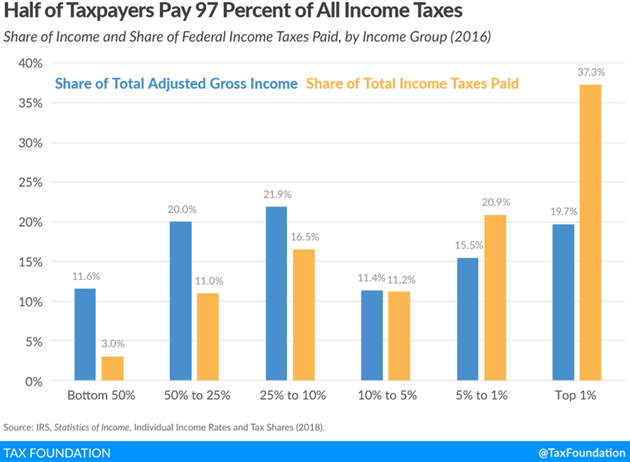

Ray Dalio Is Kinda, Sorta, Really Wrong, Part 3 By John Mauldin | Jun 22, 2019  Two weeks ago I started a mini-series in the form of an open letter responding to a series of essays by Ray Dalio, the founder of Bridgewater Associates. I wrote here and here that he was kinda, sorta wrong in Why and How Capitalism Needs to Be Reformed, Parts 1 and 2 but really, really wrong in It’s Time to Look More Carefully at ‘Monetary Policy 3 (MP3)’ and ‘Modern Monetary Theory,’ in which he basically endorsed MMT. Today I continue my response. If reader feedback is any indication, you are also passionate about this conversation. Last week’s letter generated many long, thoughtful reader comments. Clearly, it is not just Ray and I who are worried about the country’s future direction. I find that encouraging. A national conversation is precisely what we need in these serious times. As noted, Ray has done us all a service by pointing out some rarely mentioned elephants in the room (some tinged with pink). We discuss various parts but seldom the entire creature. By that, I mean the rapidly growing potential for “progressive” control of both Congress and the White House. This stems from differences between haves and have-nots, between the protected and unprotected, combined with a desire to have government solve our society’s perceived ills. So let’s pick up where we left off last week. In Part 1 of this letter I mostly agreed with you about the significant wealth and income disparities in the US today. And then in looking for your hope of a bipartisan commission that can deal with the problems, I simply pointed out that such commissions have rarely worked in the past and would be even more unworkable given today’s partisan, ideological divide. Now I want to review two of your suggested solutions. Since this is an open letter and others will be reading it, let me quote directly from that section: 1. Leadership from the top. I have a principle that you will not effect change unless you affect the people who have their hands on the levers of power so that they move them to change things the way you want them to change. So there need to be powerful forces from the top of the country that proclaim the income/wealth/opportunity gap to be a national emergency and take on the responsibility for reengineering the system so that it works better. 4. Redistribution of resources that will improve both the well-beings and the productivities of the vast majority of people. As an economic engineer, naturally I think about how money might be obtained from taxes, borrowing, businesses, and philanthropy, and how it would flow to affect prices and economies. For example, I think about how a change in personal tax rates might occur and how changes in them relative to corporate tax rates would affect how money would flow, and how changes in tax rates in one location relative to another location would drive flows and outcomes in them. I also think a lot about how the money raised will be spent—e.g., how much will be spent on programs that will improve both social and economic outcomes, and how much will be redistributive. Such decisions would of course be up to the people on the bipartisan commission and the leadership to decide and are way too complicated an engineering exercise for me to opine on here. I can, however, give my big picture inclinations. Above all else, I’d want to achieve good double bottom line results. To do that I’d: b. Raise money in ways that both improve conditions and improve the economy’s productivity by taking into consideration the all-in costs for the society (e.g., I’d tax pollution and various causes of bad health that have sizable economic costs for the society). c. Raise more from the top via taxes that would be engineered to not have disruptive effects on productivity and that would be earmarked to help those in the middle and the bottom primarily in ways that also improve the economy’s overall level of productivity, so that the spending on these programs is largely paid for by the cost savings and income improvements that they create. Having said that, I also believe that the society has to establish minimum standards of healthcare and education that are provided to those who are unable to take care of themselves. Let me highlight in particular one sentence from the above with my own bolded emphasis. So there need to be powerful forces from the top of the country that proclaim the income/wealth/opportunity gap to be a national emergency and take on the responsibility for reengineering the system so that it works better. First, let’s ignore the fact that many would not agree that the income and wealth gaps rise to the level of “national emergency.” Let’s for the moment assume the levers of power you mention would pass to a majority who would in fact see it that way and want to do something about it. Using suppositions and hypotheticals, this is not all that far-fetched. It is entirely possible next year’s elections will deliver a Democratic Congress and White House that would consider these gaps a national emergency. A recession in early 2020 would raise those odds. And if not in 2020 then by 2024 it might even be more plausible. That said, let’s look at what your proposals to raise taxes and redistribute income might actually look like. First, the on-budget national deficit for this year will be in the $1 trillion range and when you add in the off-budget deficits total debt could easily rise by $1.3 trillion or more. That’s just in 2019 and it won’t get much better in 2020. Total US government debt is now $22.4 trillion. We could easily see the national debt at $25 trillion before the next inauguration. That doesn’t include the $3 trillion+ state and local governments owe, nor some $100 trillion of unfunded federal liabilities or $6.7 trillion of unfunded state and local government pensions (data from The US Debt Clock.) Even a garden-variety recession will blow those deficit numbers out of the water. If revenue falls and expenses rise as they did in the last two recessions, a $2-trillion deficit is more than likely. The national debt would almost certainly reach $30 trillion within a few years. Interest on the national debt is budgeted at $389 billion for fiscal 2019. Assuming similar interest rates in the future, that cost will rise to almost $550 billion on a $30-trillion national debt—almost as much as the defense budget. Essentially, we would need to raise taxes by $1 trillion along with some considerable budget cutting just to balance the budget before we get into any redistribution of income. But let’s set aside that for the moment and talk about raising taxes enough to fund the income redistribution programs you would like to see. In your words, you want to increase taxes “from the top” and earmark those increases to help those in the bottom and middle, somehow “engineering” those taxes to have no effect on productivity. Let’s look at some real-world numbers of what the top income earners pay in taxes, courtesy of the Tax Foundation.

Source: Tax Foundation Some 68% of all income tax revenue comes from the top 10% of income earners. That’s fair enough, I suppose. Interestingly, the top 1/10 of 1% of income tax payers pay more than the bottom 50% combined.

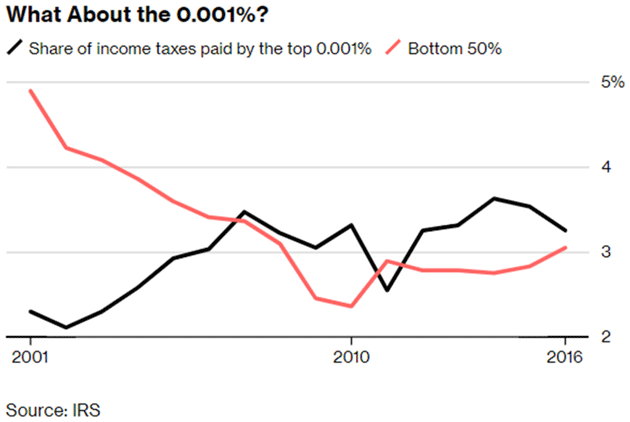

Source: Bloomberg Here’s a chart from that same Bloomberg article that breaks it down by the different percentiles and the percentage of total income taxes they paid. The top 1% paid a greater share of individual income taxes (37.3%) than the bottom 90% combined (30.5%).

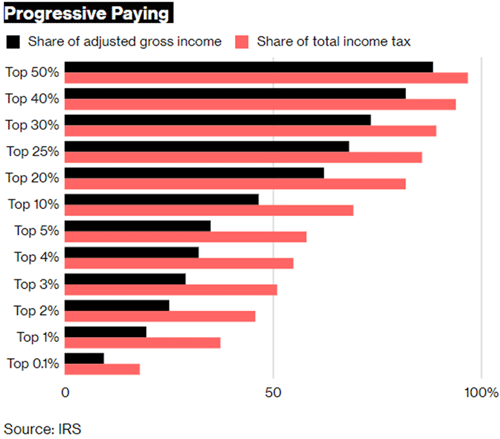

Source: Bloomberg Now, let’s go back to the Tax Foundation data. This is part of a larger and more detailed analysis at the website.

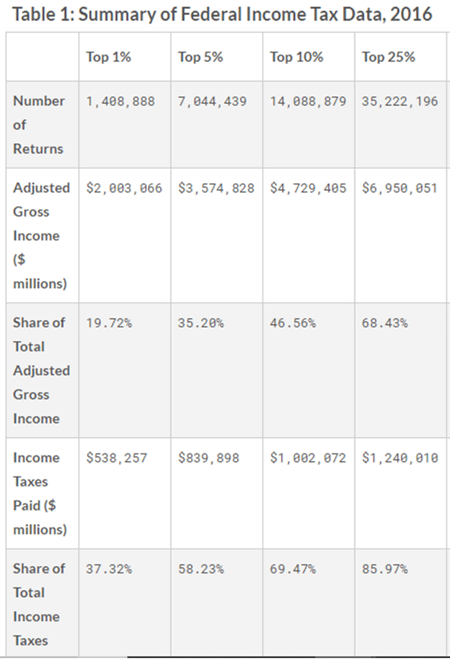

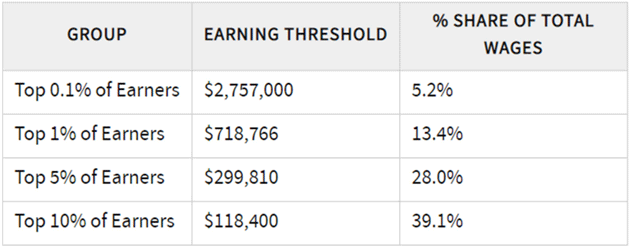

Source: Tax Foundation Note the top 10% of income tax payers paid approximately $1 trillion in income taxes. When you say that you want to “raise more from the top via taxes” let’s see what that means. Giving $3,000 to each of the 70 million tax filers in the bottom half would require $210 billion. You would also need the government to have the systems and people to do this which would require at least another $20 billion or so, and that may be giving a lot of credit to government efficiency. So, getting an additional $230 billion from the top 10% of income earners would mean giving that group a roughly 23% across-the-board tax increase. That’s before we do anything about the national deficit. Note also, to do this you wouldn’t be taxing only millionaires and the rich. To get in the top 10% of income payers you merely need to be making ~$140,000 a year. The cut-off for the top 5% is approximately $200,000. So, let’s say we ask only the top 5% of income earners to fund this new spending. To get that same $230 billion you would need to raise their taxes by approximately 30%, give or take. Want to do it just from the top 1%? You would need to raise their tax rates by 50%. Again, that is before we even begin to reduce the deficit. And when you say that you want to engineer these taxes not to affect productivity, I am scratching my head trying to figure out precisely how to do that. The marginal tax rate for incomes over $500,000 is 37%. So if you wanted to get that $230 billion from the wealthiest taxpayers, their top marginal tax rate would rise to approximately 56%. Add state income tax and the rates could easily get to 60% or more in some states. And do we really want to raise taxes either during or just after recession? Seriously? Not exactly a prescription to boost the economy and productivity. Adding a little more complexity, there is a difference between the top 10% of earners and the top 10% of taxpayers. To be a top-10% earner, you merely have to make $118,000. In October of 2018, the Economic Policy Institute published a study showing that the top 1% reached the highest wages ever in 2017. But when you read all those stories about the 1%—or even the top 5% or 10%—how much money do you need to pull in to be in one of those groups?

Source: Investopedia We already have a system where somewhere between 40–47% of taxpayers literally pay no income tax. (They do, of course, pay Social Security and Medicare taxes on their wage incomes.) How much more progressivity do we need in order to be “fair,” whatever that is? It is one thing to simply state that you want to engineer taxes in order to redistribute income to the lower half and doing that while not hurting productivity. But it is another thing entirely to lay out exactly how much money is needed to be able to make the system more equitable. Is $3,000 per family enough? Do you need twice that much? Where does the money come from and how much would taxes have to be raised? It is one thing to say that we should tax pollution (if it would help bring down pollution, I might even find myself in favor of that—pollution has a social cost) but it is another thing to say what constitutes pollution and how much. Automobile emissions? Do you raise taxes on the bottom 50% for their cars? It gets complicated real quick. Louisiana Sen. Russell Long (Senate finance committee chair from 1966 to 1981) is credited with saying, “Most people have the same philosophy about taxes. Don’t tax you, don’t tax me, tax that fellow behind the tree.” If the top 10% are the “fellow behind the tree” then you must raise their taxes substantially in order to collect any meaningful amount of money. Or else move down the scale and raise taxes on many more people. The real emergency? Trillion-dollar deficits that will grow to $2-trillion deficits during the next recession. You could literally double taxes for the top 10% and barely balance the budget today, before any recession. That is how far out of balance our system has gotten. And all this is before we have paid for climate change or free college or any of the progressive left’s other proposals, along with income redistribution. And to be fair, Republicans are no longer concerned about multi-trillion-dollar deficits, either. They just have different spending priorities. You want bipartisanship, Ray? It seems to me that deficit spending pretty much gets everyone’s support. Not exactly the kind of bipartisan cooperation that I find helpful. Finally, you call for coordinated monetary and fiscal policies. Quoting: 5. Coordination of monetary and fiscal policies. Because money is clogged at the top and because the capacity of central banks to ease enough to reverse the next economic downturn is limited, fiscal policy will have to be more coordinated with monetary policy, which can happen while maintaining the Federal Reserve’s independence. If done well, this will both stimulate economic growth and reduce the effects that quantitative easing has on increasing the wealth gap by shifting money and credit into the hands of those who have a higher propensity to spend from those who have a higher propensity to save and from those who need it less to those who need it more. Here and elsewhere, you acknowledge that quantitative easing did in fact make the income and wealth gap worse. So you call for fiscal policy to do the income redistribution that you feel necessary. When I read Parts 1 and 2, I came to this section and left a little bit mystified. If you didn’t want to use quantitative easing, and the realities of our national debt and growing deficits being what they are, how much would taxes have to be raised? And then you answered that question when you wrote It’s Time to Look More Carefully at ‘Monetary Policy 3 (MP3)’ and ‘Modern Monetary Theory’. And it is at this point that you went from being kinda, sorta wrong to being really, really, really wrong. [To be continued…] Next week we will look at various scenarios for the future (going out about 10 years), what their various outcomes and costs might be, and how we can deal with the massive debt and deficits, not to mention new spending programs. I am actually going to propose my own solution that I think will put us back on track. Unfortunately, paraphrasing Winston Churchill, the US will likely try everything else before we finally do the right thing. I am enjoying the beautiful weather here in Puerto Rico. Later this month I’ll be visiting Boston and New York, then on July 4 I fly back to Puerto Rico working on what will likely be Part 5 of this series. It may or may not be the final part. I’ll just see how far I get. Shane has developed an interesting new hobby. One of our guest bedrooms has an open outdoor alcove. There was really nothing in it but weeds when we moved in. She has cleared it out and made a nice little garden. The interesting thing is that she planted something that to me looks like a weed but monarch butterfly caterpillars evidently consider those weeds to be ambrosia. So now Shane is growing cocoons and raising monarch butterflies. It is really pretty cool to watch them emerge from the cocoon. And theoretically, they’ll migrate back next year, since they supposedly return where they were born to start the process all over again. We’ll see how that theory works next year. But right now, it’s just a lot of fun. And with that I will hit the send button. I feel like there’s more to be said on taxes. I know that Elizabeth Warren is talking about a wealth tax. I’m not quite certain how that would work on illiquid assets. It would certainly raise a lot of money but imagine the chaos. On that cheerful thought, let me wish you a great week! Your thinking about taxes in the future analyst,   | John Mauldin

Chairman, Mauldin Economics |

P.S. Want even more great analysis from my worldwide network? With Over My Shoulder you'll see some of the exclusive economic research that goes into my letters. Click here to learn more.    | | Share Your Thoughts on This Article | | |

|