plus cranes and other equipment.

Source: Sany Global It turns out, some 380,000 Sany-built construction machines are connected to the internet and constantly send data back to their maker. The company uses it to design better products, constantly adjusting production on the fly. That’s possible because the workers are robots who just need new software instructions, not lengthy retraining. US and European companies make the same kind of equipment, of course. I suspect the quality is more than equal or better. Their problem is that even if a trade deal gives them full access to China, manufacturers like Sany are already way ahead, they don’t have shipping costs, and foreigners don’t get the kind of help from their governments that Sany gets from Beijing. Now multiply this by thousands of other companies in many industries. Many are fully capable of competing anywhere on the globe, but they don’t have to. They have a giant market right there at home. This next section comes from this short video on Facebook about some of China’s bright spots you might not know about. (The Science Nature Page has scores of other interesting videos, too, by the way.) - China has recently become the world’s largest solar power producer.

- China is pouring $364 billion into renewable power generation.

- At least 40 hospitals in China have deployed IBM’s Watson AI technology.

- They are rolling out AI to improve healthcare and diagnoses at a prodigious rate.

- Chinese scientists have invented rice that can grow in saltwater that will be able to feed over 200 million people. That will be a big deal.

- At least 1 million Chinese could be using 5G mobile networks by 2023.

- Most Chinese consumers are now using mobile payments instead of cash, even at local street vendors. That means Tencent knows your buying habits even down to the type of noodles you like. And again, the Chinese seemingly don’t care others have that data.

- I don’t think they will beat Bezos or Musk or Allen to the moon, but China is teaming up with Europe to build a base on the moon. They are serious about it.

- They just built the world’s largest telescope to study the universe. Basic research is the font from which new ideas and businesses grow.

- The use of robots in China is growing at a prodigious rate. They actually have fully unmanned factories.

- (A personal sore point): China will begin work on the world’s largest supercollider in 2020. It will be twice the size of the current Hadron collider. The US poured billions into what would’ve been the world’s largest superconducting supercollider south of Dallas. After digging the holes and tunnels, Congress decided it was wasted money and walked away.

- China has the largest network of bullet trains in the world and they are expanding it to include all of those super cities I mentioned above.

- China allows genetically modifying human embryos and stem cells, and will soon catch up with the research we have been doing in the US and Europe. Especially since we publish everything we do.

- Rather than keeping things in the lab, the country allows CRISPR gene editing on humans. I can imagine all sorts of things that will go awry and it makes me cringe to use humans as guinea pigs, but it will speed up the invention of treatments for all sorts of diseases. And that’s a good thing for humanity. (Note: I think we should speed up the process but there still should be guidelines on gene editing in humans. Too much can go wrong.)

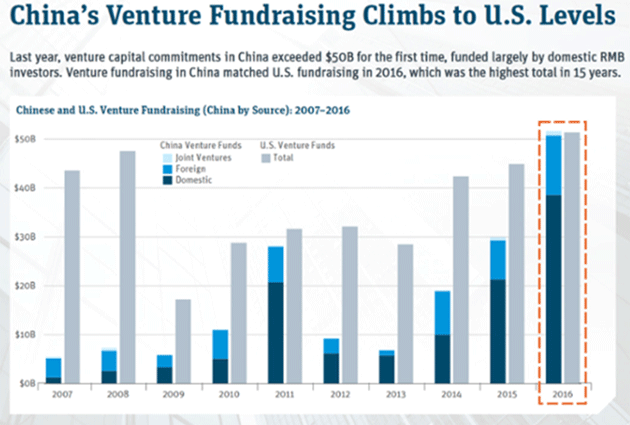

For years, China basically locked out certain US companies and let Chinese companies “copycat” foreign technology, often ignoring patents and ideas and so forth. It was a free-for-all but created Chinese “champions” in many industries. Think Baidu (tech holding company and second-largest search engine), Alibaba Group (huge diversified holding company—comparable to Amazon), Tencent (tech, internet, gaming, etc.), Xiaomi (phones and electronics). Of course, now hundreds of American companies operate in China, but the Chinese government has a ring fence around certain segments. That’s one reason China has nine of the world’s top 20 tech companies. And now these companies are taking that local profit, creating state-of-the-art and often leading technology and using it to go global. I showed this chart last week. Chinese venture capital is now over $50 billion and roughly at the US level.

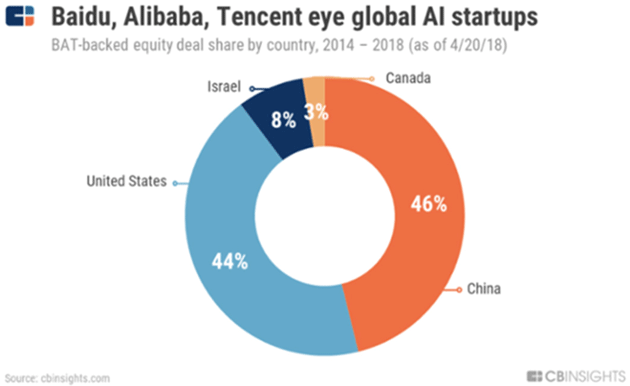

Source: VentureBeat This from my friend Peter Diamandis: This astounding growth is part of China’s explosion in private equity. Currently, almost 16,000 limited partners have disclosed investments in private equity and VC funds totaling 6.1 trillion RMB. But while many of these funds used to be poured into thousands of Chinese copycat companies and local tech startups, we’re seeing a dramatic outward shift in China’s biggest investments. Let’s take a look at BAT-backed startups, for instance.

Source: CB Insights As Baidu, Alibaba, and Tencent take on global leadership in AI, autonomous vehicles, and personalized medicine, China’s corporate VC targets are getting an even split between China and the rest of the world. And this is just the VC expenditures of three companies, albeit big ones. Other Chinese corporations or state-owned enterprises (SOEs) are also pouring money into acquisitions and venture capital. They are all creating new technologies and buying whatever they need to compete, and they are all going to follow the One Belt, One Road as they expand. Count on it. China is a growing competitive force and the rest of the world needs to step up its game. This is good from a strictly human perspective. Competition makes everybody improve their services and products. We believe that for US companies but it’s true on a world scale as well. Do we have to like it? No. Nobody really likes having to compete aggressively in what they believe is “their” space, but that is reality now. And by the way, don’t dismiss South American or other Asian countries. I think over time we will see African companies competing at a high level as well. The world is going to look very different in 20 years. An idea is circulating that the US should somehow rein in Xi’s and China’s drive for technological superiority. That is silly. First, it can’t be done; China won’t (and arguably can’t) stop progressing. Furthermore, if the US and other Western countries want to remain technologically superior, they need to devote resources to making that happen. As we saw last week, China now has more research, more scientists and engineers, and more capital. We are choosing to let that happen. There is no reason China necessarily will surpass the West in technology, in artificial intelligence, autonomous cars, and a host of other technologies. We had an enormous advantage, but we have not kept up our drive. We call our entrepreneurs before congressional hearings to ask how they spend their capital, etc. We want to regulate one business initiative after another. We worry about monopolies. Cries to break up Amazon are part of that absurdity. Consider what Chinese companies do with customer data. The average Westerner would blanch, maybe even run hysterically to their government, complaining about invasion of privacy. Most Chinese consumer purchases are on a small number of mobile systems like Tencent or Alibaba, which are using that data to improve and, admittedly, make more money. And you know what? The average Chinese person doesn’t care. That is just a foreign (literally) concept to the West and especially the US. It offends our notions of privacy. Here is what you have to understand. Less than 40 years ago, most Chinese people lived at subsistence level, following an ox in a rice paddy, or its equivalent. Now they are living in megacities. They didn’t develop our Western privacy sensibilities over centuries as we did. This is all brand-new to them. They don’t understand why we would do it differently. Consider the vast cultural differences and leave your Western thinking behind when you try to understand China. And with that, we will leave our bullish story behind, realizing that one could easily write several books about all the great things going on in China. I’m in Houston tonight (Thursday) for a meeting at Rice University and dinner with the RISE committee (The Rice Initiative for the Study of Economics). This is an extraordinarily interesting group of people and it gives me a chance to get back to my old college stomping grounds. I will do some more business meetings Friday morning before I fly home in the early afternoon. I also know that I will have to make a few currently unplanned trips over the next month. The next actual trip I have scheduled is to Frankfurt in early November, and I know that Shane and I will have to get back to Puerto Rico at some point very soon. The schedule does seem to fill up. I will be doing two presentations in Dallas on October 4 (my 69th birthday) at the Dallas Money Show, which is at the Hyatt Regency Dallas. Normally when I have a dinner with Art Cashin the table gets crowded, and the conversations can get animated. Last Monday we went to the Friends of Fermentation gathering at Bobby Vans right next to the exchange. It wasn’t the usual group—just six of us in a private room. I found it special because two of the six had never met Art or heard his stories. And while we talked a little bit about the markets, I got us started and then the others chimed in with questions. Art held court, telling one story after another, many that I had never heard. Barry Habib had the presence of mind to pull out his phone and record it all, and Art, never camera shy, just stayed on his roll. They were all great but one stood out as I was talking with Ben Hunt and Steve Blumenthal the next morning. Art’s father died just as he graduated from high school, and he had to go to work. He was applying here and there and his uncle, who was a bartender, was looking rather pensive and one of his clients asked, “What’s the matter?” He explained about Art’s situation. The bartender wrote a name on a card, handed it to Art and said, “Go see this man at the stock exchange.” So Art took that card and went to the exchange (and I’m skipping a bunch of the story about how he negotiated to get on the floor where the action is rather than in the back room) and agreed to work for $75 a week. Art had one other interview lined up that kept raising the amount of money that they would pay until he got $115 a week, his own office and a secretary. It was for a brand-new mutual fund. Art called the original company back and told them of the competing offer and the partner at the firm said, “Son, this is Wall Street. Your word is your bond. If you want to work here you better remember that. Are you coming to work at the price we offered?” Art hung up, thought about it and called back to say he would be there Monday to work at $75 a week. Art decided that his word was his bond. Five years later, at 23 years old, Art had his own seat on the exchange, one of the youngest members. Twenty-five years later he was the sheriff of the exchange, a story I’ve told before. The next day we talked and I encouraged him to write his memoirs, as he has seen 50 years at the exchange and the era is ending. Today, it is not much more than a TV set for CNBC. It’s sad in a way, but 90% of NYSE stocks are traded off-exchange already. They could close the exchange and nothing would happen. If you know or ever meet Art, bug him about writing his memoirs. I guarantee you it will be a bestseller. And one you want to get. It’s time to hit the send button. You have a great week! And get together with some friends and swap a few stories. We all have them. I look forward to meeting you someday and hearing your stories. Your nostalgic-but-still-looking-to-the-future analyst,   | John Mauldin

Chairman, Mauldin Economics |

P.S. Want even more great analysis from my worldwide network? With Over My Shoulder you'll see some of the exclusive economic research that goes into my letters. Click here to learn more.     | | Share Your Thoughts on This Article | | |

|